Solicited Corporate Credit Rating for ITALIA POWER SPA: B1+ (Upgrade)

modefinance published the Solicited Corporate Credit Rating of ITALIA POWER S.P.A. on the website and the rating assigned to the entity is B1+ (Upgrade). The analysis revealed it is an adequate company with average capability of repaying financial obligations and it is little affected by adverse economic scenarios.

ITALIA POWER S.P.A. is an Italian energy sector’s company since 2016 and, over its first six years of life, has developed a marked lateral diversification, expanding its business to energy efficiency, marketing of products related to green mobility, mobile telephony, and clothing. The Company’s fast strategic expansion makes it one of the leading ESCo Utilities in Southern Italy.

Key Rating Assumptions

The Company confirms the appreciable economic and financial situation, characterized by a capital endowment capable of covering existing risks without massive recourse to financial debt. The financial balance is confirmed as adequate from a static point of view, while from a more dynamic side, there is an increase in tax receivables to be considered consistent with the growth of operations in the energy efficiency sector. Moreover, lateral diversification continues to ensure sustained profitability. Cash and cash equivalents express a contraction, having been impacted by both new investments and the performance of working capital, which is affected by the aforementioned growth in tax receivables.

The management of credit lines is confirmed to be correct, being characterized by punctuality in payments and the absence of financial tension.

The governance and control system confirm their solidity, with the internal bodies having a collegial form and being supported in their work by an auditing company voluntarily appointed by the Company. Moreover, the Company adopts the organizational model ex-231/2001 and confirms the presence of a supervisory body.

Comparing the Company’s health with the reference peer group, it is possible to note an appreciable positioning in terms of size and profitability; the performance in terms of solvency is also largely sufficient. The peer group expresses an adequate trend in all areas of analysis examined.

Italy’s energy sector has been affected by recent geopolitical tensions, which have led to a rise in energy commodity prices and the need for the national government to diversify its sources of supply. The situation seems to have eased over the past few weeks, with a return to lower prices and greater diversification of production sources. This has led to a revision of the medium/long-term outlook, which is now showing appreciable recovery.

The Italian macroeconomic situation shows modest growth, with rising interest rates, high inflation and unfavorable international scenario as factors of uncertainty, countered by strengthened political stability. The macroeconomic forecast data could be revised upward.

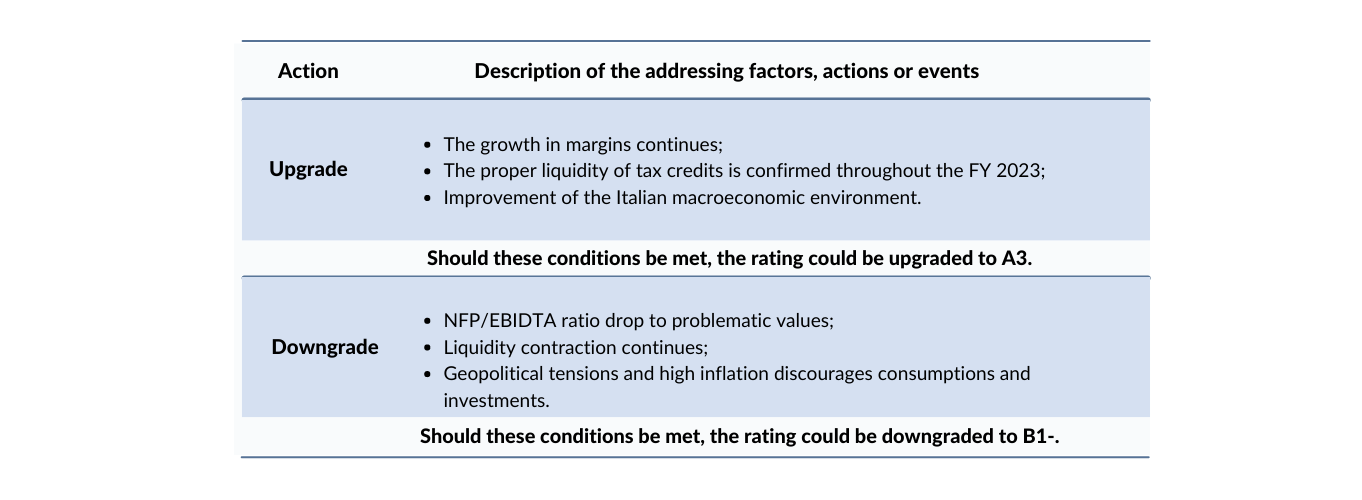

Sensitivity Analysis

In the following table, the addressing factors, actions or events that could lead to an upgrade or a downgrade are summarized:

{kind=link}

Important

The present Corporate Credit rating is issued by modefinance under EU Regulation 1060/2009 and following amendments.

The present rating is solicited and is based on both private and public information. The rated entity and/or related third parties have provided all private information used. modefinance had access to some accounts and other relevant internal documents of the rated entity and/or related third parties. Solicited and unsolicited ratings issued by modefinance are of comparable quality, as the solicitation status has no effect on methodologies used. More comprehensive information on modefinance Corporate Credit Ratings are available at http://cra.modefinance.com/en

The present Corporate Credit Rating is issued on MORE Methodology 2.0 and Rating Methodology 1.0. A comprehensive description of both methodologies, as well as information on modefinance Rating Scale and Mappings, is available at http://cra.modefinance.com/en/methodologies.

For information on historical default rates of modefinance Corporate Credit Ratings please refer to ESMA Central Repository and ESMA European Rating Platform.

modefinance refers to default as a company under bankruptcy, or under liquidation status, or under administration or for which missed payments on a financial obligation are officially recorded.

The quality of the information available on the rated entity and used to determine the present rating was judged by modefinance as satisfactory. Please note that modefinance does not perform any audit activity and is not in a position to guarantee the accuracy of any information used and/or reported in the present document. As such, modefinance can accept no liability whatsoever for actions taken based on any information that may subsequently prove to be incorrect.

The present credit rating was notified to the rated entity in order to identify potential factual errors, as prescribed by the CRA Regulation.

No amendments were applied after the notification process.

The rated entity is not a buyer of ancillary services provided by modefinance.

The rating action issued by modefinance was performed independently. The analysts, members of the rating team involved in the process, modefinance Srl and its members and shareholders do not have any conflicts of interest in relation to the Rated Entity and/or Related Third Parties. If in the future a potential conflict of interest is identified in relation to the persons reported above, modefinance Ratings will provide the appropriate information and if necessary the rating will be withdrawn.

The present Credit Rating is an opinion of the general creditworthiness that modefinance issues on the rated entity, and should be relied upon to a limited degree. The issued rating is subject to an ongoing monitoring until withdrawal.

Contacts

Head Analyst - Christian Raimondo, Rating Analyst

christian.raimondo@modefinance.com

Responsible for Rating Approval - Pinar Dilek, Rating Process Manager

pinar.dilek@modefinance.com