Solicited Corporate Credit Rating for ECOSERVIM S.R.L.: B1 (First Issuance)

modefinance published the Solicited Corporate Credit Rating of ECOSERVIM S.R.L. on the CRA website and the rating assigned to the entity is B1 (first issuance). The analysis revealed that the subject has a proper economic and financial balance and it is able to cope with adverse economic conditions in the medium and long term.

The company ECOSERVIM S.R.L. was founded in the 1970s in Reggio Emilia, thanks to the entrepreneurial initiative of Matteo Bonini, who set up a small firm for plumbing and heating services. Today the company is led by the founder's son, Gianluca, who has expanded the range of services for companies and privates to the entire region, hence founding the Ecoservim Group, active in the energy and facility management sectors. In detail, the company offers different types of services such as plumbing, energy saving, construction and heating/cooling systems, also thanks to the public incentives for buildings available in 2021 and 2022.

Key Rating Assumptions

The company's economic and financial situation is characterized by a strong growth in sales volumes, driven by the activities related to government incentives for the building industry. Despite the increase in production, the growth led to liquidity issues, which were solved by the company by the opening of different banking channels and the diversification of services offered.

The company has a collegial administrative body, whose actions are subject to the control of a collegial supervisory body. In addition, the company entrusts the certification of its financial statements to an auditing company.

The coportate structure is well outlined. The majority of the shares are held by the entrepreneur Gianluca Bonini, who is flanked by a private equity company as a minority shareholder. The Group is expanding with the establishment of real estate and instrumental companies.

The construction sector strongly grew in 2022, consolidating the excellent results of the previous year, driven by the tax incentives aimed at the renovation and energy redevelopment of residential properties. In 2023 investments in the sector will remain consistent, although the rise in interest rates, the high cost of raw materials and the provision of decree 11/2023 –which prohibits public bodies from purchasing credit and cancels the use of credit transfer or invoice discounts for future interventions - will have a negative impact on the sector. The growth of investments in the public works necessary for the implementation of the National Recovery and Resilience Plan, will partially compensate for the drop in incentives.

Despite the moderate drop in prices recorded in the first months of 2023, companies of the sector still face higher energy and material costs than in the post-pandemic months. Although the contraction in energy prices has in fact led to a drop in the prices of plastic materials, in the first quarter of 2023 the prices of non-energy commodities and steel products have grown further. In 2022, the residential real estate market continued its recovery, but the first signs of a slowdown were already felt in the fourth quarter, mainly due to inflation and the increase in mortgage interest rates, which have worsened credit access conditions with repercussions on the sector business activities.

The macroeconomic forecasts for Italy envisage modest growth in 2023 due to the rise in interest rates, rising inflation and the unfavorable economic situation. The early general elections resulted in a solid majority, which could lead to less uncertaintyHowever, the new government will have to follow the agenda of the previous one to complete the post-pandemic recovery plan. Macroeconomic forecasts could be revised in the sign of an improvement.

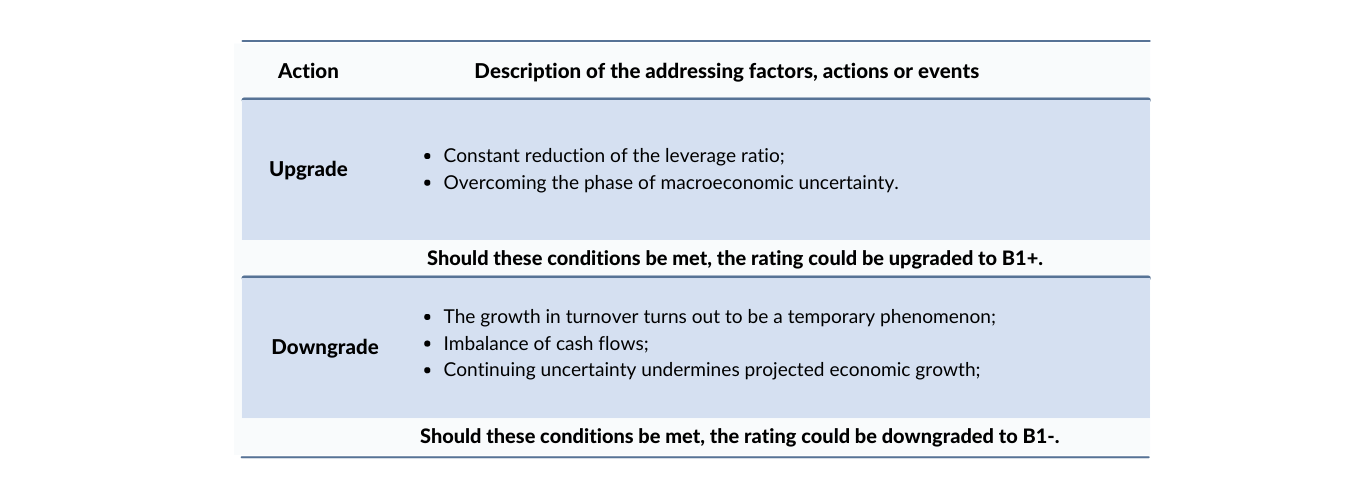

Sensitivity Analysis

{kind=link}

Important

The present Corporate Credit rating is issued by modefinance under EU Regulation 1060/2009 and following amendments.

The present rating is solicited and is based on both private and public information. The rated entity and/or related third parties have provided all private information used. modefinance had access to some accounts and other relevant internal documents of the rated entity and/or related third parties. Solicited and unsolicited ratings issued by modefinance are of comparable quality, as the solicitation status has no effect on methodologies used. More comprehensive information on modefinance Corporate Credit Ratings are available at http://cra.modefinance.com/en

The present Corporate Credit Rating is issued on MORE Methodology 2.0 and Rating Methodology 1.0. A comprehensive description of both methodologies, as well as information on modefinance Rating Scale and Mappings, is available at http://cra.modefinance.com/en/methodologies.

For information on historical default rates of modefinance Corporate Credit Ratings please refer to ESMA Central Repository and ESMA European Rating Platform.

modefinance refers to default as a company under bankruptcy, or under liquidation status, or under administration or for which missed payments on a financial obligation are officially recorded.

The quality of the information available on the rated entity and used to determine the present rating was judged by modefinance as satisfactory. Please note that modefinance does not perform any audit activity and is not in a position to guarantee the accuracy of any information used and/or reported in the present document. As such, modefinance can accept no liability whatsoever for actions taken based on any information that may subsequently prove to be incorrect.

The present credit rating was notified to the rated entity in order to identify potential factual errors, as prescribed by the CRA Regulation.

No amendments were applied after the notification process.

The rated entity is not a buyer of ancillary services provided by modefinance (credit risk software).

The rating action issued by modefinance was performed independently. The analysts, members of the rating team involved in the process, modefinance Srl and its members and shareholders do not have any conflicts of interest in relation to the Rated Entity and/or Related Third Parties. If in the future a potential conflict of interest is identified in relation to the persons reported above, modefinance Ratings will provide the appropriate information and if necessary the rating will be withdrawn.

The present Credit Rating is an opinion of the general creditworthiness that modefinance issues on the rated entity, and should be relied upon to a limited degree. The issued rating is subject to an ongoing monitoring until withdrawal.

Contacts

Head Analyst - Elisa Graffi, Rating Analyst

fabio.politelli@modefinance.com

Responsible for Rating Approval - Pinar Dilek, Rating Process Manager

pinar.dilek@modefinance.com