Two different evaluation models: rating and scoring

Since the global economic downturn, rating agencies have not enjoyed a good reputation.

In the common mindset, they are associated with ruthless judges and there is a general misunderstanding about ratings themselves.

Such misinformation is detrimental for companies first, which could rely on ratings to evaluate the creditworthiness of clients and partners and to reduce unexpected losses.

Let’s try to clarify this issue and see how ratings can help companies to assess the riskiness of their investments.

Let's start with a definition: a credit rating is an opinion on a company's ability to generate the resources needed to meet its financial commitments.

The creditworthiness analysis includes all the key factors that may affect the economic and financial health of the evaluated entity: not only the balance sheet data, but also qualitative parameters, such as the board composition, the country risk and the management’s professional background.

Similar to a credit rating, a credit score is an assessment of a company creditworthiness obtained through an automated process and the use of statistical models or system. The assessment is conveyed by means of a score and evaluates quantitative parameters only, i.e. the company’s financial data and public information that can be mathematically quantified.

To sum up, while credit scorings are based mainly on the analysis of the company's balance sheet data, comparing the values of each ratio with the average values resulting from the sector comparison, credit ratings take also into account all the external factors that may affect the company’s performances, and must be therefore drawn up by financial analysts.

Rating and scoring: what fits your needs?

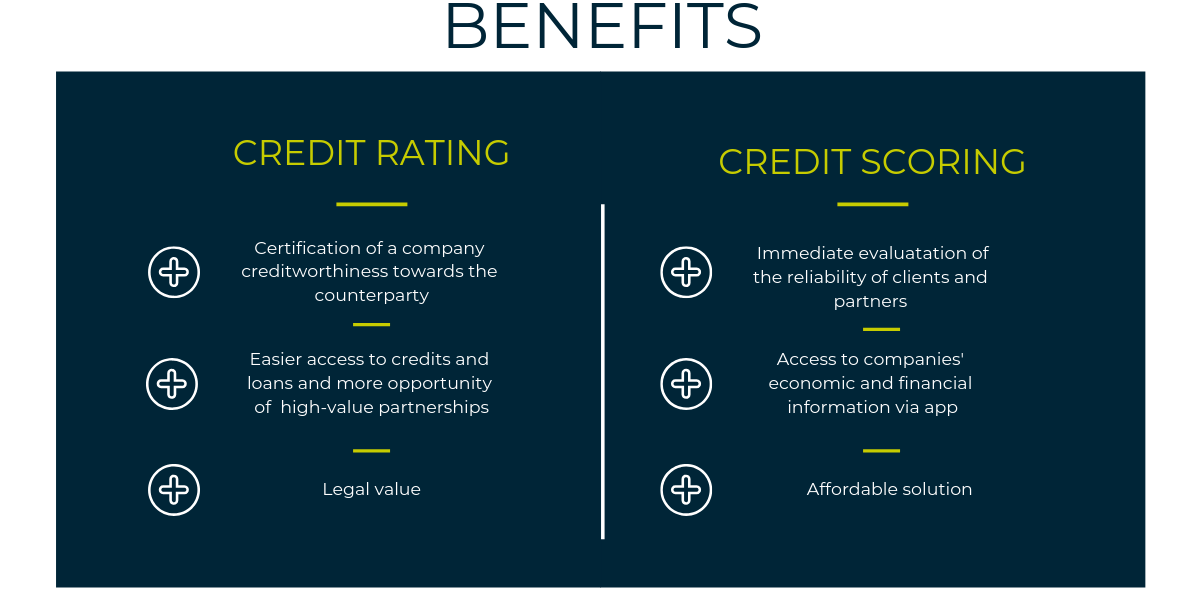

A credit rating helps companies certify their reliability towards the counterparty, to gain an easier access to credits and loans, to secure high-value partnerships or to evaluate the economic and financial situation of a third entity.

Scoring services are usually available via mobile or web app and are a useful and affordable solution for small and medium-sized businesses to gain an intuitive and immediate evaluation of the counterparty’s financial situation.

Ratings issued by credit rating agencies under EU Regulation n.1060/2009 have legal value, while credit scoring services can be provided by anyone with access to the companies’ public data and financial statements (credit bureaus, consumer credit reporting agencies, data providers, etc).

For this reason, when choosing scoring software to rely on, it is important to verify the reliability of the scoring methodology and opt for solutions that regularly review the results, such as s-peek, whose credit scores are calculated through the MORE methodology, which is tested and validated on a regular basis.

{kind=link}