In the ongoing global pursuit of sustainable business practices, the significance of Environmental, Social, and Governance (ESG) factors cannot be overstated. These factors have now become central in evaluating the performance and sustainability of companies, particularly small and medium-sized enterprises (SMEs). In this article, we delve into the scoring methodology developed by modefinance for the EE-ESG assessment of SMEs based on the TranspArEEns’ questionnaire data.

TranspArEEns (Mainstream Transparent Assessment of Energy Efficiency In Environmental Social Governance Ratings), is a Horizon 2020 project led by Ca’ Foscari University in Venice, in partnership with modefinance, the EMF-ECBC, the Leibniz Institute for Financial Research SAFE of Frankfurt and CRIF, which has as its aim the mainstreaming of a quali-quantitative framework for standardized collection and analysis of firms’ EE and ESG information and the development of a standardized EE-ESG rating.

modefinance’s data-driven approach to EE-ESG scoring

Our approach to this issue is distinctly data-driven and algorithmic, aligning itself with the latest standards like the European Taxonomy and the Global Reporting Initiative (GRI). It refrains from manual interventions to maintain objectivity and precision. Consequently, the term “EE-ESG score” is preferred over “EE-ESG rating” to distinguish this data-driven evaluation from traditional rating processes.

To enrich its methodology, we introduced benchmarks and logical considerations to mimic the traditional rating process. These supplementary steps are rooted in sustainability thematic areas and guided by our team of ESG analysts.

The core of our methodology lies in data comparison within a peer group. However, it’s crucial to note that the data provided by TranspArEEns is anonymized, focusing on general company information and ESG details. As more data becomes available, the scoring process becomes more precise, reflecting the growing significance of data in ESG assessments.

Our model design encompasses three key elements:

- a KPI dictionary

- an assessment system

- an aggregation function or methodology used to obtain a total EE-ESG evaluation.

{kind=link}

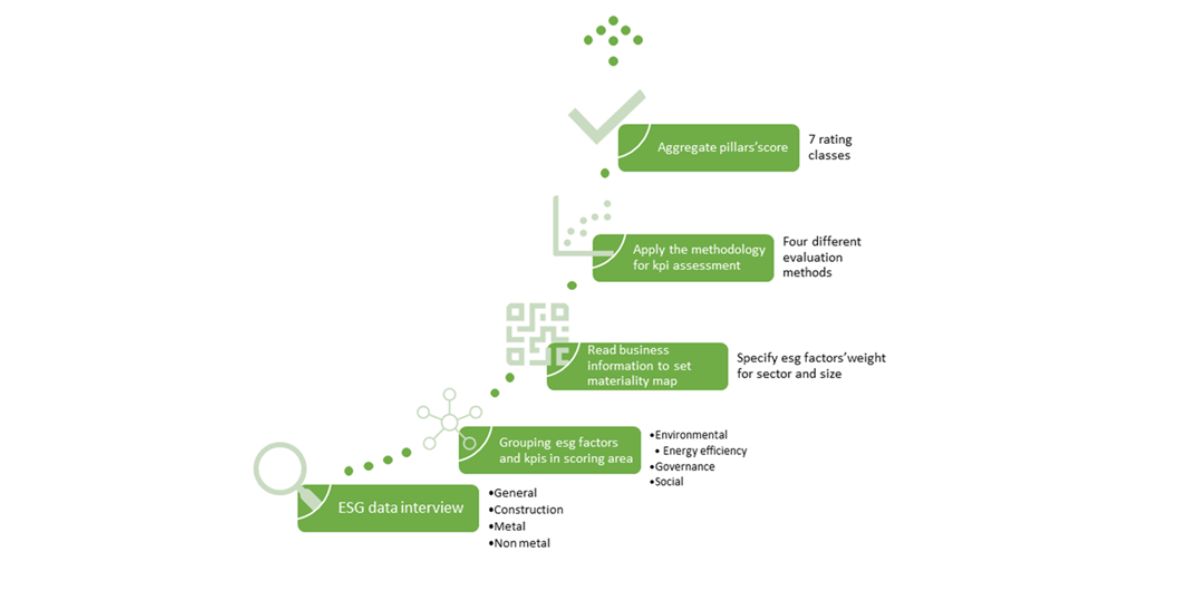

The figure above illustrates the process of EE-ESG scoring release, from the interview to the final evaluation.

