modefinance Unsolicited Corporate Credit Rating for BARILLA INIZIATIVE S.P.A.: A3 (Downgrade)

modefinance published the Unsolicited Corporate Credit Rating (Downgrade) of BARILLA INIZIATIVE S.P.A. on its CRA website and the rating assigned to the entity is A3.

The analysis revealed that the company has good capabilities of repaying financial obligations and very low dependence on possibile adverse macroeconomic conditions.

Reason for review: publication of 2019 annual account.

Key Rating Assumption

The reasons that have driven this decision are:

- The overall financial and economic situation of Barilla Group is good in all the analyzed areas and follows a constant trend over the years. Solvency is very good, and both liquidity and profitability level are adequate. Despite the tougher and fragile economic scenario, the Group managed to reach a growth in operating sales also in 2019. During 2019, Barilla Group recorded a positive change in cash and cash equivalent of +113 million Euro, while in 2018 it was of 50 million euro. Operating cash flow, thanks to the high self-financing capacity, is very positive and sufficient enough to totally finance both investing and financing activities. Closing cash reached an elevated value and complies with the Group’s intention of continuing its investment strategy.

- The Group is well positioned in terms of turnover where it is ranked at the 100th percentile of the peer group’s distribution. Founded in 1877, Barilla is a well-established and well-diversified company that operates in 26 countries. Barilla Group is also sound: both the parent company and the consolidated ones achieved positive results , as most of the subsidiaries recorded adequate MORE Score classes.

- From January 2020, the global scenario has been characterized by the health emergency triggered by the outbreak of the Coronavirus and by the consequent restrictive measures for its containment put in place by the public authorities of the hitten countries. The lockdown applied by many countries around the world generated unprecedented economic and social damage. Traditionally, the food sector remains almost immune to the volatility of the other production sectors, due to the lower variability of food consumption. However, these global circumstances have direct and indirect impacts on the Group’s economic activity, creating a context of general uncertainty, the evolution of which is not foreseeable.

- In the agri-food sector, throughout the lockdown, companies as Barilla ensured the food production and distribution to guarantee the supply to supermarkets and points of sale. However, the impact that the coronavirus emergency, and the consequent restrictive policies implemented by governments, will have on agro-food sector remain uncertain. A drop in export of agri-food product is expected, attributable to the slowdown in road transport, the overall increase in production costs, the drop on demand from international hospitality sector and the new customs duties imposed by US on products coming from EU. On the other hand, there is an increase in domestic demand, partly due to the difficulties in provisioning from abroad together with counsumer’s increased attention to food safety.

- For Italy, a tiring recovery is expected after the collapse caused by the coronavirus emergency; investments and exports are suffering even more than consumption. The Italian government is devising different measures to support production activities, citizens and families, however the situation is still evolving and undefined.

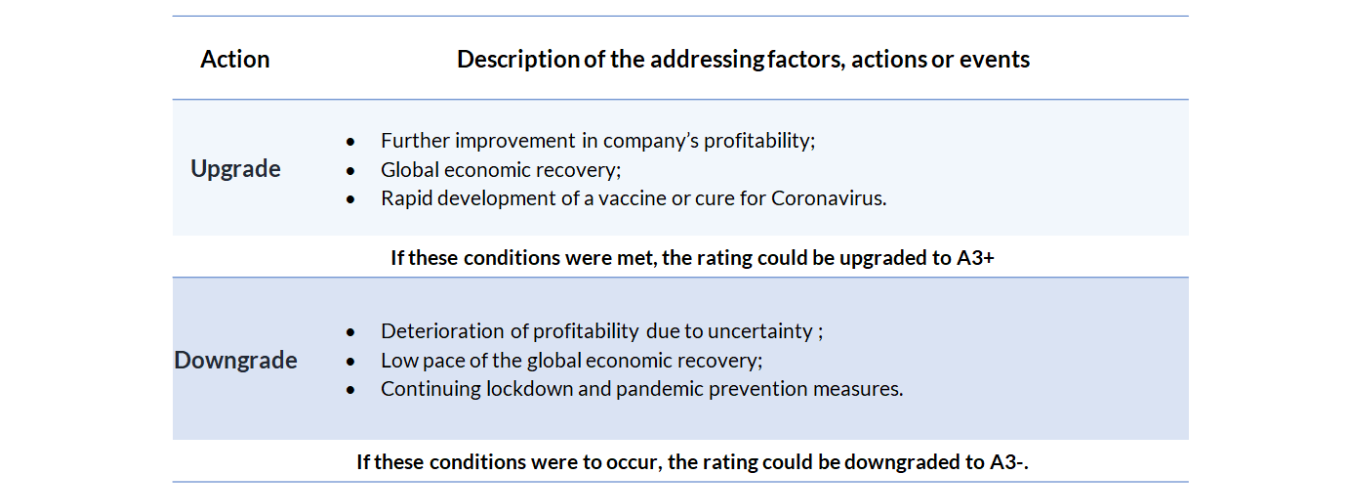

Sensitivity Analysis

The following table summarizes the addressing factors, actions or events that could lead to a rating upgrade or downgrade:

