New rating for Innovatec S.p.A.

modefinance published the Solicited Corporate Credit Rating of INNOVATEC S.P.A. on its CRA website, and the rating assigned to the entity is B1 (first issuance).

The analysis revealed it is an adequate company with average capabilities of repaying financial obligations and it is little affected by adverse economic scenarios.

The company INNOVATEC S.P.A. is a holding company listed on Borsa Italiana (the Italian Stock Exchange), active in Clean Technology, i.e. the set of technologies that develop processes, products or services useful to reduce negative environmental impacts by improving energy efficiency, using sustainable resources or undertaking environmental protection activities. The Company was founded in 2013 and deals with the development of energy efficiency projects, products and services offered to companies. In addition, the company is active in the field of renewable sources and the construction and management of plants for the production of electricity from renewable sources.

Key Rating Assumption

At consolidated level, INNOVATEC S.P.A.’s economic and financial situation is “sufficient” and particularly influenced by the recent acquisition of the Luxemburg company CLEAN TECH LUXCO S.A. The acquisition led to an increase in the leverage ratio, which nevertheless remains at a largely adequate level, whilst the financial indebteness has improved. The management of lending and short-term sources is adequate, as well as profitability, which shows an appreciable ROE value.

In terms of cash flow, the operations management covers quite completely the absorption caused by investments and the repayment of financial exposures: net of this, the Company continues to have a high level of liquidity.

The Bank of Italy’s Central Credit Register shows only loans, the management of which is characterized by numerous short-term overdrafts, even of large amounts. Nonetheless no disputes or serious anomalies are recorded.

Since 2013, the Company has been listed on the AIM Italia segment of Borsa Italiana. The performance of the stocks over the last twelve months has been slightly volatile, yet characterized by a positive increase in the share price.

The Company has a collegial administrative body (board of directors), which is supported by an adequately composed supervisory body and a specialized auditing firm. The corporate structure is quite articulated. The main owner is the entrepreneur Pietro Colucci, but most of the shares are listed. In turn, the Company has a lot of subsidiaries, including the recent acquisition, which is of significant strategic value.

There are no black records concerning the Company and the members of the Board of Directors, while the parent company is subject to arrangement with creditors project.

The Company is positioned above the median of sector in terms of size and profitability, while it performs below the industry median in terms of solvency. The peer group shows a constantly decreasing, yet good, leverage level throughout the period under review, while the financial debt shows a slight increase, though still adequate. The industry’s liquidity indicators show a slight, but constant increase and such as to be considered adequate, while the sector’s ROE value remains barely adequate.

The Italian energy sector is experiencing an important transition towards a greater contribution of the renewable energy sources to the overall national energy production. This could open up attractive scenarios for the Company in terms of turnover growth. At the same time, the macroeconomic scenario, already weak before the crisis, is still affected by the Coronavirus emergency, althoughis showing the first signs of recovery in the current year. Compliance with certain important pillars could ensure a rapid recovery of what has been lost in terms of GPD.

