modefinance can estimate the impact of COVID-19 on companies’ performances

The outbreak of Coronavirus in Italy continues to raise concern. To contain the spreading of the virus, the Italian Government has taken severe measures that strongly restrict commercial activities, causing an unavoidable contraction on companies’ sales revenues. At this stage, it’s hard to predict how long the emergency will last and the impact it will have on the real economy and international financial markets.

Along with macroeconomic considerations, it’s now necessary to forecast the impact it will have on every single company and its supply chain, allowing entrepreneurs to review their business and credit strategy to limit damages. Through the Forecasting-StressTest analysis model (For-ST), modefinance can estimate the impact of COVID-19 on companies’ performances according to 3 different scenarios (positive, neutral and negative) and simulate how it will affect their creditworthiness and probability of default (PD).

The Forecasting-StressTest model (For-ST)

For-ST is an analysis tool designed to process budget simulations and stress testing scenarios within the Rating-as-a-Service platform developed by modefinance.

The model runs both historical and statistical information. Artificial Intelligence algorithms group companies with significant common features into clusters and determine the most likely future behavior of the analyzed company according to its size, industry, location, creditworthiness and economic and financial history.

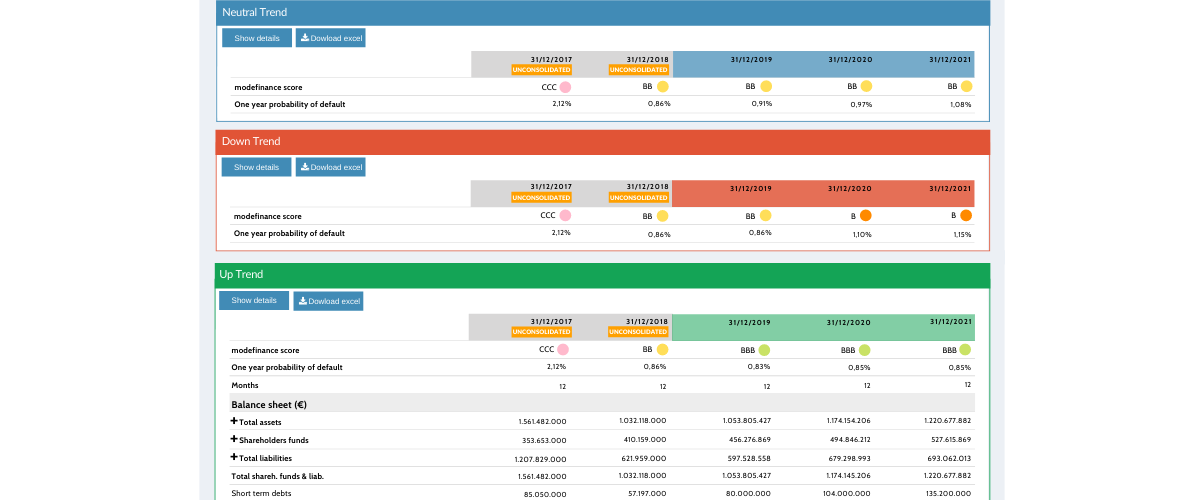

For-ST can forecast the company’s performances over 5 years according to 3 different scenarios.

{kind=link}

The model forecasts costs and revenues and uses this data to determine the cash cycle. Then it estimates working-capital and assets, from which it derives amortizations, EBIT, and the all income statement. Through the latter, it estimates the shareholders' equity.

The result is a simulation of a complete balance sheet, from which the model calculates the probability of default and the creditworthiness of the company.

For-ST also shows which scenario best reflects the company’s most likely future performances. The degree of accuracy of the simulations is 81.3%.