The complex world of ESG reporting: challenges and solutions for SMEs

The demand for robust sustainability data has never been higher. However, for companies, especially small and medium-sized enterprises (SMEs), navigating the complex landscape of sustainability reporting can be daunting. In the world of ESG, the adage “more is better” certainly holds, with over six hundred data points available for assessing a company’s ESG profile. Yet, the challenge lies in sorting through this vastity of data to find what truly matters.

For SMEs, the search for sustainable development often involves deciphering the variety of reporting frameworks available. While the European and international stages are adorned with an array of standards, such as TCFD, SASB, UN SDGs, UN PRI, SFRD, GRI, and IFRS, there is no universally adopted framework. The need for a standardized approach has supported the drafting of the Corporate Sustainability Reporting Directive (CSRD) by the European Commission in 2022. It supersedes the Non-Financial Reporting Directive, extending reporting obligations and widening the scope.

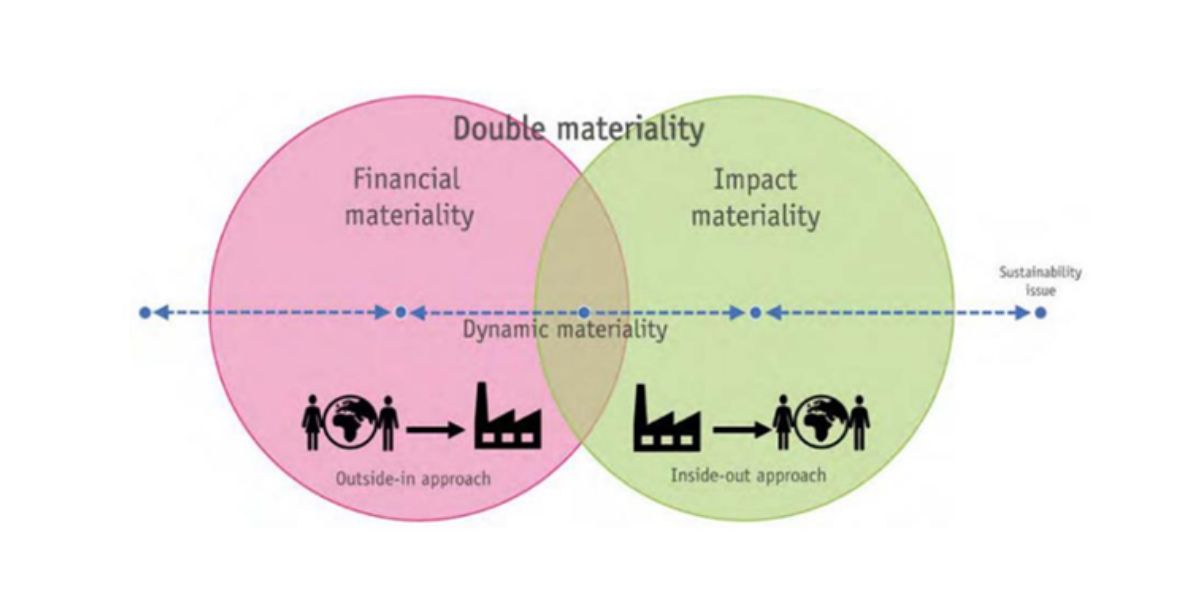

Central to CSRD is the concept of materiality assessment, a key requirement to focus on what is material in terms of ESG risk and opportunities for the company. This analysis is based on the double-materiality or dynamic materiality principle that helps identifying those thematic areas that can have a positive or negative impact on the business of the company (financial materiality) and those that originates from the business that can have an impact outside it (impact materiality), e.g., environment, community, customers, etc.

