Burgo Group obtained the certification of its credit management system

{kind=link}

Burgo Group, the Italian paper company headquartered in Altavilla Vicentina, has obtained the certification of its credit management system.

Assisted by the law firm Lexant and the consulting firm Ask Advisory, the corporate has been certified according to the UNI/PdR 44:2018 and the TÜV Rheinland CMC:2012, the standards that internationally define the criteria for credit risks prevention, assessment, and management.

The certification process began in February 2019, as a result of the corporate recovery’s process undertaken in 2016 by the Treasury, Credit, and Insurance Manager Andrea Porelli. It was not an easy situation to manage due to the industry’s hardships and the considerable group's debt exposure. To solve it, Burgo implemented a changeover strategy of its paper mills and a review of its financial management processes, involving modefinance in two projects:

- in the development of a Credit Risk Management platform;

- in the definition of the commercial credit limit to extend to buyers.

The development of the Credit Risk Managment platform

The development of a Credit Risk Management platform stems from Burgo’s need for a credit risk tool for exposure management and monitoring. Burgo Group is Italy's major paper producer and required an integrated system to coordinate the exposures management across all the branches. For its implementation, Burgo Group turned to modefinance; as Fintech's native Rating Agency we could guarantee high-quality risk assessment methodologies as well as the expertise and technologies needed for the development of an advanced platform.

The platform is connected to the main national and international data providers for the download of buyers’ company data and financial statements. It includes several analysis models and tools for risk management and assessment of both specific exposure and entire portfolios. Exposure data conveyed from local branches are automatically updated in less than 24 hours, thanks to the connection with the group's CRM software.

{kind=link}

The credit limit

One of the most helpful analysis models included in the platform is the credit limit calculation model. Within the platform there are two credit limit items: the MORE credit limit and the quantitative credit limit.

The MORE credit limit

The MORE credit limit derives its name from the Artificial Intelligence methodology for credit risk assessment developed by modefinance. The value is determined by the economic-financial soundness of the company and is based on the assumption that Burgo is the strategic supplier for each of its clients. The MORE credit limit is calculated on public data only and guarantees the allocation of a credit limit for each buyer, including prospects for whom the history of the business relationship is not yet available.

The quantitative credit limit

To provide the credit limit of regular and long-standing clients, we also developed a custom credit limit model, the quantitative credit limit. Using internal trade exposure data, the quantitative credit limit analyses the strategic importance of Burgo Group towards its customers and their payment habits, recalibrating the MORE credit limit accordingly. The result is a commercial credit limit assigned both in consideration of the company's creditworthiness and of the commercial relationship between Burgo and the customer.

The qualitative credit limit

If there is no economic and financial data available, Burgo Group can resort to the qualitative credit limit. This model provides a commercial credit limit calculated on the qualitative information available (including the size of the company and the sector to which it belongs) and provides an estimation of the maximum recommended exposure.

Trade credit insurance and discretionary limit

According to the amount suggested by the platform and to credit risk internal policies, Burgo defines the internal credit limit to grant to each buyer in case no credit insurance has been activated.

To further protect the corporate against possible losses, for each new exposure Burgo activates a trade credit insurance, which will set the credit limit within which the insurance company will cover any insolvency of the buyer. Burgo may also agree on a discretionary credit limit, i.e. an amount up to which it may grant credit to the buyer (and obtain insurance coverage) without the prior approval of the insurance company. To extend a discretionary credit limit, Burgo must submit a valid justification. The insurance companies Euler Hermes and Coface, for example, recognize the validity of the commercial credit limit calculated by modefinance as a valid justification for the granting of a discretionary credit limit to the buyer.

Risk management certification

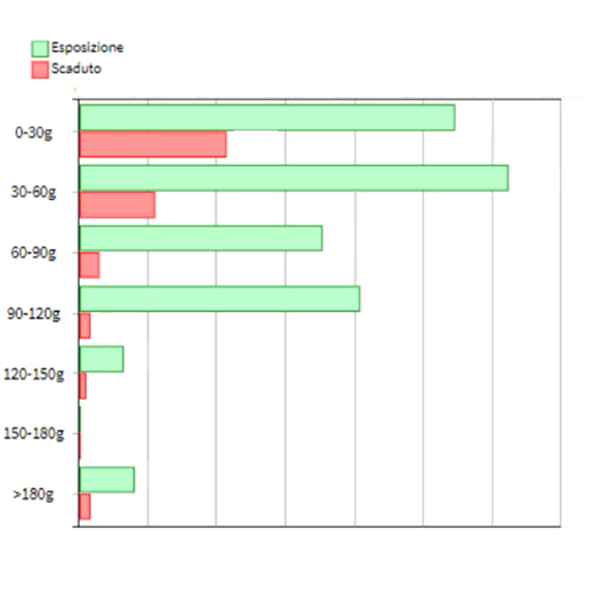

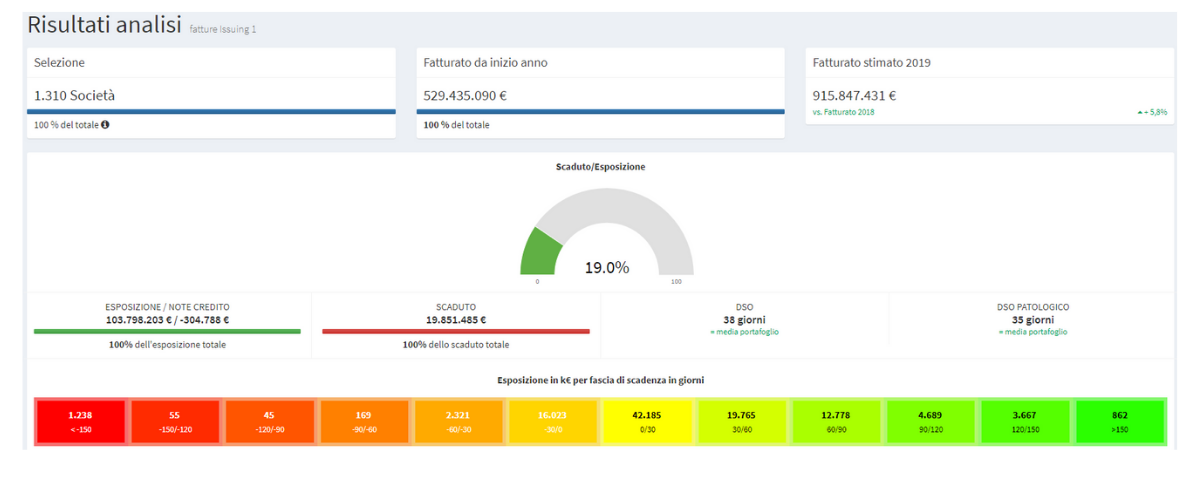

The certification obtained last February by Burgo Group testifies the validity of the new risk management process and of the tools adopted. But even more importantly, it was the results obtained by Burgo in recent years that highlighted the success of the new management. In a short time, Burgo has managed to reduce losses on trade receivables, cut the overdue invoices, and optimize working capital management. Today the group has recovered and can face the difficulties generated by the current crisis with an adequate management structure.