Corporate Credit Rating (Solicited) for ZENERGIA S.R.L.: B1 (First Issuance)

modefinance published the Solicited Corporate Credit Rating of ZENERGIA S.R.L. on its CRA website and the rating assigned to the entity is B1 (First Issuance). The analysis revealed it is an adequate company with average capability of repaying financial obligations and it is little affected by adverse economic scenarios.

Key Rating Assumptions

The rating assigned by modefinance is based on the following key elements:

- The company shows a balanced assets and liabilities structure, with an extremely good solvency, thanks to lack of financial indebtedness. From the liquidity point of view, it needs to improve the cash conversion cycle, while profitability could be improved in turnover. The overall situation is good.

- The cash flow analysis highlighted an absorption of cash and cash equivalents, caused by an inappropriate working capital management which led to a negative operating cash flow. In the last two years, liquid assets has decreased but they are still sufficient. In any case, a reassessment of cash management appears necessary.

- ZENERGIA S.R.L. has no financial indebtedness and therefore no data were reported in the Italian Central Credit Register.

- The governance is represented by the sole administrator, who is also the shareholder of the company, so, despite the size of the company, it seems to be necessary to increase roles and responsibilities and integrate the management with a statutory board.

- The company operates for 10 years in the energy sector, strengthening its presence and its products and services. No black records were found.

- Considering the reference peer group, ZENERGIA S.R.L. could be considered the biggest among the other companies and the one with the better performance in solvency ratios. Still, the company could improve from the profitability point of view. Regarding the peer group, the solvency ratios show a reduction in total indebtedness, whose level remains high but not risky. Also, liquidity level appears not sufficient for the industry, while profitability is the best area considered for the peer group.

- In 2019 there has been a consistent drop in raw materials prices that brought a reshaping of the market in terms of demand and supply for all the players of the industry. The pandemic related to Covid-19 and the consequent lockdown will bring in 2020 to higher consumption for the families, but, at the same time, to an increase in default of payments that all companies will have to manage to avoid liquidity losses. The pandemic is still presents and the consequent economic losses will lead to a contraction in GDP and an increase in unemployment rates. It is clear no company will benefit from this difficult situation, even if specific policies will be put in place from the Italian and European governments.

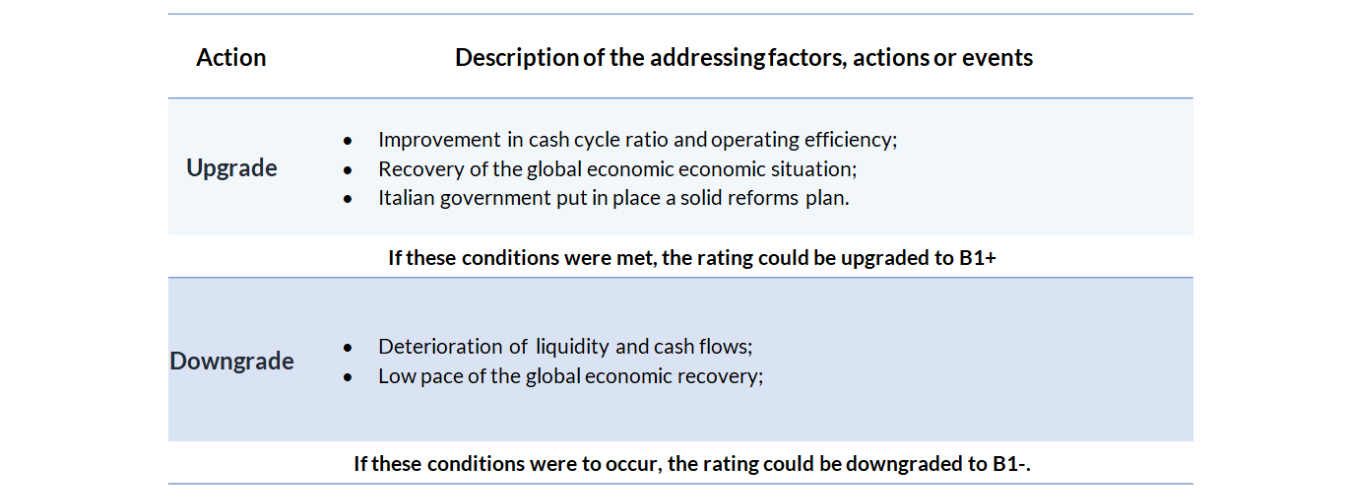

Sensitivity Analysis

In the following table, the addressing factors, actions or events that could lead to a rating upgrade or a downgrade are summarized:

{kind=link}

Important

The present Corporate Credit rating is issued by modefinance under EU Regulation N. 1060/2009 and following amendments.

The present rating is solicited and is based on both private and public information. The rated entity and/or related third parties have provided all private information used. modefinance had access to some accounts and other relevant internal documents of the rated entity and/or related third parties. Solicited and unsolicited ratings issued by modefinance are of comparable quality, as the solicitation status has no effect on methodologies used. More comprehensive information on modefinance Corporate Credit Ratings are available here.

The present Corporate Credit Rating is issued on MORE Methodology 2.0 and Rating Methodology 1.0.

For information on historical default rates of modefinance Corporate Credit Ratings please refer to ESMA Central Repository and ESMA European Rating Platform.

modefinance refers to default as a company under bankruptcy, or under liquidation status, or under administration or for which missed payments on a financial obligation are officially recorded.

The quality of the information available on the rated entity and used to determine the present rating was judged satisfactory by modefinance. Please note that modefinance does not perform any audit activity and is not in a position to guarantee the accuracy of any information used and/or reported in the present document. As such, modefinance can accept no liability whatsoever for actions taken based on any information that may subsequently prove to be incorrect.

The present credit rating was notified to the rated entity in order to identify potential factual errors, as prescribed by the CRA Regulation. No amendments were applied after the notification process.

The rated entity is not a buyer of ancillary services provided by modefinance (credit risk software).

The rating action issued by modefinance was performed independently. The analysts, members of the rating team involved in the process, modefinance Srl and its members and shareholders do not have any conflicts of interest in relation to the Rated Entity and/or Related Third Parties. If in the future a potential conflict of interest is identified in relation to the persons reported above, modefinance Ratings will provide the appropriate information and if necessary the rating will be withdrawn.

The present Credit Rating is an opinion of the general creditworthiness that modefinance issues on the rated entity, and should be relied upon to a limited degree. The issued rating is subject to an ongoing monitoring until withdrawal.

Contacts

Head Analyst – Eva Vocci(Rating Analyst)

eva.vocci@modefinance.com

+39 040 3756740

Assistant Analyst – Fabio Politelli (Rating Analyst)

fabio.politelli@modefinance.com

+39 040 3756740

Responsible for Rating Approval – Pinar Dilek (Rating Process Manager)

pinar.dilek@modefinance.com

+39 040 3756740