modefinance between the lead partners of the winning project

The project aims to improve the competitiveness of the European Fintech sector introducing a framework for a common regulatory approach across all countries.

modefinance will be one of the very few Fintech companies to take part in the project, which will gather together over than 50 European partners, including:

- some of the major European Universities (the Paris Sorbonne, the Humboldt University of Berlin and the University College London);

- the main Fintech hubs and associations (B-Hive, AFGC, Fintech District, Swiss Fintech Innovations, etc.);

- and all the European regulators and supervisors (ESMA, EBA, EIOPA, Consob, FCA, FCA, AMF, etc.).

Why we need a common regulation?

Financial technologies have strongly developed over the last years, changing the financial world and consumers’ habits. Just think about how cryptocurrencies and peer-to-peer lending (just to mention a few) have changed funding and payment methods: there is a strong need for a common regulatory framework across all the European countries to supervise Fintech companies and technology compliance, protecting consumers and investors from the inherent risks, such as potential for frauds, cyber-attacks or any illegal activity.

There are yet two kind of issues. On one hand, a regulatory framework should be supple enough not to stifle Fintech’s economical potential and fast-growing technologies; on the other side, countries’ regulations should be standardized on a European level, allowing Fintech companies to open up to a wider market. In order to fill this gap, two Fintech branches have been introduced:

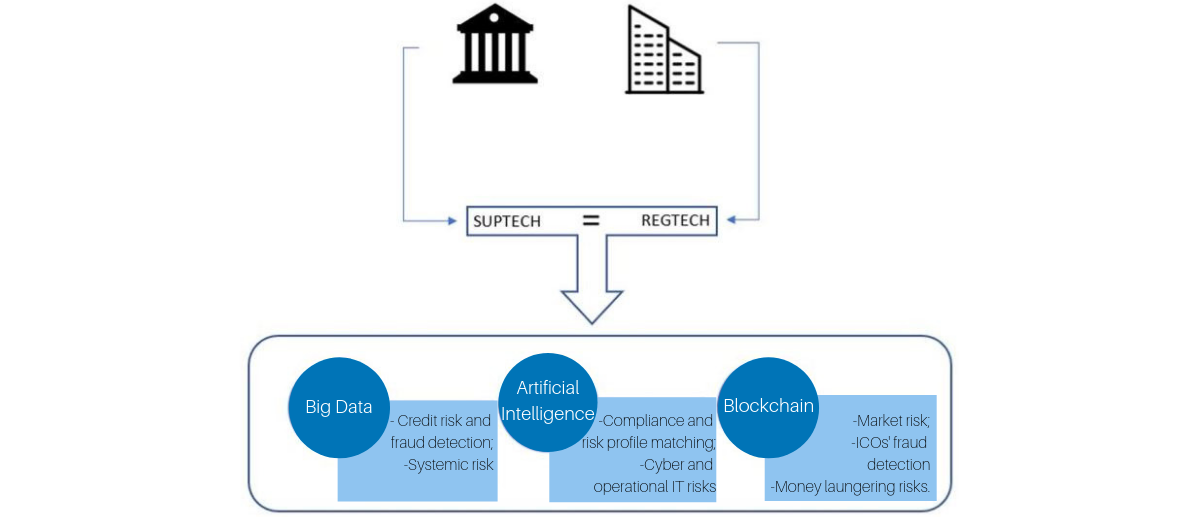

- RegTech (Regulatory Technology), which aims to develop advanced technologies to help companies and organizations comply with different laws and regulations;

- SupTech (Supervisory Technology), i.e. the development of technology solutions that can address problems and challenges faced by supervisors.

{kind=link}

Although these trends started to benefit regulatory and supervisory process, they also remark the need for a joint action. This also means boosting Artificial Intelligence, Big Data Analysis and Blockchain research, which will:

- reduce credit scoring bias and improve fraud detection in peer-to-peer lendingr;

- measure and monitor systemic risk in peer-to-peer lending;

- identify and prioritize cyber risks and IT operational risks in robo-advisory;

- enhance client risk profile matching in robo-advisory;

- identify frauds in ICOs and crypto assets.identify and quantify illegal activities and money laundering.

Over the years 2019-2020 the project will promote research activities in the digital technologies field and will constitute a European training program aimed at providing shared risk management solutions that automatize compliance of Fintech companies and, at the same time, increasing the efficiency of supervisory activities.