Solicited Corporate Credit Rating for INNOVATIVE-RFK S.P.A.: B1+ (Upgrade)

modefinance published the review of the Solicited Corporate Credit Rating of INNOVATIVE-RFK S.P.A. on their website. The rating assigned to the entity is B1+ (upgrade). The analysis revealed that the company has average capability of repaying financial obligations, although possible adverse macroeconomic conditions or different management or strategies might impact on the capability of repaying their debt.

Innovative-RFK is an investment company founded in 2017 by the same partners as Red-Fish Kapital, an enterprise that has long been active in the field of private equity investments. The investment target of i-RFK is innovative Start-ups and SMEs with a solid profitability profile in terms of marginality, turnover growth and cash generation. i-RFK presents itself as an investment partner through the purchase of minority shares, while increasing SMEs and start-ups value and leading them towards a listing on AIM Italy stock exchange or other Growth Market SME.

Key Rating Assumptions

Founded in 2017 by Red Fish Kapital spa, i-RFK is an investment company specializing in high innovation content start-ups. During the financial year 2021, Innovative-RFK achieved new and important milestones and in August 2021 a so-called Charity Bond was issued through a debt crowdfunding campaign of the CrowdFundMe platform. From an economic and financial point of view, the company presents an adequate situation, characterized by a solid level of solvency, while profitability continues to appear limited, due to the still evident aftermath of the pandemic and the outbreak of the Russia-Ukraine conflict. This inevitably affected the profitability of i-RFK's investee companies. The analysis of cash flows shows how the company manages to maintain a certain cash margin thanks to its liquid funds. An analysis of the Central Credit Register shows no critical issues, as well.

The company is listed on Euronext Acces Paris and the main shareholder is Paolo Pescetto, a founding partner who holds 19.09% of the capital. As a holding company, i-RFK holds numerous shareholdings in various companies, most of which are in an adequate financial condition. Moreover, the company is administered by a Board of Directors, it has a board of statutory auditors and an external auditing company. The company's positioning compared to the reference sector remains adequate in terms of size and solvency; however, profitability can still be improved. The peer group expresses an adequate level of both general and financial debt, which is accompanied by good profitability. The sector relating to start-ups and innovative SMEs is growing steadily, both in terms of number and volume of turnover, and in terms of the workforce employed. The macroeconomic picture of Italy shows that the recovery in 2021 was generally in line with forecasts, with sustained economic growth that is likely to be confirmed in the coming years.

However, the conflict between Russia and Ukraine, with the consequent impact on energy and food prices, undermines the forecasts, especially as regards the maintaining of adequate economic growth, with domestic consumption likely to be affected by rising inflation, currently estimated at over 6%. The 2022 macroeconomic forecast data appear to be revised downwards compared to the estimates at the beginning of the year.

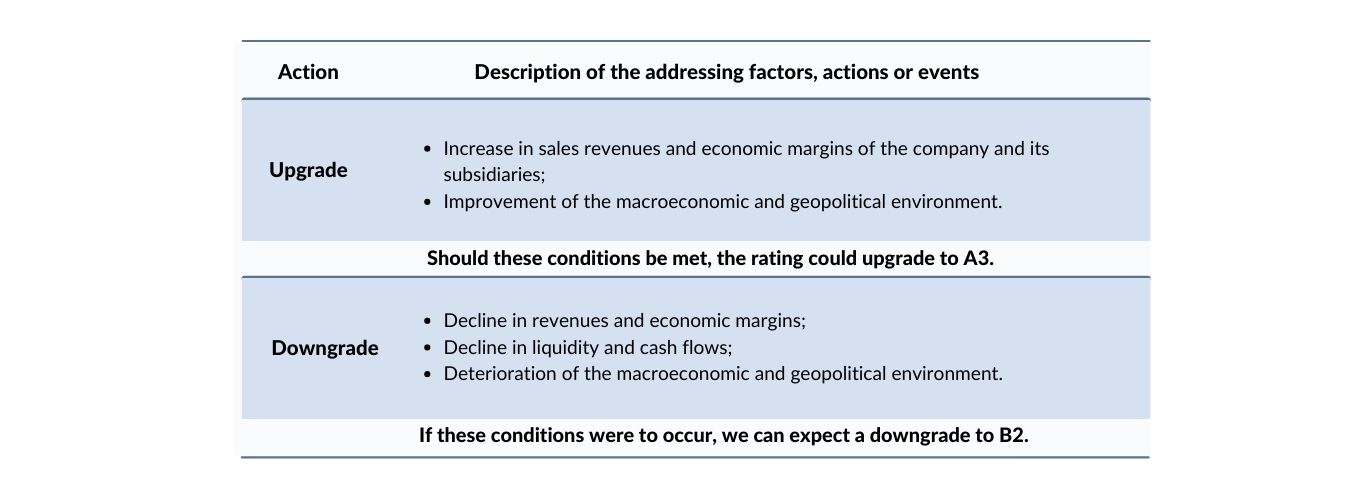

Sensitivity Analysis

In the following table, the addressing factors, actions or events that could lead to a rating upgrade or a downgrade are summarized:

{kind=link}

Important

The present Corporate Credit rating is issued by modefinance under EU Regulation N. 1060/2009 and following amendments.

The present rating is solicited, and based on both private and public information. The rated entity and/or related third parties have provided all private information used. modefinance had access to some accounts and other relevant internal documents of the rated entity and/or related third parties. Solicited and unsolicited ratings issued by modefinance are of comparable quality, as the solicitation status has no effect on methodologies used. More comprehensive information on modefinance Corporate Credit Ratings are available here.

The present Corporate Credit Rating is issued on MORE Methodology 2.0 and Rating Methodology 1.0. A comprehensive description of both methodologies, as well as information on modefinance Rating Scale and Mappings, is available here. For information on historical default rates of modefinance Corporate Credit Ratings please refer to ESMA Central Repository and ESMA European Rating Platform.

modefinance refers to default as a company under bankruptcy, or under liquidation status, or under administration or for which missed payments on a financial obligation are officially recorded.

The quality of the information available on the rated entity and used to determine the present rating was judged by modefinance as satisfactory. Please note that modefinance does not perform any audit activity and is not in a position to guarantee the accuracy of any information used and/or reported in the present document. As such, modefinance can accept no liability whatsoever for actions taken based on any information that may subsequently prove to be incorrect.

The present credit rating was notified to the rated entity in order to identify potential factual errors, as prescribed by the CRA Regulation. No amendments were applied after the notification process.

The rated entity is not a buyer of ancillary services provided by modefinance (credit risk software). The rating action issued by modefinance was performed independently. The analysts, members of the rating team involved in the process, modefinance Srl and its members and shareholders do not have any conflicts of interest in relation to the Rated Entity and/or Related Third Parties. If in the future a potential conflict of interest is identified in relation to the persons reported above, modefinance Ratings will provide the appropriate information and if necessary the rating will be withdrawn.

The present Credit Rating is an opinion of the general creditworthiness that modefinance issues on the rated entity, and should be relied upon to a limited degree. The issued rating is subject to an ongoing monitoring until withdrawal.

Contacts

Head Analyst – Stefania Latin (Rating Analyst)

stefania.latin@modefinance.com

Assistant Analyst – Eva Vocci (Rating Analyst)

eva.vocci@modefinance.com

Responsible for Rating Approval – Pinar Dilek (Rating Process Manager)

pinar.dilek@modefinance.com