Solicited Corporate Credit Rating for PASOLINI LUIGI SRL: B1- (First Issuance)

modefinance published the Solicited Corporate Credit Rating of PASOLINI LUIGI SRL on the CRA website and the rating assigned to the entity is B1-(first issuance). The analysis revealed that the Company has an adequate economic and financial situation and can face adverse economic conditions in the medium and long term.

PASOLINI LUIGI S.R.L. operates in creating exhibition and communication solutions for retail points of sale. The company is currently a significant reference point for Large-Scale Retail Distribution chains thanks to its ability to offer effective and innovative exhibition solutions. Since 2020, the company has taken on the role of a general contractor for consultancy, conception, design, and turnkey set-up of retail points of sale, aligning them with the different corporate profiles and images, thus becoming the sole interlocutor for the supply and set-up of sales and consumption areas.

Key Rating Assumptions

The Company presents an adequate economic and financial situation characterized by a steady growth in revenue, which positively reflects on operating margins and profitability indicators. The capitalization is consistent with the Company'’s activities and the sources of financing used. The improvement in gross operating margins ensures debt sustainability without critical issues. The management of the relationship between short-term investments and sources is substantially balanced between current assets and current liabilities.

The cash flows analysis confirms the Company’s ability to generate resources through income flows and adequate management of working capital dynamics.

During the financial period, the company has reduced its reliance on financial debt, which shows no critical issues, as highlighted by the analysis of the Italian Central Credit Register.

The governance structure is appropriate for the Company's size. The administrative body is composed of the two majority shareholders flanked by a single-member control body. As of 2023, the company has adopted the Organizational Model pursuant to 231/2001 regulation.The company's shareholding consists of the shareholders Giacomo Pasolini and Pierpaolo Pasolini, and the company Athena Financial Advisory S.r.l., the latter acting as a financial support partner.

The company holds a remarkable positioning in terms of revenue, ranking just below the 90th percentile compared to the analyzed sample. However, the profitability performance is more contained, aligning with the median value of the sector despite a significant increase in margins. The peer group exhibits adequate levels of solvency, liquidity, and profitability. Moreover, the distribution of companies in the sector shows a concentration of enterprises above the threshold of sufficiency, emphasizing the overall health of the peer group.

The retail industry in Italy is weakened by ongoing strong inflationary dynamics. The generalized price increase has led consumers to adjust their purchasing choices, resulting in a reduction in shopping cart spending.

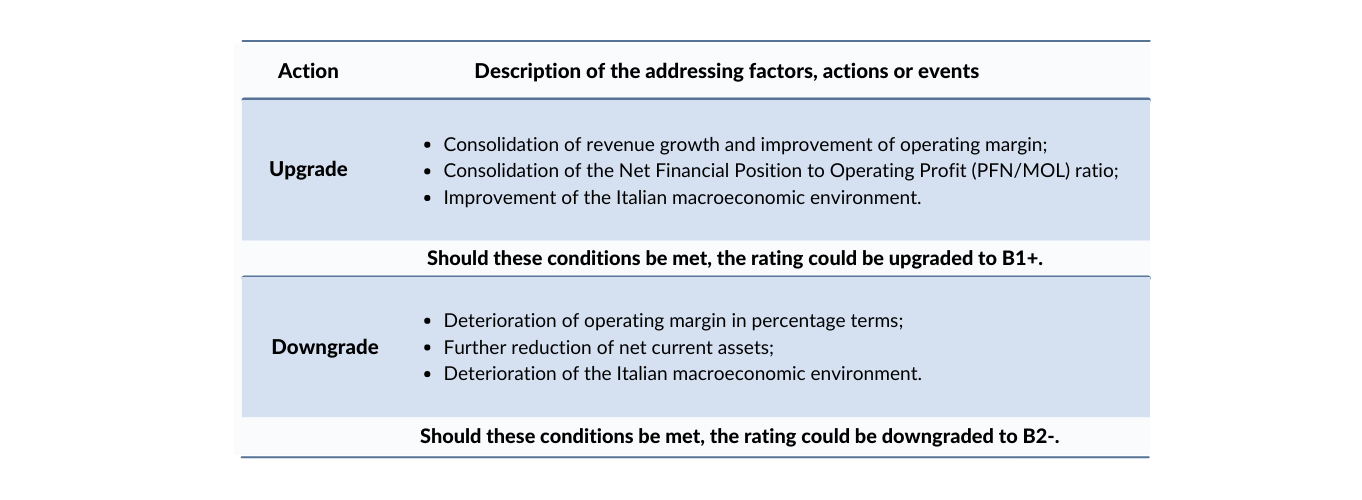

Sensitivity Analysis

{kind=link}

Important

The present Corporate Credit rating is issued by modefinance under EU Regulation 1060/2009 and following amendments.

The present rating is solicited and is based on both private and public information. The rated entity and/or related third parties have provided all private information used. modefinance had access to some accounts and other relevant internal documents of the rated entity and/or related third parties. Solicited and unsolicited ratings issued by modefinance are of comparable quality, as the solicitation status has no effect on methodologies used. More comprehensive information on modefinance Corporate Credit Ratings are available at http://cra.modefinance.com/en

The present Corporate Credit Rating is issued on MORE Methodology 2.0 and Rating Methodology 1.0. A comprehensive description of both methodologies, as well as information on modefinance Rating Scale and Mappings, is available at http://cra.modefinance.com/en/methodologies.

For information on historical default rates of modefinance Corporate Credit Ratings please refer to ESMA Central Repository and ESMA European Rating Platform.

modefinance refers to default as a company under bankruptcy, or under liquidation status, or under administration or for which missed payments on a financial obligation are officially recorded.

The quality of the information available on the rated entity and used to determine the present rating was judged by modefinance as satisfactory. Please note that modefinance does not perform any audit activity and is not in a position to guarantee the accuracy of any information used and/or reported in the present document. As such, modefinance can accept no liability whatsoever for actions taken based on any information that may subsequently prove to be incorrect.

The present credit rating was notified to the rated entity in order to identify potential factual errors, as prescribed by the CRA Regulation.

No amendments were applied after the notification process.

The rated entity is a buyer of ancillary services provided by modefinance (private corporate rating). modefinance ensures that such situation does not imply a conflict of interest in the issuance of the present credit rating.

The rating action issued by modefinance was performed independently. The analysts, members of the rating team involved in the process, modefinance Srl and its members and shareholders do not have any conflicts of interest in relation to the Rated Entity and/or Related Third Parties. If in the future a potential conflict of interest is identified in relation to the persons reported above, modefinance Ratings will provide the appropriate information and if necessary the rating will be withdrawn.

The present Credit Rating is an opinion of the general creditworthiness that modefinance issues on the rated entity, and should be relied upon to a limited degree. The issued rating is subject to an ongoing monitoring until withdrawal.

Contacts

Head Analyst - Gabriele Fadon, Rating Analyst

garbiele.fadon@modefinance.com

Responsible for Rating Approval - Pinar Dilek, Rating Process Manager

pinar.dilek@modefinance.com