Solicited Corporate Credit Rating for NAZIONE VERDE S.R.L.: B1- (First Issuance)

modefinance published the Solicited Corporate Credit Rating of NAZIONE VERDE S.R.L. on the website and the rating assigned to the entity is B1- (first issuance). The analysis revealed it is an adequate company with average capability of repaying financial obligations and it is little affected by adverse economic scenarios.

NAZIONE VERDE S.R.L. is a company founded in 2017 with the aim to invest in Green Economy and in the energetic redevelopment of public and private real estate assets.

Key Rating Assumptions

The company NAZIONE VERDE S.R.L. presents an economic and financial health characterized by a substantial reduction in shareholders’ funds, which can be referred to change in corporate structure. This had the concomitant effect of raising profitability ratios, which were significantly strengthened. At the same time, the liquidity area appears to be adequate.

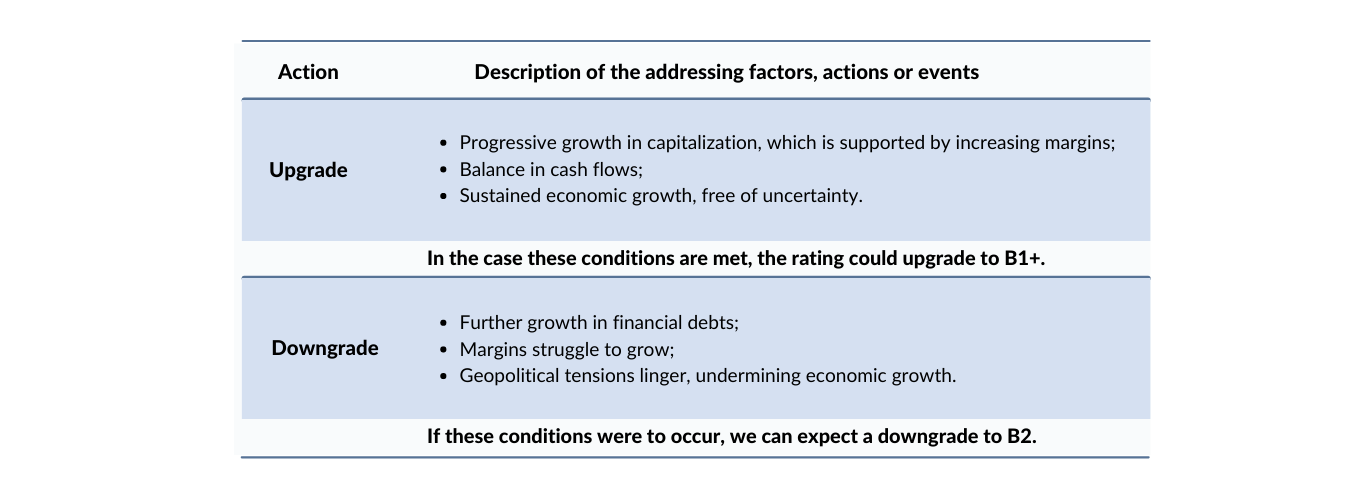

The cash flows expressed by the Company manifest a physiological contraction of liquidity, which is affected by the erosion operated by financing activities, which is accompanied by operations absorption. The Bank of Italy’s Central Credit Register reveals a positive management of credit lines granted.

The Company was founded in 2017 and its management is currently focused on consolidation of its position as a key player in the implementation of eco-bonus and sisma-bonus incentives, while diversifying and expanding its operations. The administrative body presents a collegial form and its actions are controlled by a monocratic auditor. The Company has also appointed a supervisory body ex 231/2001. The group structure appears rather lean, with control attributable to five different physic persons, operating through a holding company. The Company, the shareholders or administrators have no black records.

The Company ranks better than the industry median in both size and profitability, while in terms of solvency it expresses a weak ranking. The peer group manifests an adequate level of solvency and a good financial balance, while profitability shows growth during the last year.

The construction sector and, more generally, the sector of energy redevelopment of buildings, is experiencing a period of appreciable recovery, although some important critical issues have emerged and threatens to undermine the positive trend. The macroeconomic picture of Italy presents a recovery in 2021, that has met forecasts: this is expected to be followed by a three-year period of sustained economic growth, which is accompanied by growing uncertainty, attributable to geopolitical tensions. Macroeconomic forecast data are therefore likely to be revised downward.

Sensitivity Analysis

{kind=link}

Important

The present Corporate Credit rating is issued by modefinance under EU Regulation 1060/2009 and following amendments.

The present rating is solicited and is based on both private and public information. The rated entity and/or related third parties have provided all private information used. modefinance had access to some accounts and other relevant internal documents of the rated entity and/or related third parties. Solicited and unsolicited ratings issued by modefinance are of comparable quality, as the solicitation status has no effect on methodologies used. More comprehensive information on modefinance Corporate Credit Ratings are available at http://cra.modefinance.com/en

The present Corporate Credit Rating is issued on MORE Methodology 2.0 and Rating Methodology 1.0. A comprehensive description of both methodologies, as well as information on modefinance Rating Scale and Mappings, is available at http://cra.modefinance.com/en/methodologies.

For information on historical default rates of modefinance Corporate Credit Ratings please refer to ESMA Central Repository and ESMA European Rating Platform.

modefinance refers to default as a company under bankruptcy, or under liquidation status, or under administration or for which missed payments on a financial obligation are officially recorded.

The quality of the information available on the rated entity and used to determine the present rating was judged by modefinance as satisfactory. Please note that modefinance does not perform any audit activity and is not in a position to guarantee the accuracy of any information used and/or reported in the present document. As such, modefinance can accept no liability whatsoever for actions taken based on any information that may subsequently prove to be incorrect.

The present credit rating was notified to the rated entity in order to identify potential factual errors, as prescribed by the CRA Regulation.

No amendments were applied after the notification process.

The rated entity is not a buyer of ancillary services provided by modefinance (credit risk software).

The rating action issued by modefinance was performed independently. The analysts, members of the rating team involved in the process, modefinance Srl and its members and shareholders do not have any conflicts of interest in relation to the Rated Entity and/or Related Third Parties. If in the future a potential conflict of interest is identified in relation to the persons reported above, modefinance Ratings will provide the appropriate information and if necessary the rating will be withdrawn.

The present Credit Rating is an opinion of the general creditworthiness that modefinance issues on the rated entity, and should be relied upon to a limited degree. The issued rating is subject to an ongoing monitoring until withdrawal.

Contacts

Head Analyst - Christian Raimondo, Rating Analyst

christian.raimondo@modefinance.com

Assistant Analyst - Stefania Latin, Rating Analyst

stefania.latin@modefinance.com

Responsible for Rating Approval - Pinar Dilek, Rating Process Manager

pinar.dilek@modefinance.com