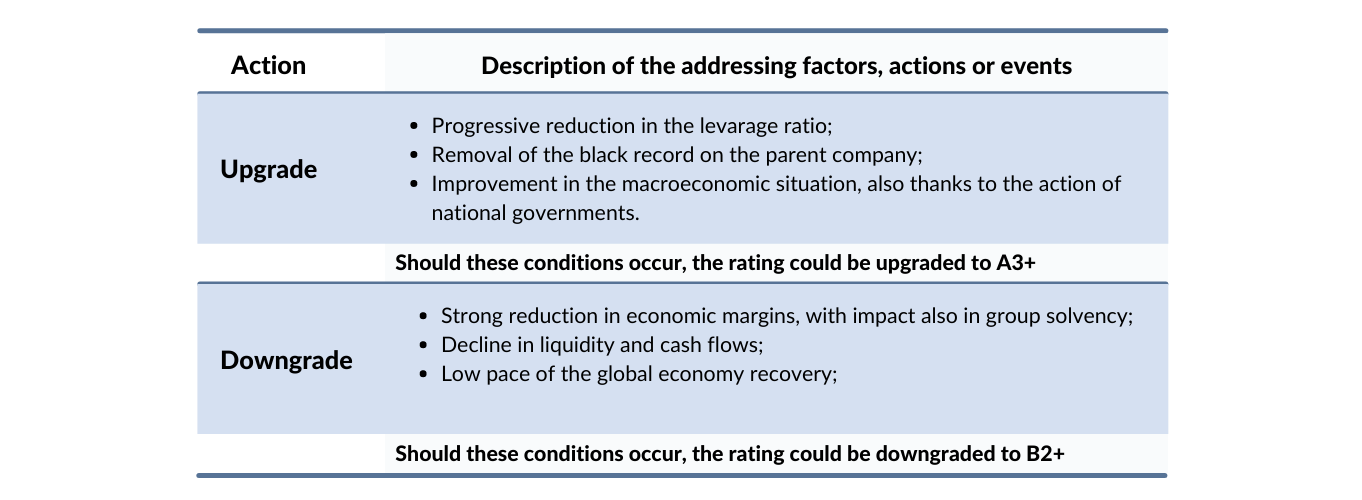

Sensitivity Analysis

In the following table, the addressing factors, actions or events that could lead to an upgrade or a downgrade are summarized:

{kind=link}

Important

The present Corporate Credit rating is issued by modefinance under EU Regulation N. 1060/2009 and following amendments.

The present rating is solicited, and based on both private and public information. The rated entity and/or related third parties have provided all private information used. modefinance had access to some accounts and other relevant internal documents of the rated entity and/or related third parties. Solicited and unsolicited ratings issued by modefinance are of comparable quality, as the solicitation status has no effect on methodologies used. More comprehensive information on modefinance Corporate Credit Ratings are available here.

The present Corporate Credit Rating is issued on MORE Methodology 2.0 and Rating Methodology 1.0. A comprehensive description of both methodologies, as well as information on modefinance Rating Scale and Mappings, is available here. For information on historical default rates of modefinance Corporate Credit Ratings please refer to ESMA Central Repository and ESMA European Rating Platform.

modefinance refers to default as a company under bankruptcy, or under liquidation status, or under administration or for which missed payments on a financial obligation are officially recorded.

The quality of the information available on the rated entity and used to determine the present rating was judged by modefinance as satisfactory. Please note that modefinance does not perform any audit activity and is not in a position to guarantee the accuracy of any information used and/or reported in the present document. As such, modefinance can accept no liability whatsoever for actions taken based on any information that may subsequently prove to be incorrect.

The present credit rating was notified to the rated entity in order to identify potential factual errors, as prescribed by the CRA Regulation.

No amendments were applied after the notification process.

The rated entity is not a buyer of ancillary services provided by modefinance.

The rating action issued by modefinance was performed independently. The analysts, members of the rating team involved in the process, modefinance Srl and its members and shareholders do not have any conflicts of interest in relation to the Rated Entity and/or Related Third Parties. If in the future a potential conflict of interest is identified in relation to the persons reported above, modefinance Ratings will provide the appropriate information and if necessary the rating will be withdrawn.

The present Credit Rating is an opinion of the general creditworthiness that modefinance issues on the rated entity, and should be relied upon to a limited degree. The issued rating is subject to an ongoing monitoring until withdrawal.

Contacts

Head Analyst – Christian Raimondo (Rating Analyst)

christian.raimondo@modefinance.com

+39 040 3756740

Assistant Analyst – Stefania Latin (Rating Analyst)

stefania.latin@modefinance.com

+39 040 3756740

Responsible for Rating Approval – Pinar Dilek

pinar.dilek@modefinance.com

+39 040 3756740