{kind=link}

Unpacking modefinance’s ESG evaluation model: from KPI dictionary to final EE-ESG Score

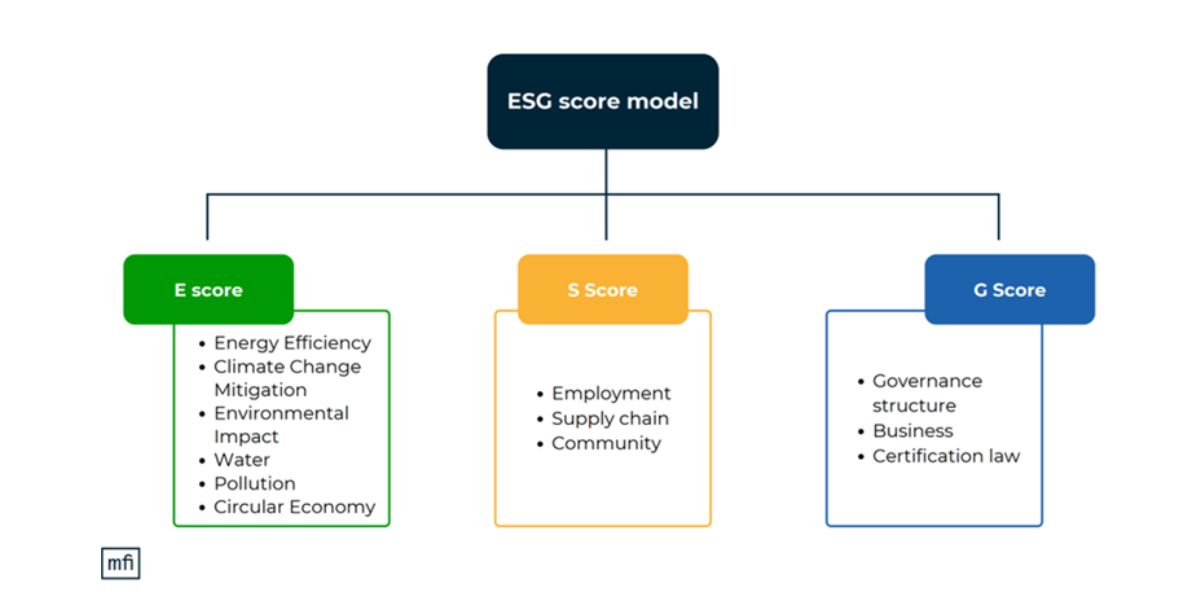

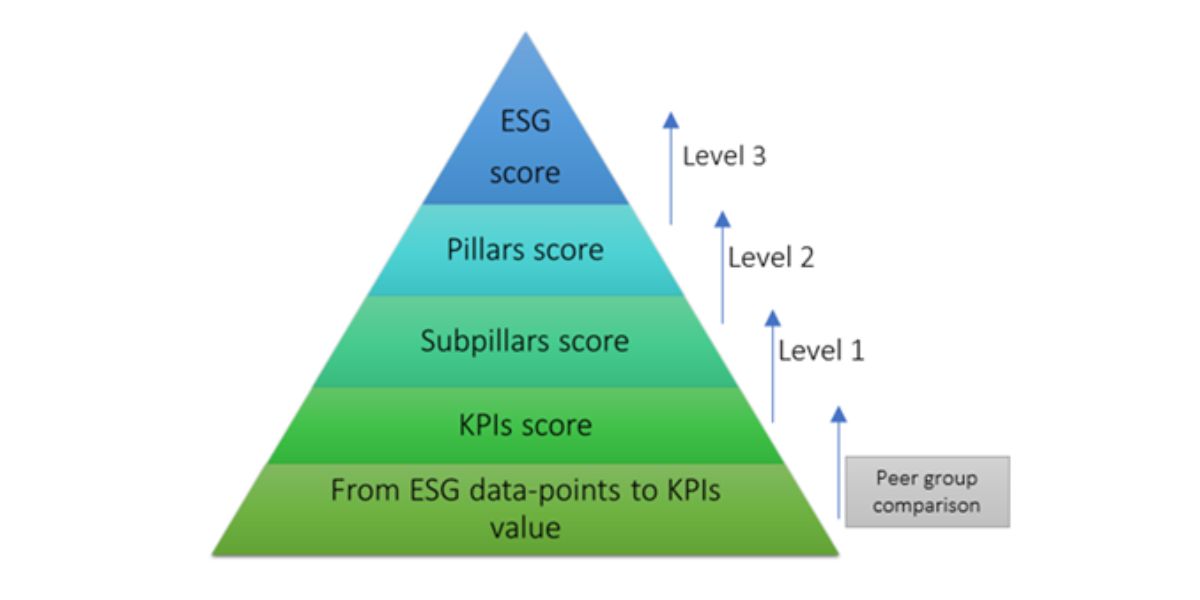

Getting back to the key elements of our ESG evaluation model, the KPI dictionary is constructed based on a questionnaire developed for Italian SMEs, covering various business areas and sustainability dimensions. This comprehensive questionnaire categorizes KPIs into three pillars: Environmental, Social, and Governance, which are further divided into thematic areas or subpillars. The dataset’s size and completeness are crucial for precise evaluations.

{kind=link}

The assessment system leverages these KPIs and their scores to evaluate a company. Various methodologies, including judgmental approaches and peer comparisons, are employed. Peer group compatibility, size, and activity business are all considered for robust evaluations.

The aggregation method combines KPI scores within each thematic area to calculate subpillar scores. Thematic areas are then weighted to produce pillar scores, which are eventually combined to yield the final EE-ESG score.

