Solicited Corporate Credit Rating for ETC INVEST S.P.A.: A3- (Affirm)

modefinance published the Solicited Corporate Credit Rating of ETC INVEST S.P.A. on their website and the rating assigned to the entity is A3- (affirm). The analysis revealed it is a good company, capable of repaying financial obligations and little dependent on possible adverse macroeconomic conditions.

ETC INVEST S.P.A., holding of the multinational Italian group “Export Trading Cooperation” (ETC), is a joint-stock company that provides consulting services in project finance and trade finance with an exclusive operational focus on African markets, directly and through the Group's subsidiaries. The company is specialized in Trade Finance and Supply Chain activities, through which it supports interchanges with Sub-Saharan African countries and investment projects. Since its foundation, the Company has pursued an internationalization process through the creation of representative offices, subsidiaries and funds across Europe and Africa, including the Regional Bureau Africa based in Cotonou (Benin).

Moreover, as an active member of SWIFT (Society for Worldwide Interbank Financial Telecommunication), the Group facilitates interbank financial messages between European and African financial institutions. Thanks to its direct and indirect presence in Africa and its combined expertise in trade finance and supply chain management, the ETC Group has become the leader and main reference of banks and industrial/commercial groups as far as the management of supply and investment projects in Africa is concerned, in sectors that range from agribusiness to industry, but also from transport to green energy.

Key Rating Assumptions

The company was established in 2016, but its operational activity began in 2012. Since then, ETC Group pursued a process of internationalization and Group reorganization, changing its legal form into a joint-stock company and improving its operational and governance structure. The Group is continuously growing thanks to the entry of new and important shareholders, as well. No black records have been found.

The corporate structure is clear as far as roles and responsibilities are concerned. In fact, from 2021, Monte Paschi Fiduciaria S.p.a. retains full control of the Group, while the two founding partners, hold office in the Board of Directors, in addition to holding minority blocks of shares. The BoD was implemented with the appointment of an additional independent director, while the control structure was strengthened through the appointment of a Supervisory Board.

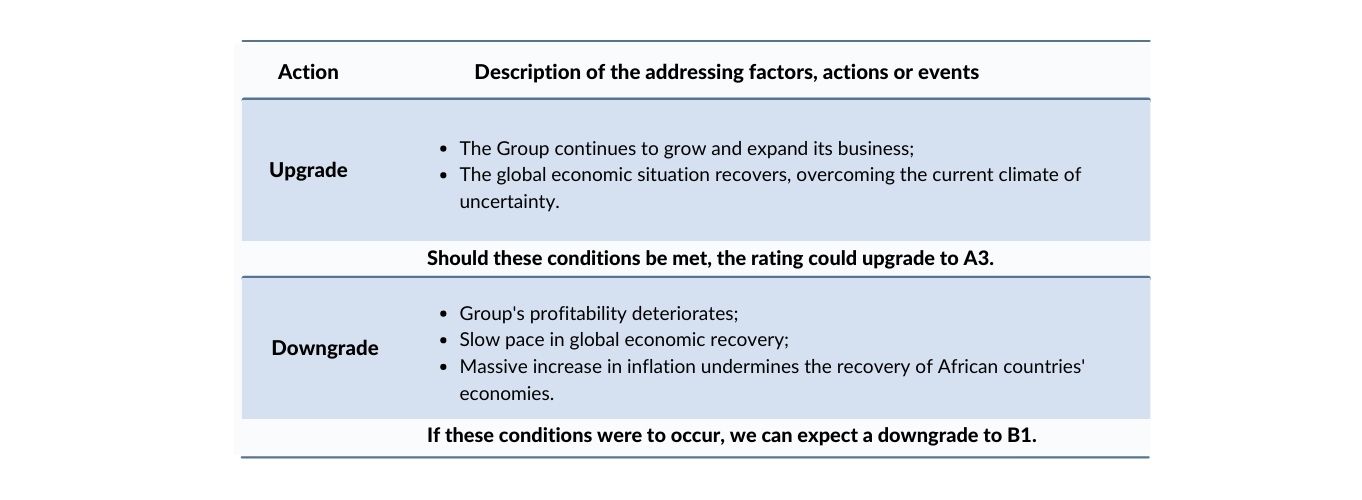

In FY2021, the Group, in addition to maintaining good liquidity and solvency, showed significant growth in sales, which resulted in improved margins and profitability. The Group’s report released by the Italian Central Credit Register doesn’t show any critical issues and reveals good management of maturity and overdraft risks. The peer group is healthy in all considered areas and in particular with reference to profitability, which shows a significant increase over the previous year. The management consulting sector showed encouraging results in 2021, and further growth is expected in 2022.

The rising inflationary wave and the effects of the war in Ukraine will have serious repercussions on African countries, which are already put to test by the effects of the pandemic – a widening in fiscal deficits is unavoidable. Tax increases and spending cuts are expected in the medium term and these, in addition to the tightening of monetary policies, will bring to a contraction of domestic demand. Africa will face a period of stress as far as debt repayment is concerned in 2024-25, when credit risk will become much more marked.

Sensitivity Analysis

{kind=link}

Important

The present Corporate Credit rating is issued by modefinance under EU Regulation N. 1060/2009 and following amendments.

The present rating is solicited, and based on both private and public information. The rated entity and/or related third parties have provided all private information used. modefinance had access to some accounts and other relevant internal documents of the rated entity and/or related third parties. Solicited and unsolicited ratings issued by modefinance are of comparable quality, as the solicitation status has no effect on methodologies used. More comprehensive information on modefinance Corporate Credit Ratings are available here.

The present Corporate Credit Rating is issued on MORE Methodology 2.0 and Rating Methodology 1.0. A comprehensive description of both methodologies, as well as information on modefinance Rating Scale and Mappings, is available here. For information on historical default rates of modefinance Corporate Credit Ratings please refer to ESMA Central Repository and ESMA European Rating Platform.

modefinance refers to default as a company under bankruptcy, or under liquidation status, or under administration or for which missed payments on a financial obligation are officially recorded.

The quality of the information available on the rated entity and used to determine the present rating was judged by modefinance as satisfactory. Please note that modefinance does not perform any audit activity and is not in a position to guarantee the accuracy of any information used and/or reported in the present document. As such, modefinance can accept no liability whatsoever for actions taken based on any information that may subsequently prove to be incorrect.

The present credit rating was notified to the rated entity in order to identify potential factual errors, as prescribed by the CRA Regulation. No amendments were applied after the notification process.

The rated entity is not a buyer of ancillary services provided by modefinance (credit risk software). The rating action issued by modefinance was performed independently. The analysts, members of the rating team involved in the process, modefinance Srl and its members and shareholders do not have any conflicts of interest in relation to the Rated Entity and/or Related Third Parties. If in the future a potential conflict of interest is identified in relation to the persons reported above, modefinance Ratings will provide the appropriate information and if necessary the rating will be withdrawn.

The present Credit Rating is an opinion of the general creditworthiness that modefinance issues on the rated entity, and should be relied upon to a limited degree. The issued rating is subject to an ongoing monitoring until withdrawal.

Contacts

Head Analyst – Stefano Chirsich (Rating Analyst)

stefano.chirsich@modefinance.com

Assistant Analyst – Andrea Marion (Rating Analyst)

andrea.marion@modefinance.com

Responsible for Rating Approval – Pinar Dilek (Rating Process Manager)

pinar.dilek@modefinance.com