modefinance Unsolicited Corporate Credit Rating for GIORGIO ARMANI S.P.A.: B1(Downgrade)

modefinance published the Unsolicited Corporate Credit Rating of GIORGIO ARMANI S.P.A. on its CRA website, reviewed after the publication of the 2019 financial statement, and the rating assigned to the entity is B1 (Downgrade). The analysis revealed that the company has an average capability of repaying financial obligations and possibile adverse macroeconomic conditions or different management or strategies might impact on the capacity of repaying debt.

Giorgio Armani S.p.A. is a leading company in the fashion and luxury industry.

Key Rating Assumptions

Giorgio Armani S.p.A. is a long-established company founded in 1975, and it is the parent company of a solid international group. The Group includes 17 subsidiaries and 531 directly managed stores all over the world, with a total of 8,973 employees. The GUO of Giorgio Armani S.p.A. is Mr. Giorgio Armani. Despite being almost entirely family-owned, the Company has so far been well managed. The group appears sound since most of the subsidiaries have a good level of creditworthiness.

The overall financial and economic situation of Giorgio Armani S.p.A. in 2019 was good. The Company confirmed its excellent condition of solvency and the adequate liquidity condition but recorded a contraction in profitability, mostly related to the instruction of the IFRS16, which substantially reduced profit for period. No black records have been found.

Comparing Giorgio Armani S.p.A. with its peer group, it emerges that the Italian fashion house is well positioned in terms of turnover and presents an excellent solvency level but performs poorly in terms of profitability.

Regarding the sector, the personal luxury goods industry, as all business segments, has been impacted by the sanitary emergency related to Covid-19. The True- Luxury Global Consumer Insight report predicts a drop in sales of personal luxury products between -25% and -45% in 2020, while the estimates that concern the experiential luxury, which has grown the most in the last three years, fluctuate between -40% and -60%. The return to 2019 levels (in absolute value) is expected in 2022 or 2023.

As regards the macroeconomic situation, all the countries that most influence the Group’s performance, except for China, are expected to suffer a recession in 2020 due to the spread of COVID-19. Although a slight recovery is forecasted for the next year, in many countries the output at the end of 2021 will still be below levels at the 2019 levels and below what was expected before the sanitary emergency. Risks and uncertainty remain high and the outlook will depend on the virus, policies, people’s behavior, and confidence.

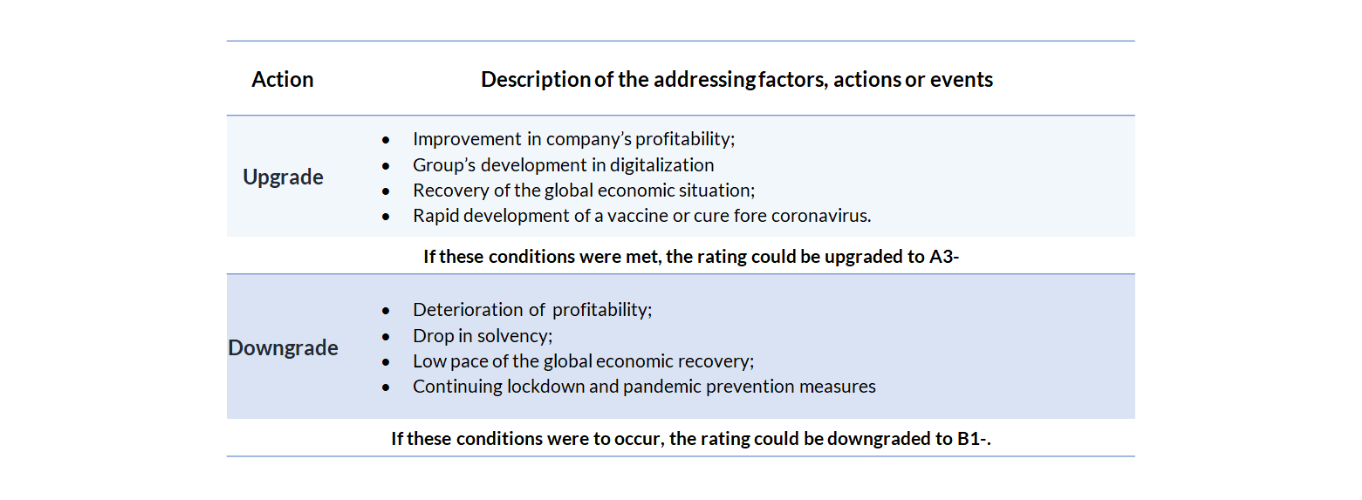

The following table summarizes the addressing factors, actions or events that could lead to a rating upgrade or downgrade:

{kind=link}

Important

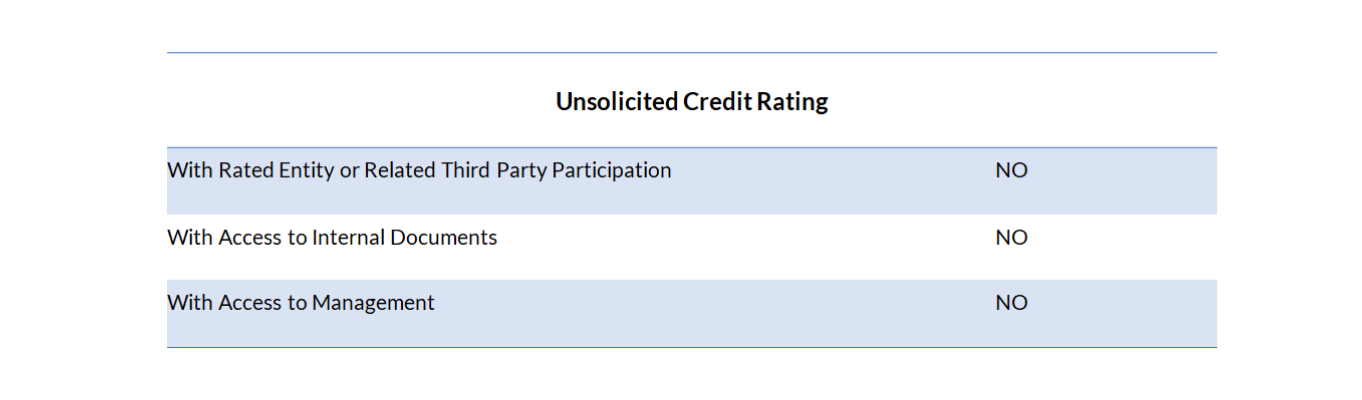

The present Corporate Credit rating is issued by modefinance under EU Regulation 1060/2009 and following amendments. The present rating is unsolicited: the rated entity and/or related third parties have not participated in the rating process and modefinance has no access to accounts or other relevant internal documents of the rated entity and/or related third parties.

{kind=link}

Solicited and unsolicited ratings issued by modefinance are of comparable quality, as the solicitation status does not affect the methodologies used. More comprehensive information on modefinance Corporate Credit Ratings is available at cra.modefinance.com.

The present Corporate Credit Rating is issued on MORE Methodology 2.0 and Rating Methodology 1.0.

For information on historical default rates of modefinance Corporate Credit Ratings please refer to ESMA Central Repository and ESMA European Rating Platform.

modefinance refers to default as a company under bankruptcy, or under liquidation status, or under administration or for which missed payments on a financial obligation are officially recorded.

The quality of the information available on the rated entity and used to determine the present rating was judged by modefinance as satisfactory. Please note that modefinance, however, is not in a position to guarantee the accuracy of that information. As such, modefinance can accept no liability whatsoever for actions taken based on any information that may subsequently prove to be incorrect.

The present credit rating was notified to the rated entity in order to identify potential factual errors, as prescribed by the CRA Regulation.

No amendments were applied after the notification process.

The Rated Entity or Related Third Party has not purchased ancillary services from modefinance.

The rating action issued by modefinance was performed independently. The analysts, members of the rating team involved in the process, modefinance Srl and its members and shareholders do not have any conflicts of interest concearning the Rated Entity and/or Related Third Parties. If in the future a potential conflict of interest related to the persons reported above is identified, modefinance Ratings will provide the appropriate information and if necessary the rating will be withdrawn.

The present Credit Rating is an opinion of the general creditworthiness that modefinance issues on the rated entity, and should be relied upon to a limited degree. The issued rating is subject to ongoing monitoring until withdrawal.

Contacts

Head Analyst – Giulia Valentina Facchini

giulia.facchini@modefinance.com

+39 040 3756742

Assistant Analyst – Eva Vocci

eva.vocci@modefinance.com

+39 040 3756742

Responsible for Rating Approval – Pinar Dilek (Rating Process Manager)

pinar.dilek@modefinance.com

+39 040 3756740