{kind=link}

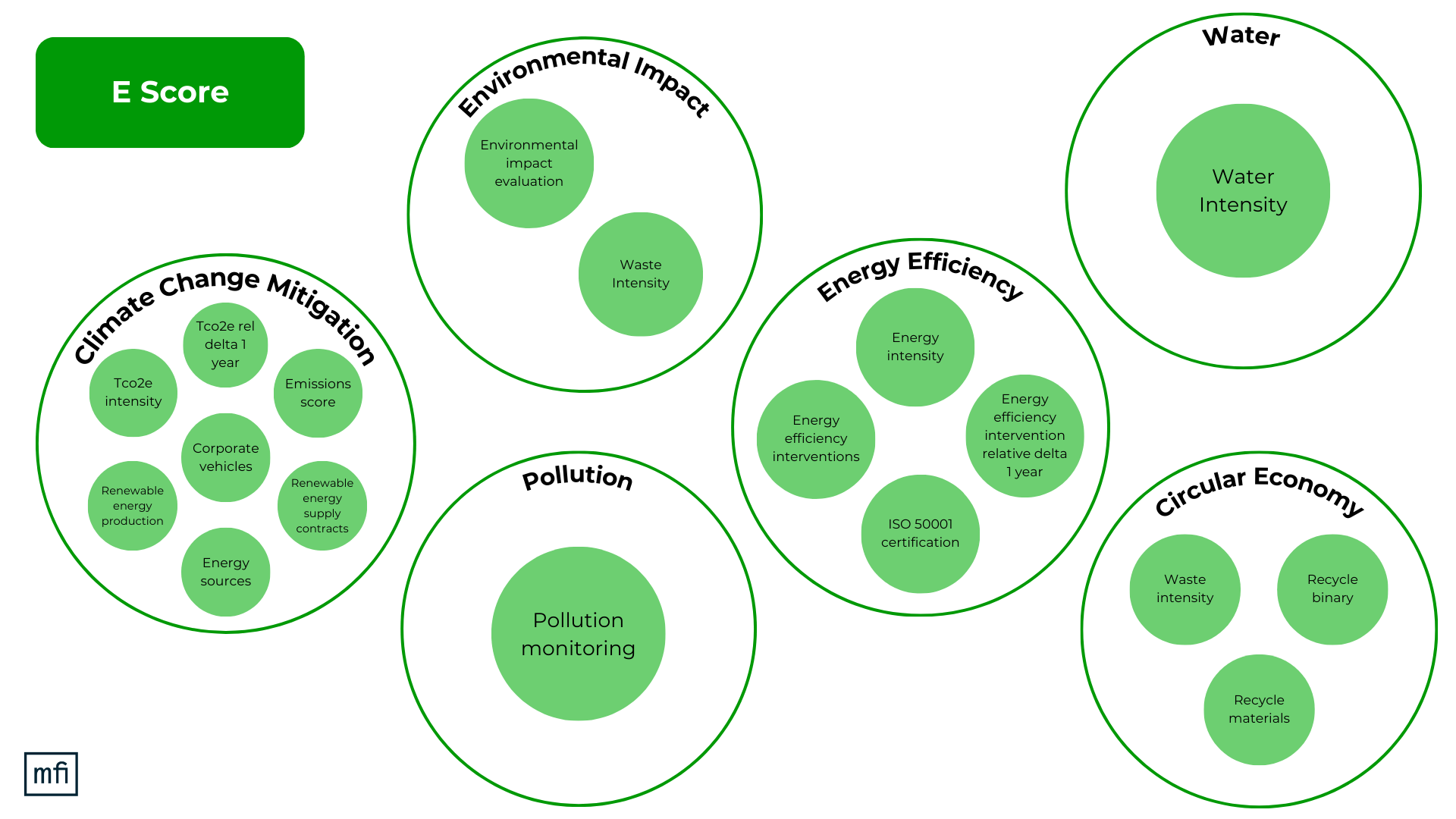

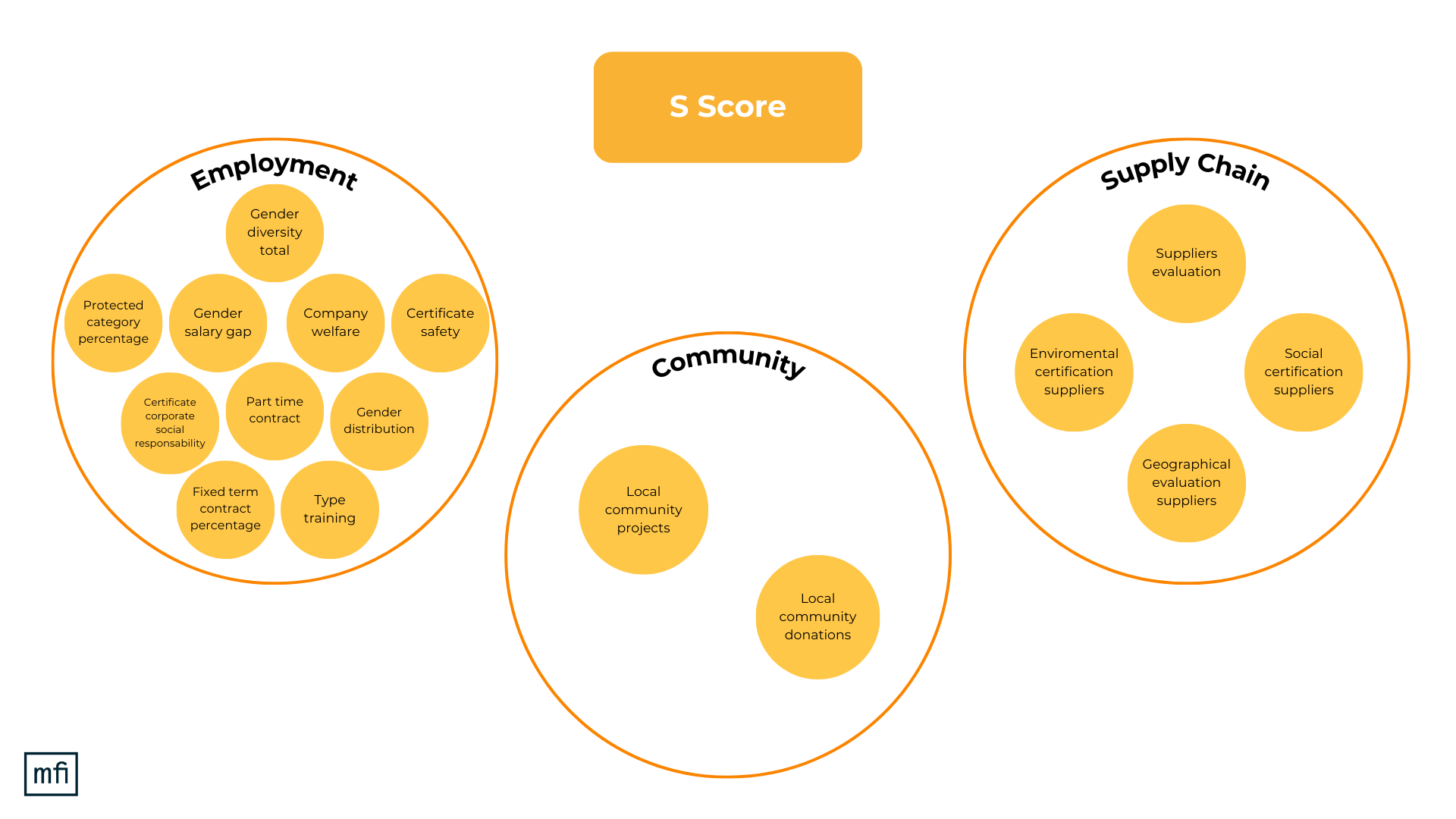

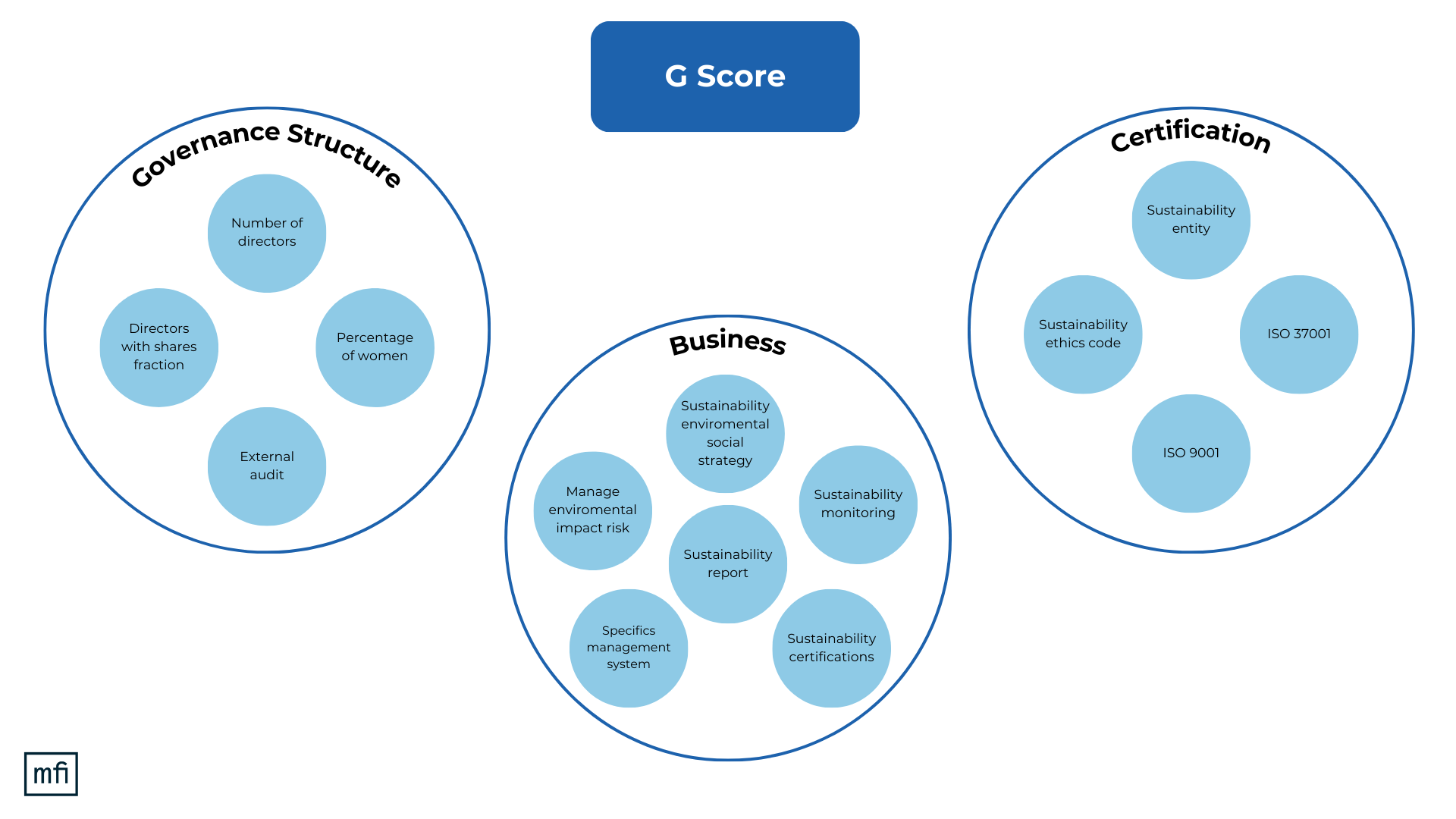

The figures below provide a schematic view of the aggregation process for the sector-agnostic model. Each circle represents a KPI score, and its radius is proportional to the weight applied by the algorithm.

{kind=link}

{kind=link}

{kind=link}

To simplify the overall evaluation process, we use a set of seven different score ranges, from S1 (the best) to S7. These ranges are further