Solicited Corporate Credit Rating for SPOT LIGHT IMPORT EXPORT SRL: A3- (First Issuance)

modefinance published the Solicited Corporate Credit Rating of SPOT LIGHT IMPORT EXPORT SRL on the CRA website and the rating assigned to the entity is A3- (first issuance). The analysis revealed that the Company has a strong capacity to meet its commitment on financial obligations.

SPOT LIGHT IMPORT EXPORT SRL was established in 2002 as an advertising agency specializing in integrated communication, social media marketing, content and video production in the advertising field. Since 2020, with the entry of Mr. Napoletano Giuseppe as sole shareholder, the Company's activities have undergone diversification, seizing the business opportunities in the field of construction, marketing and leasing of billboards, as well as in the import/export of materials for the billboard and advertising printing sector. Hence, the Company name was changed from "Spot Light Advertising" to "Spot Light Import Export S.r.l." To consolidate the revenue growth trend recorded in recent years, the Company plans two considerable investments: a printing centre in the province of Caserta and a headquarter close to Milan, with the aim of creating an advertising district that can operate as apoint of reference for other agencies and professionals in the sector.

Key Rating Assumptions

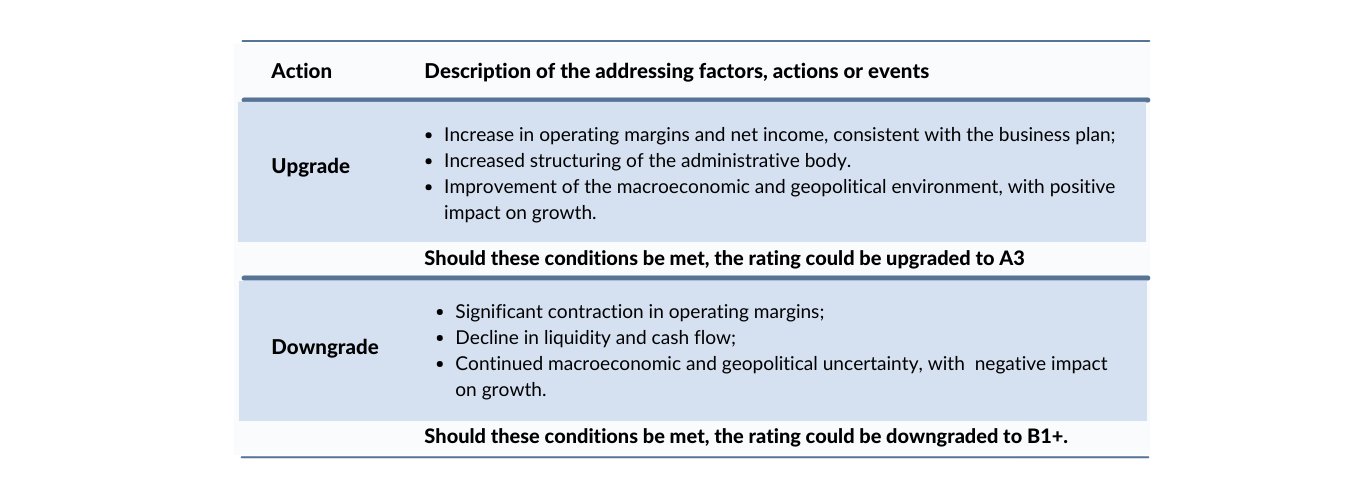

SPOT LIGHT IMPORT EXPORT S.R.L. presents an adequate economic-financial situation, characterized firstly by the total absence of financial debt, which follows the shareholder's commitment to efficient management of credit collection and debt payment, which ensures the liquidity inflow necessary to carry out operations independently. Along with the prevalence of shareholders' equity (1.40 mln euros) over liabilities (1.06 mln euros), this led to solvency indicators on extremely good values. Liquidity appears adequate, with ratios above one. The cash inflow from core business fully financed investments and repaid bank debts. Sales revenues (5.42 mln euros) marked +6% YoY growth, confirming the positive trend of recent years. In 2022, most of the Company's turnover (45%) was generated by the construction, marketing, maintenance, service, and rental of billboards, followed by the wholesale trade of raw materials for the advertising sector (25%). Operating margins remained almost flat compared to 2021, as the increase in production costs went hand in hand with the expansion of sales volumes. Net income of 309 thousand euros (+5.82%) resulted in an ROE of 21.99%. Together with an ROI of 18.22% and an EBITDA/revenues ratio of 10%, the overall income performance is adequate.

