Environmental sustainability, circular economy, global warming, CO2 emissions reduction: these are concepts that we all heard well before the emergence of the notion of ESG in various contexts, which go from the corporate world to loans granted by financial institutions. However, why is it that important to identify and correctly manage climate and environmental risks in the financial sector?

In one of our previous articles, we introduced the directives approved by Bank of Italy in the document “Aspettative di vigilanza sui rischi climatici e ambientali” of April 2022, with regard to the need to integrate climate and environmental risk factors in the business culture and strategy, as far as risk management and the disclosure to financial institutions is concerned. Indeed, for national and European banking institutions, introducing climate and environmental risk evaluations in the comprehensive judgement regarding the economic and financial health of a given entity on the part of financial institutions, becomes essential in order to cope with the changes that the economic system will be facing in the coming years. Moreover, banks and enterprises that are able to implement suitable policies in order to identify and mitigate climate and environmental risks, will continue to provide the necessary access to credit to companies (banks), and maintain their competitiveness and reputation on the market (enterprises).

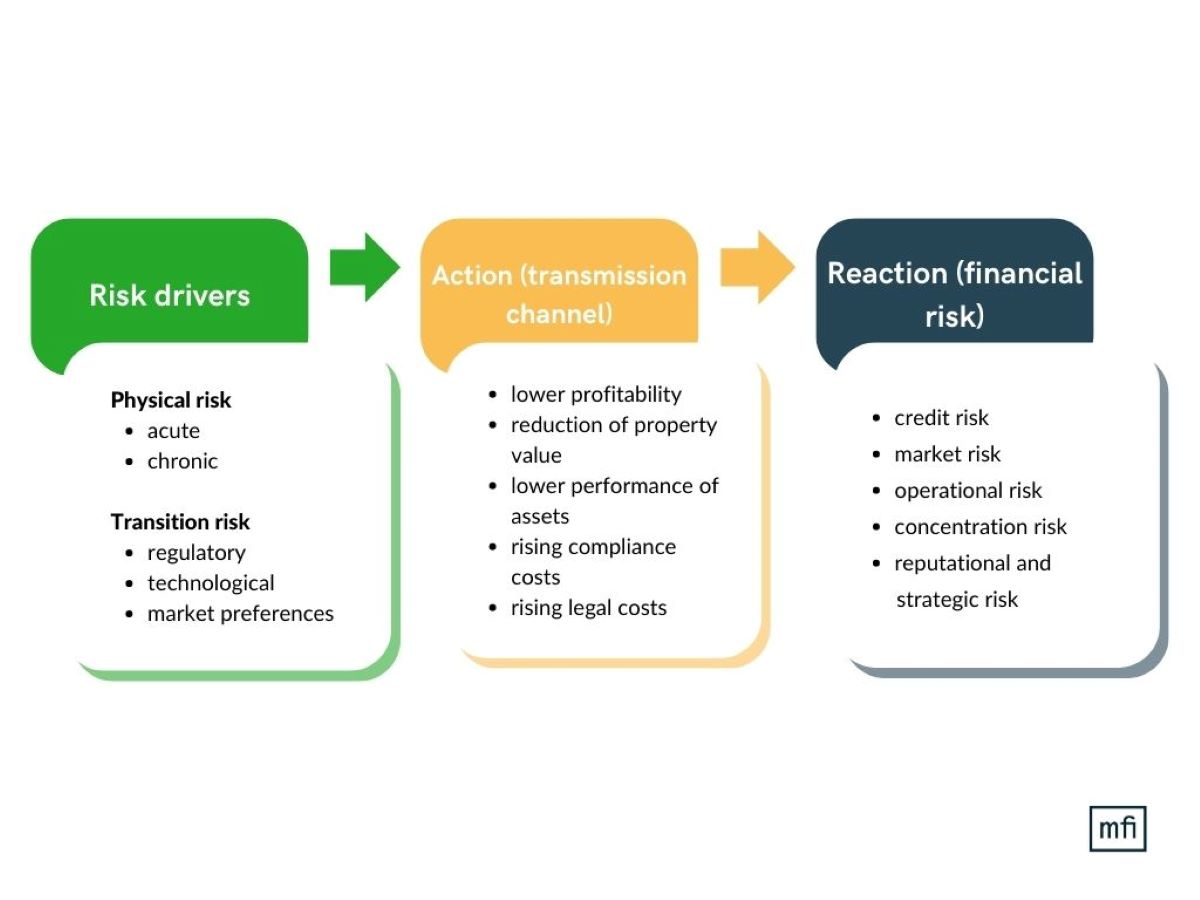

The financial world between physical risk and transition risk

The document drafted by Bank of Italy – in line with what has been presented in the ECB guide, Guide on climate-related and environmental risks and in the EBA report on management and supervision of ESG risks for credit institutions and investment firms – divides climate and environmental risks in:

- Physical risk: it refers to the economic impact caused by the expected increase in extreme natural events, whose manifestation can be defined as:

- acute, in the circumstance that the risk depends on the occurrence of extreme environmental events (e.g. flooding, earthquakes, hailstorms etc.) connected to climate changes that increase their intensity and frequency

