Credit limit

It’s been a long time since we first theorized the importance of including client-suppliers relationship data in the evaluation of the trade credit limit. Information such as the number of clients or the payment history are crucial in determining the credit amount to extend to a company.

The same concept was applied to our credit limit assessment model.

In the MORE Credit Limit model, the recommended credit exposure is determined by:

- the company’s creditworthiness (valued with the MORE methodology);

- the average costs a company allocates for suppliers according to its size, the business sector and the country of incorporation.

The model provides an estimation of a company’s credit limit; nevertheless, the suggested credit exposure is calculated on public financials and statistics data only.

Unless the model has been customized.

The model’s customization allows you to exploit your private data on the business relationships to define an accurate credit limit tailored to your risk policies. Let’s see a case study.

A custom model for an unordinary client

In April 2019 modefinance was entrusted with the development of a customized credit limit model.

The client was (and still is) an international bank operating as Export Credit Agency, provides insurance solutions, guarantee and financing to the local export companies.

In such a case, the supplier-client relationship becomes a key variable in the definition of the credit to extend to the exporter. Late or missed payments of the supplying can affect the exporter’s financial health and hence reduce the bank’s probability of credit recovery. Only the analysis of the suppliers’ payment history allows to identify risky transactions.

The model development

In designing the model, we started assessing the credit limit of the client – represented by the importer (buyer) – to determine the credit limit the bank can grant to the suppliers, i.e. the export companies.

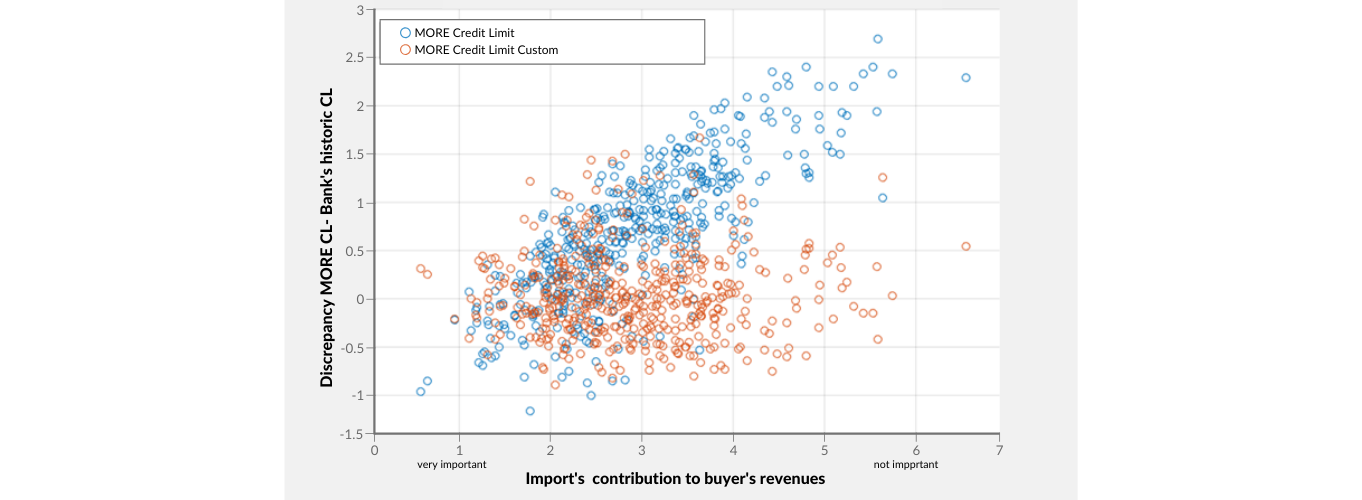

In order to have outcomes tailored to the bank's risk appetite, we first compared the values of the MORE credit limit, calculated on public financial data only, with the historic credit limits accorded by the bank to the same customers.

The comparison showed a discrepancy between the values calculated via MORE and the ones historically granted by the bank. The variable that better explains this discrepancy turned out to be the overall costs of the imported wares on the buyer's revenues.

{kind=link}

The discrepancy between the two values shows in fact an exponential trend: as the import volume increases, so decreases the distance between the MORE credit limit (higher) and the one historically assigned by the bank. The reason is simple: the MORE model assumes each supplier to be strategic for the client’s revenues. The bank, on the other hand, can access companies’ data on the shipments’ volumes and distinguish between major and minor suppliers.

In other words, the more strategic is the amount of import to the buyer revenues, the closer is the bank’s historic credit limit to the MORE values and the higher is the limit that can be ensured to the buyer.

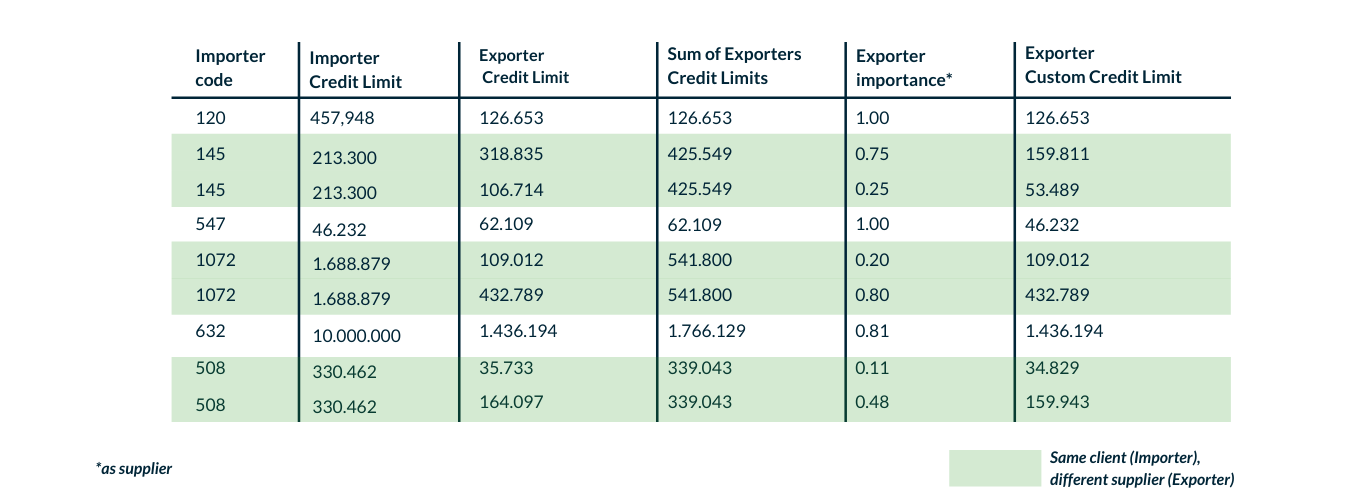

We have therefore adjusted the buyer’s credit limit by including bank’s proprietary data. Finally, we parceled out the credit limit of the import company among the various exporters according to their importance as suppliers, thus determining the credit amount the bank can extend to each of them.

{kind=link}

Benefits of the custom credit limit model

In a nutshell, we can identify three main advantages:

- Thanks to the MORE methodology, the model can assess the creditworthiness and credit limit of both buyers and exporter, automatically and in a few minutes.

- The model takes into account both the strategic importance of the supplier to the customer and vice versa.

- The values of the custom credit limit calculated are in line with the bank’s risk policies and previous assessments.

It’s worth mentioning the MORE Credit Limit model can also assess a company’s credit limit without financials. In this case the model uses qualitative data. We will deepen the topic soon. Or you can already ask for information here.