Solicited Corporate Credit Rating for ORIGINAL BIRTH S.P.A: B1 (First Issuance)

modefinance published the Solicited Corporate Credit Rating of ORIGINAL BIRTH S.P.A. on the CRA website and the rating assigned to the entity is B1 (first issuance). The analysis revealed it is an adequate company with average capability of repaying financial obligations and it is little affected by adverse economic scenarios.

ORIGINAL BIRTH S.P.A. is a company operating since 1979 in the independent aftermarket (IAM) of the automotive industry. The Company sells a wide range of components, for both domestic and international markets. The Company's market share has been growing in recent years thanks to new production lines, the expansion of the sales network and partnerships, and continuous investments, which are the main growth driver the management focuses on.

Key Rating Assumptions

The Company's economic and financial situation shows a good level of capitalization and fully sustainable financial debt, as demonstrated by financial leverage and NFP/MOL ratio, both at low values.

In 2021, revenues raised by +15% (17.7 mln euros), which also led to a growth in the EBITDA margin. Profitability ratios show sufficient values. Regarding liquidity management, a fully adequate current ratio is observed. Although liquidity declined in 2021, it is appreciable the Company's ability to generate a positive operating cash flow as a result of conspicuous self-financing and efficient management of the Net Working Capital.

In addition, the analysis of the Bank of Italy’s Central Credit Register highlights the correct management of credit lines.

The Company has an administrative body and a supervisory body, both in a collegial form, and shows a straightforward corporate structure with a single shareholder represented by Emera S.p.A., the holding company headed by the Chianese family.

Sector peer group analysis shows adequate performance in all areas considered. The Company, compared with the aforementioned peer group, is well positioned in terms of size and solvency, while profitability is below the 50th percentile. However, Company’s ROI and ROE express sufficient values when considered from a stand-alone perspective.

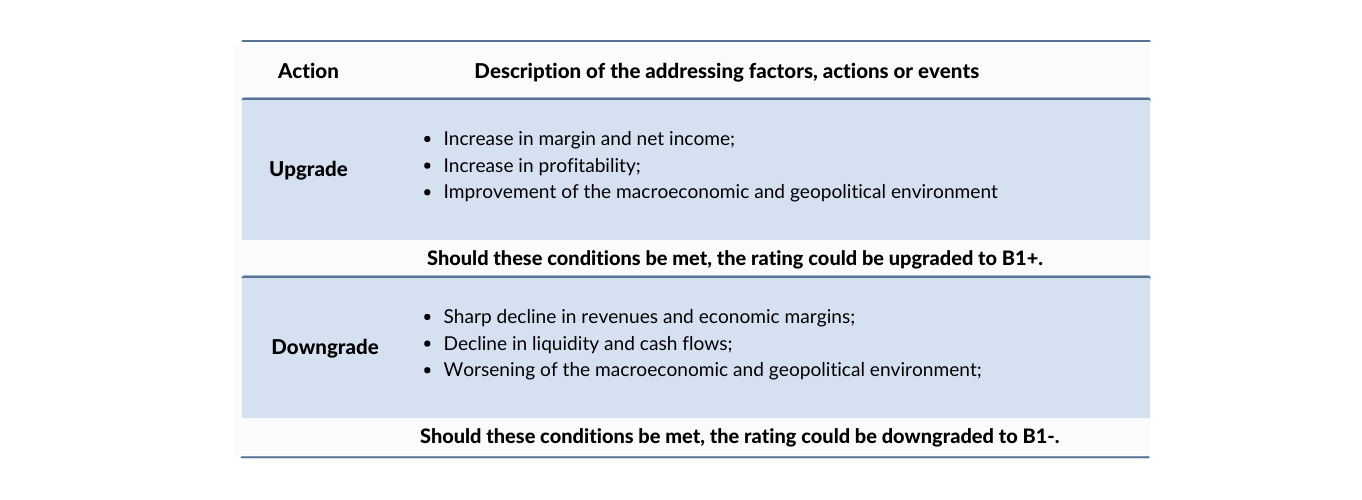

The macroeconomic and geopolitical environment is still uncertain, although early signs of improvement could lead to an upward revision of the economic forecast for the coming months. The automotive sector, in which the Company operates, has been inevitably impacted by the macroeconomic situation, but a gradual recovery in sales and production is estimated for the period 2023-2027, also with the contribution of the electric mobility market.

Sensitivity Analysis

{kind=link}

Important

The present Corporate Credit rating is issued by modefinance under EU Regulation 1060/2009 and following amendments.

The present rating is solicited and is based on both private and public information. The rated entity and/or related third parties have provided all private information used. modefinance had access to some accounts and other relevant internal documents of the rated entity and/or related third parties. Solicited and unsolicited ratings issued by modefinance are of comparable quality, as the solicitation status has no effect on methodologies used. More comprehensive information on modefinance Corporate Credit Ratings are available at http://cra.modefinance.com/en

The present Corporate Credit Rating is issued on MORE Methodology 2.0 and Rating Methodology 1.0. A comprehensive description of both methodologies, as well as information on modefinance Rating Scale and Mappings, is available at http://cra.modefinance.com/en/methodologies.

For information on historical default rates of modefinance Corporate Credit Ratings please refer to ESMA Central Repository and ESMA European Rating Platform.

modefinance refers to default as a company under bankruptcy, or under liquidation status, or under administration or for which missed payments on a financial obligation are officially recorded.

The quality of the information available on the rated entity and used to determine the present rating was judged by modefinance as satisfactory. Please note that modefinance does not perform any audit activity and is not in a position to guarantee the accuracy of any information used and/or reported in the present document. As such, modefinance can accept no liability whatsoever for actions taken based on any information that may subsequently prove to be incorrect.

The present credit rating was notified to the rated entity in order to identify potential factual errors, as prescribed by the CRA Regulation.

No amendments were applied after the notification process.

The rated entity is not a buyer of ancillary services provided by modefinance (credit risk software).

The rating action issued by modefinance was performed independently. The analysts, members of the rating team involved in the process, modefinance Srl and its members and shareholders do not have any conflicts of interest in relation to the Rated Entity and/or Related Third Parties. If in the future a potential conflict of interest is identified in relation to the persons reported above, modefinance Ratings will provide the appropriate information and if necessary the rating will be withdrawn.

The present Credit Rating is an opinion of the general creditworthiness that modefinance issues on the rated entity, and should be relied upon to a limited degree. The issued rating is subject to an ongoing monitoring until withdrawal.

Contacts

Head Analyst - Elisa Graffi, Rating Analyst

elisa.graffi@modefinance.com

Responsible for Rating Approval - Pinar Dilek, Rating Process Manager

pinar.dilek@modefinance.com