{kind=link}

Important

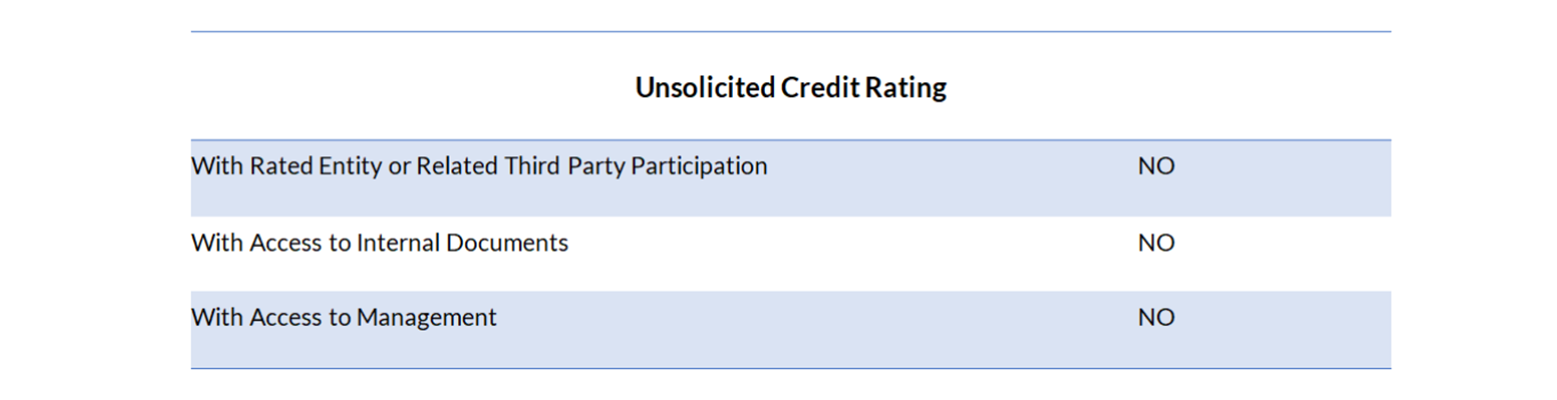

The present Corporate Credit rating is issued by modefinance under EU Regulation 1060/2009 and following amendments. The present rating is unsolicited: the rated entity and/or related third parties have not participated in the rating process and modefinance has no access to accounts or other relevant internal documents of the rated entity and/or related third parties.

{kind=link}

Solicited and unsolicited ratings issued by modefinance are of comparable quality, as the solicitation status does not affect the methodologies used. More comprehensive information on modefinance Corporate Credit Ratings is available on the CRA website.

The present Corporate Credit Rating is issued on MORE Methodology 2.0 and Rating Methodology 1.0.

For information on historical default rates of modefinance Corporate Credit Ratings please refer to ESMA Central Repository and ESMA European Rating Platform.

modefinance refers to default as a company under bankruptcy, or under liquidation status, or under administration or for which missed payments on a financial obligation are officially recorded.

The quality of the information available on the rated entity and used to determine the present rating was judged by modefinance as satisfactory. Please note that modefinance, however, is not in a position to guarantee the accuracy of that information. As such, modefinance can accept no liability whatsoever for actions taken based on any information that may subsequently prove to be incorrect.

The present credit rating was notified to the rated entity in order to identify potential factual errors, as prescribed by the CRA Regulation.

No amendments were applied after the notification process.

The Rated Entity or Related Third Party has not purchased ancillary services from modefinance.

The rating action issued by modefinance was performed independently. The analysts, members of the rating team involved in the process, modefinance Srl and its members and shareholders do not have any conflicts of interest concearning the Rated Entity and/or Related Third Parties. If in the future a potential conflict of interest related to the persons reported above is identified, modefinance Ratings will provide the appropriate information and if necessary the rating will be withdrawn.

The present Credit Rating is an opinion of the general creditworthiness that modefinance issues on the rated entity, and should be relied upon to a limited degree. The issued rating is subject to ongoing monitoring until withdrawal.

Contacts

Head Analyst – Chiara di Piazza (Senior Rating Analyst)

chiara.dipiazza@modefinance.com

+39 040 3756742

Assistant Analyst – Giulia Valentina Facchini (Senior Rating Analyst)

giulia.facchini@modefinance.com

+39 040 3756742

Responsible for Rating Approval – Pinar Dilek (Rating Process Manager)

pinar.dilek@modefinance.com

+39 040 3756740