- chronic, whenever the risk is determined by whether events that occur progressively (e.g. ecosystems deterioration, biodiversity loss, gradually rising sea-level and temperatures etc.)

- Transition risk: it includes the economic impact to which enterprises can be prone as a consequence of the implementation of regulations designed to reduce carbon emissions and encourage the development of renewable energy, of technological progress and adaptation, as well as of a change in consumer preferences and in market confidence. Not being able to adapt to this non-negligible change, underestimating it and disregarding these policies, frequently reflects in higher taxation, market preferences diversion and difficult access to credit for enterprises.

Bank of Italy’s document, as well as practical examples that are surrounding us more and more, reveal that a correct approach to risk management on the part of banks and enterprises enables a facilitated prevention of climate and environmental risks (physical and transition), thus avoiding and mitigating the negative impact of traditional financial risks (credit, market, reputational and liquidity).

In order to make the context clearer, here are some examples of physical and transition risks’ adverse effects on the enterprise’s economic and financial situation. Regulatory initiatives, which concern both financial institutions and SMEs, aimed at accelerating the green transition, will cause higher costs and lower revenue for entities that leave a great carbon footprint, with a consequent creditworthiness’ deterioration. In this regard, the stakeholders’ increasing attention for climate issues generally enhances reputational risks of the entity that doesn’t adapt to their expectations, as well as legal risks caused by activities that do not conform to the protection of the environment.

{kind=link}

Physical and transition risks proprietary models: modefinance solutions now on the market

The directives on the part of Bank of Italy are indispensable also for Credit Rating Agencies that, besides issuing traditional creditworthiness assessments, are more and more enriching their range of services with sustainability evaluations. In this context, modefinance’s multidisciplinary teams developed two proprietary models for the climate and environmental risk evaluation: physical risk and transitional risk models.

