Edited by Alberto Cibin, ESG Compliance Officer at modefinance

In 2024, the urgency for companies to align with ESG standards is becoming increasingly tangible. Yet, there is much confusion. CSRD, ESRS, SFDR, CSDDD, GRI, and so on, are all terms that make up the ever-expanding “alphabet soup” within the realm of environmental, social, and governance sustainability regulation of companies in the European Union, but not only.

Let’s bring some order. ESG regulations are a set of standards and governmental criteria governing actions, reporting, and disclosure related to the sustainability and ethical impact of a company or investment.

Although institutions have made great strides in promoting their commitment to regulating sustainability performance, the reporting landscape continues to be crowded with rapidly evolving directives and multiple unknowns. The absence of a unified ESG standard has led to the proliferation of numerous sustainability reporting frameworks, each with unique approaches and requirements. Determining which aspects of sustainability to emphasize, what to disclose, and which metrics to use remains a significant challenge, making it quite difficult to compare risks, ethical and sustainability performances, as well as decision-making for companies and investors.

Eventually, one of the major issues concerns data, or rather, their absence. A recent survey conducted by Dun & Bradstreet found that 47% of companies lack sufficient information, and 46% are unable to validate and trust their ESG data. Such issues can have operational and financial consequences, from regulatory non-compliance to fines, and even weakening of the global supply chain.

The increasingly evident climate change, as well as the growing attention to human rights and sustainable economic development, have placed ESG factors at the center of the international debate. Although sustainability might be considered a rather recent concept, the “long march” in this direction has its roots as far back as the late 20th century with the 1987 Brundtland Report of the World Commission on Environment and Development (link), which advocated for development that meets present needs without compromising the future.

Several decades and countless efforts later, the European Union is on track to provide us with clear rules that regulate risks related to holistic sustainability. Now let’s see what rules to follow in 2024.

Corporate Sustainability Reporting Directive (CSDR)

Since January 5, 2023, the European Union has implemented the Corporate Sustainability Reporting Directive (CSRD), a regulation aimed at modernizing and strengthening sustainability information provisions. This directive requires an increasing number of companies to adopt a specific reporting tool for environmental, social, and governance issues. The primary purpose of the CSRD is to enhance transparency and sustainability reporting, placing greater emphasis on the importance of ESG information in assessing the reliability and risks of a company.

This objective benefits investors, analysts, consumers, and other stakeholders by providing them with a clear overview of the sustainability performance of EU companies and their related impacts and business risks. Introduced as part of the European Commission’s Sustainable Finance Package, the CSRD significantly expands the scope and reporting requirements compared to the previous Non-Financial Reporting Directive (NFRD).

Companies subject to the CSRD are required to comply with the European Sustainability Reporting Standards (ESRS), developed by EFRAG, known as the European Financial Reporting Advisory Group, an independent body involving various stakeholders. On July 31, 2023, the European Commission adopted the first set of ESRS, enabling companies to fulfill the reporting obligations established by the CSRD. This initial set includes 12 sector-agnostic standards, two of a general nature, and ten relating to specific themes, divided into five environmental areas, four social areas, and one governance area. Additionally, the CSRD stipulates that EFRAG continues to develop sector-specific standards.

