Solicited Corporate Credit Rating for STAR7 S.P.A.: B1 (First Issuance)

modefinance published the Solicited Corporate Credit Rating of STAR7 S.P.A. on the CRA website and the rating assigned to the entity is B1 (first issuance). The analysis revealed it is an adequate company with average capability of repaying financial obligations and it is little affected by adverse economic scenarios.

STAR7 S.P.A. operates in business services dedicated to product information and content. From product and process engineering support to the creation and management of technical and marketing content, to translation, print on demand, and virtual experience: with its services, STAR7 can support customers' industrial activities throughout the life cycle of any product, from the design phase to after-sales. Founded in 2000 as the Italian subsidiary of the multinational Star Group, the company has built up its independence over the years within its sector of reference, thanks above all to its wide range of related services, which today make it one of the leading European players. As of the end of 2021, STAR7 has listed its shares on the regulated market of Borsa Italiana.

Key Rating Assumptions

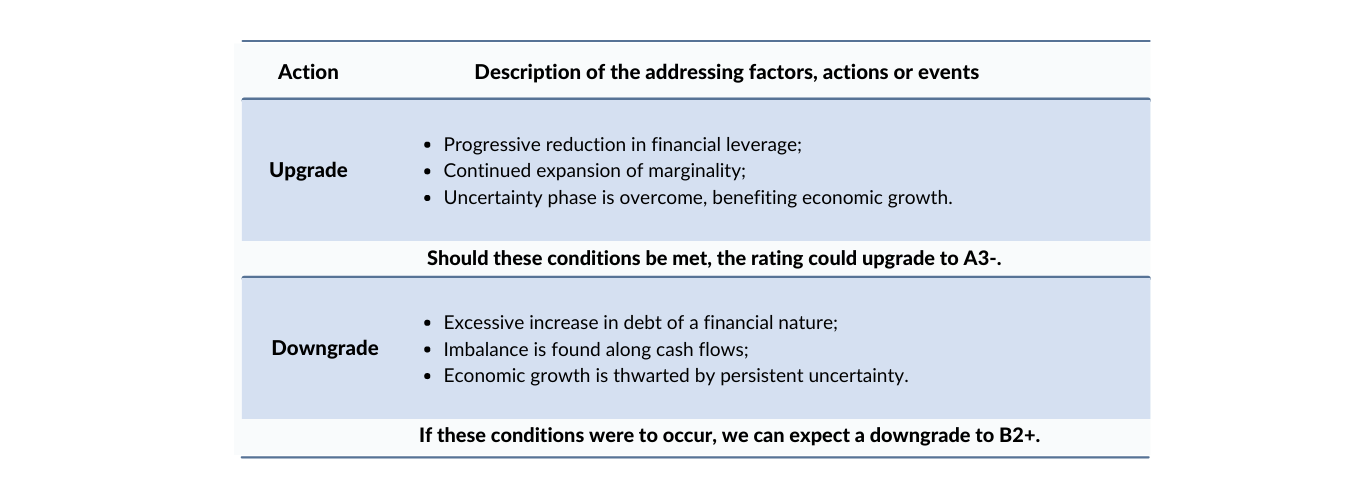

The company STAR7 S.P.A. presents an economic and financial situation characterized by an appreciable capitalization, with shareholders’ funds contributing to the financing of one third of total assets and financial indebtedness largely concentrated in medium and long-term.

The management of credit lines appears to be correct, with punctual payments for loans and long-term debts, while the utilization of self-liquidating risks and overdraft facilities risks appear contained.

The financial balance is adequate, with current ratio above one, while from a dynamic point of views, there is no decisive impact of working capital on cash flows dynamics. In fact, the latter show a contraction in cash flow from operations, while the ratio of financing activities to investments is in balance. Margins, instead, continue their expansion.

The governance and audit system is aligned with best practices, with Board of Directors featuring several figures from outside the ownership. Furthermore, in addition to the Board of Statutory Auditors, the control function is supported by the work of an auditing firm and supervisory body ex-231/2001, which also have a collegial form. The group structure appears broad and articulated, with the Company controlling, both directly and indirectly, several companies, including foreign companies: the consolidation perimeter is, in any case, easily identifiable.

The Company’s positioning, with respect to the reference peer group, appears solid in terms of size; solvency and profitability are, instead, below the 50th percentile. The peer group expresses solid performance in terms of capitalization and profitability, while the sector’s financial balance is adequate.

The macroeconomic environment is affected by uncertainty, constantly aligned by geopolitical tensions and high inflation. However, the particular business conducted by the Company makes it little exposed to country risk.

Sensitivity Analysis

{kind=link}

Important

The present Corporate Credit rating is issued by modefinance under EU Regulation 1060/2009 and following amendments.

The present rating is solicited and is based on both private and public information. The rated entity and/or related third parties have provided all private information used. modefinance had access to some accounts and other relevant internal documents of the rated entity and/or related third parties. Solicited and unsolicited ratings issued by modefinance are of comparable quality, as the solicitation status has no effect on methodologies used. More comprehensive information on modefinance Corporate Credit Ratings are available at http://cra.modefinance.com/en

The present Corporate Credit Rating is issued on MORE Methodology 2.0 and Rating Methodology 1.0. A comprehensive description of both methodologies, as well as information on modefinance Rating Scale and Mappings, is available at http://cra.modefinance.com/en/methodologies.

For information on historical default rates of modefinance Corporate Credit Ratings please refer to ESMA Central Repository and ESMA European Rating Platform.

modefinance refers to default as a company under bankruptcy, or under liquidation status, or under administration or for which missed payments on a financial obligation are officially recorded.

The quality of the information available on the rated entity and used to determine the present rating was judged by modefinance as satisfactory. Please note that modefinance does not perform any audit activity and is not in a position to guarantee the accuracy of any information used and/or reported in the present document. As such, modefinance can accept no liability whatsoever for actions taken based on any information that may subsequently prove to be incorrect.

The present credit rating was notified to the rated entity in order to identify potential factual errors, as prescribed by the CRA Regulation.

No amendments were applied after the notification process.

The rated entity is not a buyer of ancillary services provided by modefinance (credit risk software).

The rating action issued by modefinance was performed independently. The analysts, members of the rating team involved in the process, modefinance Srl and its members and shareholders do not have any conflicts of interest in relation to the Rated Entity and/or Related Third Parties. If in the future a potential conflict of interest is identified in relation to the persons reported above, modefinance Ratings will provide the appropriate information and if necessary the rating will be withdrawn.

The present Credit Rating is an opinion of the general creditworthiness that modefinance issues on the rated entity, and should be relied upon to a limited degree. The issued rating is subject to an ongoing monitoring until withdrawal.

Contacts

Head Analyst - Christian Raimondo, Rating Analyst

christian.raimondo@modefinance.com

Responsible for Rating Approval - Pinar Dilek, Rating Process Manager

pinar.dilek@modefinance.com