Solicited Corporate Credit Rating for CAL.ME. SPA: A3- (First Issuance)

modefinance published the Solicited Corporate Credit Rating of CAL.ME. SPA on the CRA website and the rating assigned to the entity is A3- (first issuance). The analysis revealed that the Company has a strong capacity to meet its commitment on financial obligations.

CAL.ME. S.P.A. is a company belonging to the industrial branch of the Calmefin Group, specialized in the production for internal use and sale of clinker, a fundamental intermediate product for the concrete manufacturing process. O¬ther products, also intended for the construction and industrial sectors, include cement, lime, and calcium carbonate. The Company, at the forefront in terms of both vertical integration and environmental sustainability, operates predominantly in southern and central Italy.

Key Rating Assumptions

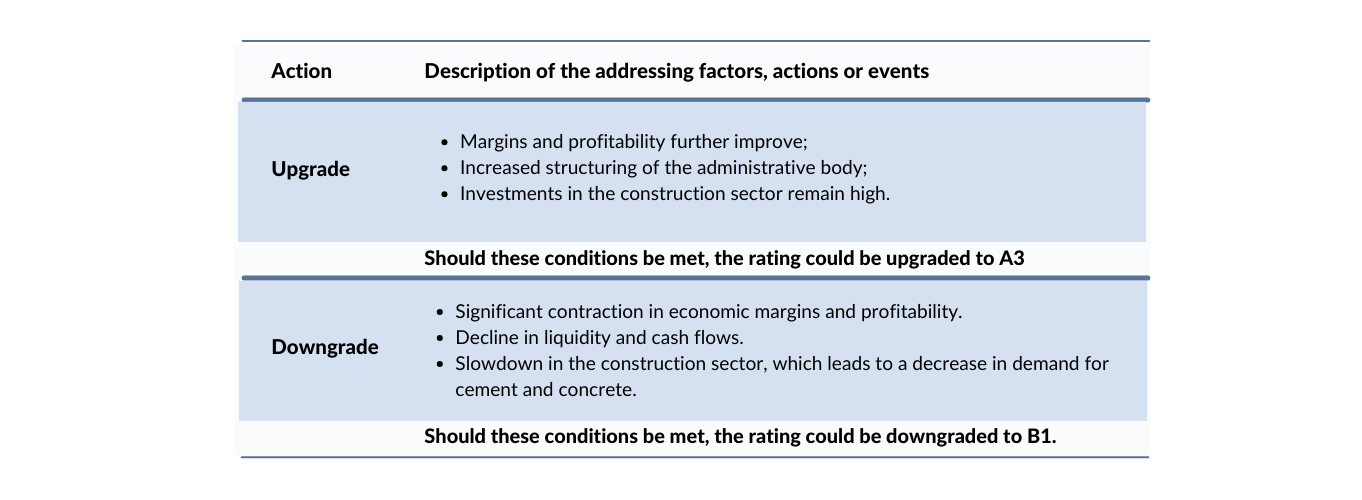

The Company presents an economic and financial situation characterized by satisfactory solvency levels and effective liquidity management. The profitability area, thanks to the significant increase in margins achieved during the 2022 fiscal year, shows a good improvement in key performance indicators. The cash flow generated from operations demonstrates satisfactory levels of self-financing, which are nearly sufficient to cover investments and the repayment of financial debts. There is an increasing absorption of resources by working capital, partly due to the rise in purchase prices and the adjustment of sales prices to cover the higher costs incurred during the procurement phase.

Regarding the governance structure, the control function has been assigned to a collective body, while the legal audit of the annual financial statements has been entrusted to a specialized company. Considering the expected growth in the Company's size in the coming years, it is clear that there is a need for a more structured administrative body, which is currently composed of a sole administrator. The group structure appears complex but is well-organized into three distinct operational branches.

The analysis of the peer group shows a progressive increase in capitalization and improving liquidity indicators. The profitability is at a good level and demonstrates strong growth between 2019 and 2022. The Company's positioning in terms of size and solvency is sound, while profitability is lower than the sector median.

The cement market in Italy is closely tied to the construction sector. The latter has shown, in the second quarter of 2023, a significant decrease in investment levels compared to the same period in the previous year. This decline is mainly due to the sharp slowdown in the residential segment, which has been particularly affected by legislative changes to construction incentives and the rise in interest rates. Despite this decline, the overall investments for the current year are expected to exceed the levels of the previous year, mainly due to the boost from the National Recovery and Resilience Plan (PNRR) for the implementation of public projects.

Finally, the macroeconomic growth is expected to be modest in 2023, but the figures could be revised upwards in the coming months.

Sensitivity Analysis

{kind=link}

Important

The present Corporate Credit rating is issued by modefinance under EU Regulation 1060/2009 and following amendments.

The present rating is solicited and is based on both private and public information. The rated entity and/or related third parties have provided all private information used. modefinance had access to some accounts and other relevant internal documents of the rated entity and/or related third parties. Solicited and unsolicited ratings issued by modefinance are of comparable quality, as the solicitation status has no effect on methodologies used. More comprehensive information on modefinance Corporate Credit Ratings are available at http://cra.modefinance.com/en

The present Corporate Credit Rating is issued on MORE Methodology 2.0 and Rating Methodology 1.0. A comprehensive description of both methodologies, as well as information on modefinance Rating Scale and Mappings, is available at http://cra.modefinance.com/en/methodologies.

For information on historical default rates of modefinance Corporate Credit Ratings please refer to ESMA Central Repository and ESMA European Rating Platform.

modefinance refers to default as a company under bankruptcy, or under liquidation status, or under administration or for which missed payments on a financial obligation are officially recorded.

The quality of the information available on the rated entity and used to determine the present rating was judged by modefinance as satisfactory. Please note that modefinance does not perform any audit activity and is not in a position to guarantee the accuracy of any information used and/or reported in the present document. As such, modefinance can accept no liability whatsoever for actions taken based on any information that may subsequently prove to be incorrect.

The present credit rating was notified to the rated entity in order to identify potential factual errors, as prescribed by the CRA Regulation.

No amendments were applied after the notification process.

The rated entity is a buyer of ancillary services provided by modefinance (private corporate rating). modefinance ensures that such situation does not imply a conflict of interest in the issuance of the present credit rating.

The rating action issued by modefinance was performed independently. The analysts, members of the rating team involved in the process, modefinance Srl and its members and shareholders do not have any conflicts of interest in relation to the Rated Entity and/or Related Third Parties. If in the future a potential conflict of interest is identified in relation to the persons reported above, modefinance Ratings will provide the appropriate information and if necessary the rating will be withdrawn.

The present Credit Rating is an opinion of the general creditworthiness that modefinance issues on the rated entity, and should be relied upon to a limited degree. The issued rating is subject to an ongoing monitoring until withdrawal.

Contacts

Head Analyst - Stefano Chirsich, Rating Analyst

stefano.chirsich@modefinance.com

Responsible for Rating Approval - Pinar Dilek, Rating Process Manager

pinar.dilek@modefinance.com