categorized into macro-areas: Vulnerable, Responsible, and Dynamic, reflecting a company’s awareness and implementation of ESG policies and practices.

However, the process isn’t devoid of nuance. The release of the ESG final Score-class goes through a so-called override step, obtained by the weighted average, and may undergo variation – downgrade or upgrade – based on a set of rules. The override step is introduced to prevent the company from reaching the best Score-class category (S1, S2) if they have not met the minimum requirement. We identified for each of the pillars E, S and G a driver scoring area, and we set a threshold value for each driver score (Climate Change Mitigation and Energy Efficiency, Supply Chain and Business respectively for Environmental, Social and Governance). If a company does not overcome all these thresholds, it is not eligible for the Dynamic macro-classes (S1, S2). Therefore, those companies that obtain a score S1 and S2 after the Level 3 aggregation will be downgraded to the class S3 if they do not outperform into the driver scoring areas.

In conclusion, our data-driven EE-ESG scoring methodology stands as a powerful tool to assess and enhance the sustainability of SMEs. By aligning with international standards, leveraging data, and introducing nuanced evaluations, we aim to empower these businesses in their journey towards a more sustainable future. As ESG factors continue to gain prominence in the business world, such methodologies play a pivotal role in fostering responsible and sustainable growth for companies of all sizes.