The ownership structure, as well as the governance and control structure, show no degree of complexity. As mentioned earlier, the Company is owned by a single shareholder, Mr. Napoletano Giuseppe, who also acts as director together with Mr. Della Posta Pietro. The Company currently does not have any supervisory body , but will nominate it starting from January 2024. The strengthening of the governance and control structure appears necessary and desirable given the dimensional growth planned by the Company in 2024.

The analysis of the peer group revealed a positive trend in the sector’s performance. The peer group recorded an improvement in solvency indicators from 2019 to 2022, achieving a sufficient balance between equity and debt. The liquidity profile appears to be adequate. Profitability performance, after the post-Covid recovery, is also good in 2022, with the main ratios on higher values than the pre-pandemic period. Compared to the peer group, the Company ranks high in size and solvency. Profitability ranking also appears adequate, with a positioning higher than the median of the analyzed sample.

Finally, Italian macroeconomic growth is expected to be modest in 2023, but the figures could be revised upward in the upcoming future.

Sensitivity Analysis

{kind=link}

Important

The present Corporate Credit rating is issued by modefinance under EU Regulation 1060/2009 and following amendments.

The present rating is solicited and is based on both private and public information. The rated entity and/or related third parties have provided all private information used. modefinance had access to some accounts and other relevant internal documents of the rated entity and/or related third parties. Solicited and unsolicited ratings issued by modefinance are of comparable quality, as the solicitation status has no effect on methodologies used. More comprehensive information on modefinance Corporate Credit Ratings are available at http://cra.modefinance.com/en

The present Corporate Credit Rating is issued on MORE Methodology 2.0 and Rating Methodology 1.0. A comprehensive description of both methodologies, as well as information on modefinance Rating Scale and Mappings, is available at http://cra.modefinance.com/en/methodologies.

For information on historical default rates of modefinance Corporate Credit Ratings please refer to ESMA Central Repository and ESMA European Rating Platform.

modefinance refers to default as a company under bankruptcy, or under liquidation status, or under administration or for which missed payments on a financial obligation are officially recorded.

The quality of the information available on the rated entity and used to determine the present rating was judged by modefinance as satisfactory. Please note that modefinance does not perform any audit activity and is not in a position to guarantee the accuracy of any information used and/or reported in the present document. As such, modefinance can accept no liability whatsoever for actions taken based on any information that may subsequently prove to be incorrect.

The present credit rating was notified to the rated entity in order to identify potential factual errors, as prescribed by the CRA Regulation.

No amendments were applied after the notification process.

The rated entity is a buyer of ancillary services provided by modefinance (private corporate rating). modefinance ensures that such situation does not imply a conflict of interest in the issuance of the present credit rating.

The rating action issued by modefinance was performed independently. The analysts, members of the rating team involved in the process, modefinance Srl and its members and shareholders do not have any conflicts of interest in relation to the Rated Entity and/or Related Third Parties. If in the future a potential conflict of interest is identified in relation to the persons reported above, modefinance Ratings will provide the appropriate information and if necessary the rating will be withdrawn.

The present Credit Rating is an opinion of the general creditworthiness that modefinance issues on the rated entity, and should be relied upon to a limited degree. The issued rating is subject to an ongoing monitoring until withdrawal.

Contacts

Head Analyst - Stefano Chirsich, Rating Analyst

elisa.graffi@modefinance.com

Responsible for Rating Approval - Pinar Dilek, Rating Process Manager

pinar.dilek@modefinance.com