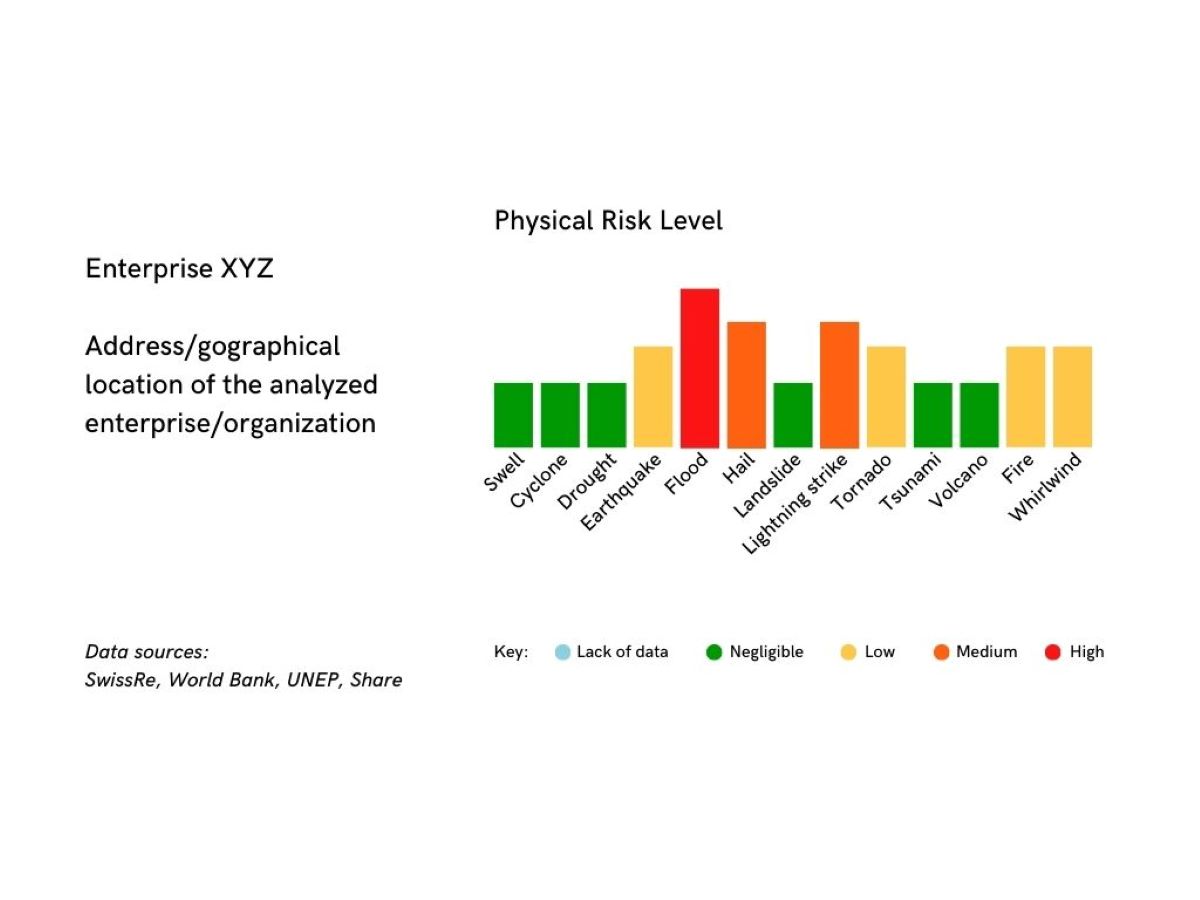

The physical risk model, based on sophisticated AI tools, automatically geolocates the enterprise by using the VAT registration number (partita IVA), thus returning the physical risk to which the firm is subject as a result.

Within the model, the indicators monitor the storage and/or production sites’ susceptibility to specific physical risks (e.g. hailstorms, earthquakes, volcanoes, fire etc.), each of which uses a specific methodology for the risk assessment. When it comes to determining the level of physical risk, in addition to geographical data, the risk exposure is also examined based on benchmarks that take account of business’ specific characteristics according to a materiality map, which indicates the relevance of a given physical event for a given business sector.

{kind=link}

Moreover, the physical risk evaluation result is displayed to the user through a synthetic and automated score, Automated Score ESG, that does not need user interaction and that uses quantitative KPIs associated with probabilities of certain extreme events taking place in a given geographical location.

On the other hand, given the nature of the transition risk, whose KPIs measure the economic and financial impact of factors such as increase in costs related to the taxation of carbon emissions and exposure to legal disputes, its assessment is qualitative. Therefore, modefinance developed a specific questionnaire to be submitted to the company that allows to achieve a quantification of the transition risk (at this point, through an automatic model). modefinance’s questionnaire for the evaluation of the transition risk is oriented to define the degree of awareness and actions taken by the enterprise for the management of:

- CO2 emissions monitoring and reduction

- use of renewable energy sources

- energy efficiency

- research and development.

The questionnaire, developed within the TransparEEnS project based on large amounts of data collected, covers numerous aspects related to the efficient use of energy sources and of renewable sources, such as:

- presence of electricity supply contracts with the origin of the electricity >50% renewable

- type of energy production plants

- energy efficiency measures

- presence of environmental certifications

In conclusion, to minimize the risks arising from corporate policies harmful to the planet within a perpetually-changing society could be lethal, and will be increasingly so. For the enterprises and for the planet. As a result, to obtain an assessment certifying the sustainability of a given company and to become aware of the gravity of the possible consequences on the one hand, but also of the multitude of opportunities that should be taken in order to remain competitive, is becoming ever more necessary, both for banks and enterprises.