modefinance published the Solicited Corporate Credit Rating of TREMAGI S.R.L. on the website and the rating assigned to the entity is B1 (first issuance). The analysis revealed it is an adequate company with average capability of repaying financial obligations and it is little affected by adverse economic scenarios.

TREMAGI S.R.L. is a holding company heading the Group of the same name, established in 2009 and operating in the energy sector. The Company operates in both electricity and gas sales, working with wholesalers, resellers and final customers, thus managing to diversify its business thanks to the operations of the different subsidiaries. In terms of its contribution to the Group’s results, as well as on the experience front, the most important company in Tremagi Group is Illumia S.p.A., a company acquired in 2010 and active since 2003 in the segment of buying and selling electricity.

Key Rating Assumptions

The Company presents a broadly sufficient economic and financial situation, characterized by proper capitalization, which is accompanied by sustainable exposure to the financial system. The financial balance is confirmed to be adequate throughout the period analyzed, while trade receivables appear to be growing.

The analysis of cash flows reveals an erosion of liquidity by investments, which absorb the entire amount contributed by financing activities. This is accompanied by a positive operating management, but which is affected by the growth in trade receivables.

The Group structure appears to be rather articulated, with control attributable to entrepreneur Francesco Maria Bernardi, who appears to be the sole shareholder. At the same time, the Company has a large set of subsidiaries, all of which appear to be functional to the development of the core business. The Company presents an administrative body having a monocratic form, whose actions are subject to the control of a body having collegial form. At the same time, the Company’s financial statements is audited by a specialized company.

In terms of size, the Company is positioned above the industry median and such that it can be considered adequate. As far as solvency is concerned, the Company expressed a positioning overall in line with the industry median and therefore to be considered largely sufficient. Finally, looking to profitability, the Company manifest a positioning that remains satisfactory. The peer group expresses a solvency that has been steadily improving throughout the period under review and such that it can be considered largely sufficient, even after net of the recent growth in financial debt, which is still adequate. Again, the peer group expresses a growing financial balance throughout the period under review, with indicators above unity and therefore such as to be considered adequate.

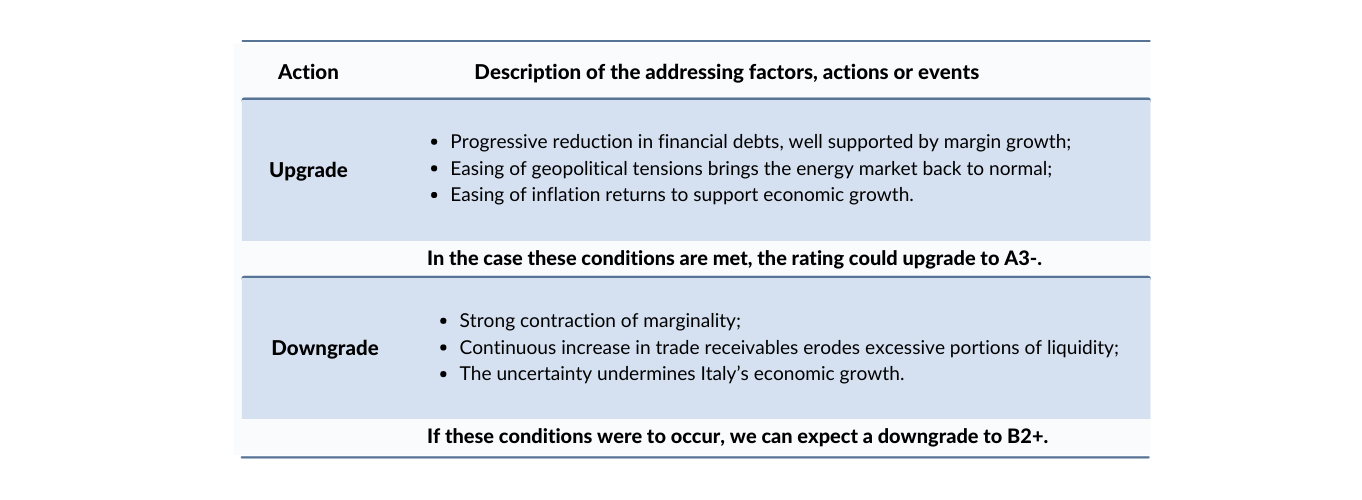

The energy sector In Italy is considerable strategic importance and has undergone a radical transformation in recent years, with the use of coal gradually declining in favor of greater use of renewable energies. This objective clashes, however, with recent geopolitical tensions and the need for the Italian government to look for alternative sources of supply. Within this framework, electricity consumption is expected to decline over the next few years. The abolition of the greater protection market will also broaden the pool of potential customers, although the granularity of the sector represents an important barrier to entry.

The macroeconomic picture for Italy shows that the recovery in 2021 has overall met forecasts, with sustained economic growth that could be confirmed in the coming years. However, recent geopolitical tensions undermine the forecasts, especially in terms of maintaining adequate economic growth, with domestic consumption likely to be affected by rising inflation. The 2022 macroeconomic forecast figures are therefore likely to be revised downward.

Sensitivity Analysis

{kind=link}

Important

The present Corporate Credit rating is issued by modefinance under EU Regulation 1060/2009 and following amendments.

The present rating is solicited and is based on both private and public information. The rated entity and/or related third parties have provided all private information used. modefinance had access to some accounts and other relevant internal documents of the rated entity and/or related third parties. Solicited and unsolicited ratings issued by modefinance are of comparable quality, as the solicitation status has no effect on methodologies used. More comprehensive information on modefinance Corporate Credit Ratings are available at http://cra.modefinance.com/en

The present Corporate Credit Rating is issued on MORE Methodology 2.0 and Rating Methodology 1.0. A comprehensive description of both methodologies, as well as information on modefinance Rating Scale and Mappings, is available at http://cra.modefinance.com/en/methodologies.

For information on historical default rates of modefinance Corporate Credit Ratings please refer to ESMA Central Repository and ESMA European Rating Platform.

modefinance refers to default as a company under bankruptcy, or under liquidation status, or under administration or for which missed payments on a financial obligation are officially recorded.

The quality of the information available on the rated entity and used to determine the present rating was judged by modefinance as satisfactory. Please note that modefinance does not perform any audit activity and is not in a position to guarantee the accuracy of any information used and/or reported in the present document. As such, modefinance can accept no liability whatsoever for actions taken based on any information that may subsequently prove to be incorrect.

The present credit rating was notified to the rated entity in order to identify potential factual errors, as prescribed by the CRA Regulation.

No amendments were applied after the notification process.

The rated entity is not a buyer of ancillary services provided by modefinance (credit risk software).

The rating action issued by modefinance was performed independently. The analysts, members of the rating team involved in the process, modefinance Srl and its members and shareholders do not have any conflicts of interest in relation to the Rated Entity and/or Related Third Parties. If in the future a potential conflict of interest is identified in relation to the persons reported above, modefinance Ratings will provide the appropriate information and if necessary the rating will be withdrawn.

The present Credit Rating is an opinion of the general creditworthiness that modefinance issues on the rated entity, and should be relied upon to a limited degree. The issued rating is subject to an ongoing monitoring until withdrawal.

Contacts

Head Analyst - Christian Raimondo, Rating Analyst

christian.raimondo@modefinance.com

Assistant Analyst - Andrea Marion, Rating Analyst

andrea.marion@modefinance.com

Responsible for Rating Approval - Pinar Dilek, Rating Process Manager

pinar.dilek@modefinance.com