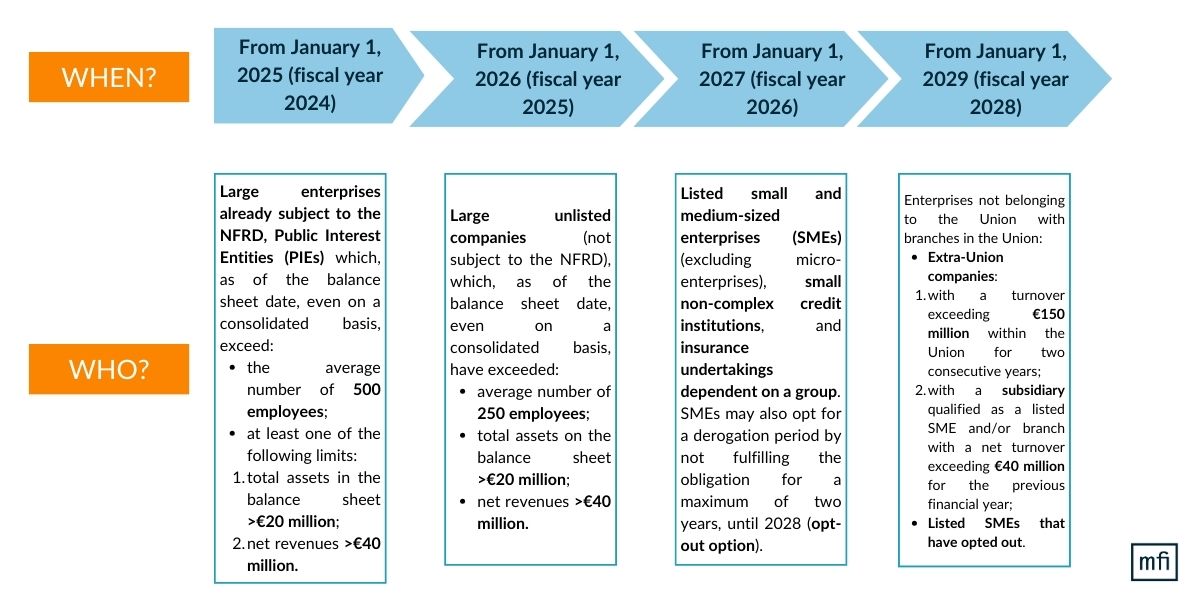

With the adoption of the CSRD by national regulations – mandatory by July 6, 2024 – the number of companies subject to sustainability reporting obligations will significantly increase, following a clear timeline. Below is a detailed breakdown of the identified deadlines, along with the categories of companies involved.

{kind=link}

Lastly, it is important to highlight how CSRD reporting is based on the principle of double materiality, which requires companies to disclose information on both the impact of their activities on the environment and people (inside-out approach) and on how sustainability goals, measures, and risks affect their financial health (outside-in approach). Therefore, a sustainability element becomes relevant for a company when it meets the materiality criteria in terms of both sustainability impact in general and financial impact.

Sustainability Finance Disclosure Regulation (SFDR)

On March 10, 2021, the European Commission’s Regulation (EU) 2019/2988 on the disclosure of sustainability-related information in the financial services sector (SFDR) came into effect, aiming to expand and standardize information on ESG investment processes. The Sustainable Finance Disclosure Regulation is therefore legislation intended to increase transparency in sustainable finance, facilitating the comparison and understanding of how financial products consider environmental and/or social characteristics, as well as how they pursue sustainable investments and objectives. The key actors most affected by the disclosure required by the SFDR are financial market participants, companies offering financial products, and entities that could be the subject of sustainable investments.

The SFDR requires disclosure of policies regarding the integration of sustainability risks and their negative impacts on financial returns. Companies and advisors choosing not to disclose sustainability factors and risks will be required to justify their choices. The Regulation specifies the following:

- sustainability risks refer to environmental, social, or governance events or conditions that could cause a substantial negative impact on the value of an investment

- key negative impacts are all adverse effects that investment decisions or advice could have on sustainability factors.

Furthermore, the Regulation defines sustainable investment, requiring that it:

- contributes to an environmental or social objective

- does not significantly harm any other environmental or social purpose (the “do no significant harm” principle, DNSH)

- respects good governance practices.

Eventually, the SFDR Regulation specifies three distinct categories of ESG products managed by investment firms based in the European Union, whose disclosure is mandatory:

- “Dark green” or Article 9 products: focus on sustainable objectives, aiming to achieve specific sustainability outcomes while maintaining a focus on financial returns

- “Light green” or Article 8 products: emphasize social and/or environmental characteristics and may include sustainable investments, although these are not the primary focus

- “Grey green” or Article 6 products: do not exclusively include sustainability-based screening criteria, thus allowing investments in various sectors.

Each category is required to provide detailed information on investment policies, sustainability indicators used, implementation strategy, and the impact on ESG factors.

When we talk about regulation, it is now inevitable not to mention the role of the European Supervisory Authorities (ESAs), for the ESG sector as well, and in particular ESMA, the European Securities and Markets Authority, which performs supervisory, coordination, and oversight functions in the field of capital markets, supporting sector legislation with the issuance of technical regulatory and implementing standards, as well as opinions and guidelines, functions that, with a different focus, are also proving to be impactful within the ESG world.

In a general perspective, ESMA, through the publication of the Strategy on Sustainable Finance first, and the Sustainable Finance Roadmap 2022-2024 later, has contributed to integrating ESG factors within its scope of action and outlining the fundamental steps towards the creation of actions, rules, and procedures that make the sustainable finance market increasingly transparent to investors, which will have increasingly practical implications, particularly referring to the support functions for the European regulation.

Specifically, when we talk about the sustainability reporting envisaged by the CSRD Directive, ESMA is developing guidelines intended for the supervisory authorities of the member states aimed at establishing common and consistent criteria for effective supervision of listed companies and at the same time aligning financial reporting with non-financial disclosure in a coherent manner.

Ultimately, even though the time is not yet ripe to draw definitive conclusions, from the proposal for a Regulation concerning ESG Ratings (Proposal for a Regulation of the European Parliament and the Council on the transparency and integrity of Environmental, Social and Governance Rating Activities), currently agreed upon by the European Parliament and the Council, it seems that ESMA’s future role as a supervisory authority over ESG Rating providers and as the entity responsible for authorizing them to issue regulated ESG ratings is to be taken for granted, in continuity with what is already provided for in credit rating regulations.

The ESG regulatory landscape is undergoing a phase of profound change, highlighting the urgency for companies to align with sustainability standards. However, the complexity of the directives, coupled with the proliferation of reporting frameworks, underscores the need for greater clarity and coherence. Yet, it seems that we are getting closer and closer.

If you wish to request an ESG rating or simply learn more