{kind=link}

Stress Test

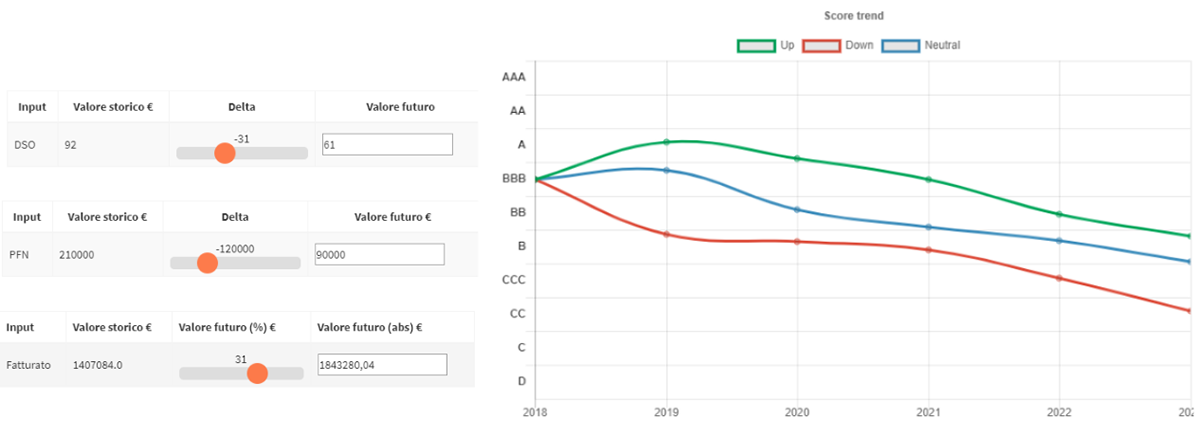

The model also allows you to perform stress tests on key variables: sales, short and long term liabilities, EBITDA, DPO, DSO, and DIO.

{kind=link}

By changing the value of these variables, you can stress test the company’s performance. As the COVID-19 emergency will first result in a decrease in sales, by changing the values of the corresponding variable you can verify the impact of a drop in sales on the company's probability of default.

Case study: effects of COVID-19 on a portfolio

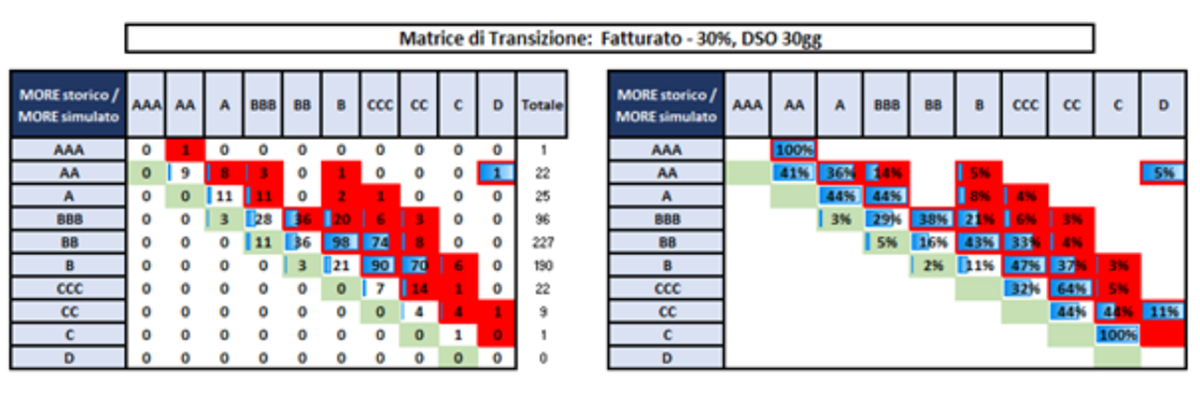

Likewise, modefinance performed a simulation of the effect of Coronavirus on a target portfolio. The analysis envisages three scenarios, with a 10%, 20%, and 30% drop in turnover and an additional 30-day delay on the historical DSO value of each company.

The image below shows the distribution of the companies in the portfolio per credit score (MORE) according to the three scenarios. Blue shows the current companies’ distribution, red the simulated scenarios.

{kind=link}

The analysis revealed the stronger the decrease in sales revenues, the more marked is the shift of the companies towards the lower classes (CCC, B).

All three scenarios highlight a sharp increase in the portfolio’s probability of default: in particular, the assumption of an extreme contraction in companies' turnover would lead to an increase of the portfolio’s probability of default of 8.3%.

{kind=link}

For-ST within the Rating-as-a-Service Plaform

For-ST is a versatile tool that allows you to:

- Perform stress test on specific portfolio;

- Estimate the debt capacity of a company in a few seconds;

- Simulate how a delay in the cash cycle can affect the economical and financial health of a company or an entire business sector.

- Analyze how a hurdle in the supply chain can affect the entire production.

For-ST is embedded in modefinance's Rating-as-a-Service platform. The outcomes of the simulations are integrated in a fully automated framework that allows users to perform credit risk analysis in a few minutes. The platform provides a powerful array of analysis tools (such as the massive analysis tool or the qualitative analysis tool) that allow users to build a rating process completely customized to their needs.