modefinance UnsolicitedCorporate Credit Rating for PRADA S.P.A.: B1+ (Downgrade)

modefinance published on its CRA website the Unsolicited Corporate Credit Rating (Downgrade) of PRADA S.P.A. and the rating assigned to the entity is B1+. The analysis revealed that the company has average capabilities of repaying financial obligations and that possibile adverse macroeconomic conditions or different management or strategies might impact on the capability of repaying debts.

Reason for review: relevant news on the spread od Covid-19 both in Italy and Far-East countries and publication 2019 annual account.

Key Rating Assumptions

The reasons that have driven this decision are:

- In 2019, despite the 3% increase in turnover, there was a drop in the More score, mainly due to the adoption of IFRS 16 on leasing, which entailed a deterioration in the solvency indicators compared to 2018. Leverage maintained a good level, while the financial leverage, consequently, assumed a weak value. Liquidity remained adequate, although continuously decreasing in the three-year period analyzed, while profitability was all in all sufficient. It should be noted that in 2019 Prada obtained full control of the retail network through the acquisition of Fratelli Prada S.p.A. for € 48.6 million and that the allocation of the previous fiscal year’s profit was almost totally offset by the distribution of dividends distributed to Prada Spa shareholders for € 153.5 million.

- Compared to its peer group, Prada S.p.A. is among the largest in the sector, although profitability can be improved. Prada is a long-established company and has a leadership position in its pertaining peer group.

- In the last four-year period, all the peer group players recorded an increase in profitability and liquidity ratios. Differently Prada, in 2019, shows a slight worsening: leverage aligns with the peer group, while financial leverage underperformed it; liquidity and profitability show a lower level than the peer group.

- From January 2020 the global scenario has been characterized by the health emergency triggered by the outbreak of the Coronavirus and the consequent restrictive measures for its containment put in place by the public authorities of the countries concerned. The lockdown applied by many countries around the world generates unprecedented economic and social damages. In particular, in the three main areas where Prada operates (Italy, Europe, China) it is expected a worsening in all macroeconomic indicators (the forecast for GDP growth in 2020 is: -9.1% in Italy, -6,7% in Europe and 1.2% in China).

- For Italy, a tiring recovery is expected after the collapse caused by the coronavirus emergency. Investments and exports are suffering even more than consumption: the Italian government is devising different tools capable of support production activities, citizens and families, however the situation is still evolving and undefined.

- In 2020, the personal luxury goods industry has been impacted by the coronavirus pandemic and the resulting national lockdowns and air traffic restrictions, with negative signs in all product categories and markets. For the current year, in particular, it has been estimated an average 20% drop in personal luxury goods consumption on all markets.

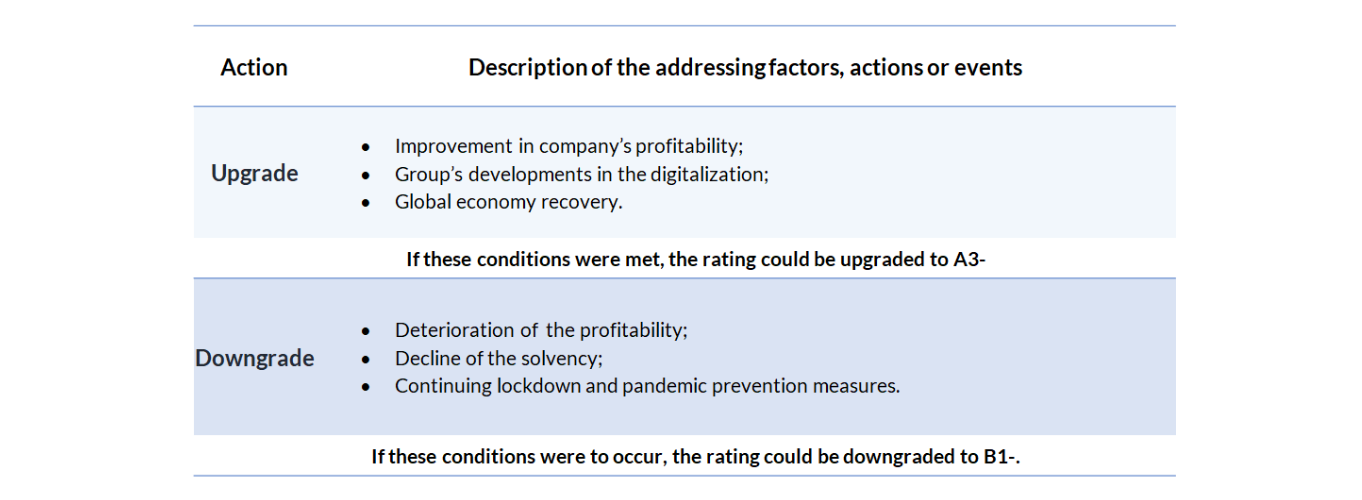

Sensitivity Analysis

The following table summarizes the addressing factors, actions or events that could lead to a rating upgrade or downgrade:

{kind=link}

Important

The present Corporate Credit rating is issued by modefinance under EU Regulation 1060/2009 and following amendments.

The present rating is unsolicited: the rated entity and/or related third parties have not participated in the rating process and modefinance has no access to accounts or other relevant internal documents of the rated entity and/or related third parties.

{kind=link}

Solicited and unsolicited ratings issued by modefinance are of comparable quality, as the solicitation status does not affect the methodologies used. More comprehensive information on modefinance Corporate Credit Ratings is available here.

The present Corporate Credit Rating is issued on MORE Methodology 2.0 and Rating Methodology 1.0.

A comprehensive description of both methodologies, as well as information on modefinance's Rating Scale and Mappings, is available here.

For information on historical default rates of modefinance Corporate Credit Ratings please refer to ESMA Central Repository and ESMA European Rating Platform.

modefinance refers to default as a company under bankruptcy, or under liquidation status, or under administration or for which missed payments on a financial obligation are officially recorded.

The quality of the information available on the rated entity and used to determine the present rating was judged by modefinance as satisfactory. Please note that modefinance, however, is not in a position to guarantee the accuracy of that information. As such, modefinance can accept no liability whatsoever for actions taken based on any information that may subsequently prove to be incorrect.

The present credit rating was notified to the rated entity in order to identify potential factual errors, as prescribed by the CRA Regulation.

No amendments were applied after the notification process.

The Rated Entity or Related Third Party has not purchased ancillary services from modefinance. The rating action issued by modefinance was performed independently. The analysts, members of the rating team involved in the process, modefinance Srl and its members and shareholders do not have any conflicts of interest concerning the Rated Entity and/or Related Third Parties. If in the future a potential conflict of interest related to the persons reported above is identified, modefinance Ratings will provide the appropriate information and if necessary the rating will be withdrawn.

he present Credit Rating is an opinion of the general creditworthiness that modefinance issues on the rated entity, and should be relied upon to a limited degree. The issued rating is subject to ongoing monitoring until withdrawal.

Contacts

Head Analyst – Giulia Valentina Facchini (Senior Rating Analyst)

giulia.facchini@modefinance.com

+39 040 3756742

Assistant Analyst – Andrea Marion (Rating Analyst)

andrea.marion@modefinance.com

+39 040 3756740

Responsible for Rating Approval – Pinar Dilek (Rating Process Manager)

pinar.dilek@modefinance.com

+39 040 3756740