2022: global Fintech investments amount to 107,8 billion dollars, as a proof of the effectiveness of tools and services put in place to support the real economy. Given that Fintech solutions are also designed to take into consideration the risk of a certain funding, it is here that the difference with traditional models emerges, showing how advanced tech, quality creditworthiness assessments and dynamic models may help financial institutions in analyzing an enterprise’s reliability to repay its debts.

Thus, in order to allow a safer and improved risk management process when granting a loan, deliver fully automated and digitized tech solutions, and provide banks with increasingly efficient tailor-made services, modefinance launched its proprietary Amortization Plan Over Uncertainty (APOU) model, able of building and/or evaluating an amortization plan while integrating the risk factor in the entire process.

In this article, we want to focus on modefinance’s Pricing model, aimed at calculating the risk-based pricing of a corporate finance operation in a completely digitized way, all while integrating a strong customization approach for a greater lending process reliability.

modefinance’s Pricing model

As already explained, the APOU Model consists of building and/or evaluating an amortization plan, as well as calculating its risk-based metrics (risk-based NPV, risk-based IRR, Duration, Average time to maturity and RAROC) and the “optimal” pricing of the financial operation.

In view of a digital evolution that makes strategies in the financial field much easier, the decision of adopting the Pricing model developed by modefinance allows a financial institution to automatically access the Optimal Annual Active Rate to be applied on a loan provided to a customer. Thus, users can understand whether a financial operation is profitable for the financial intermediary or not, and whether the interest rate offered to the obligor is as close as possible to the fair value. A fundamental strategic instrument that meets the entire financial landscape’s needs, and that satisfies the bank’s intention of securing as much profit as possible without bringing the debtor to the edge on one side, and the enterprise’s ability to negotiate, making it thus obtain more favorable terms.

Thanks to the Pricing model, it is possible that the result returned presents a fair interest rate, upon which it is feasible building an adequate amortization plan, based on several inputs: ROI (Return on Investment), the amortization plan (inputted by the client or calculated by the APOU model), costs of funding, operational costs, costs for counterparties, recovery rate, market rate and financial guarantees (always considered in the APOU model).

How does the Pricing model work?

Well aware that any financial intermediary’s needs consist of knowing the profit and costs on the loan they are granting, modefinance’s active rate pricing is based on a simple mathematical formula:

i(ar) = i(tr) + i(rf) + risk spread

where:

i(ar) = active rate

i(tr) = target rate of the bank

i(rf) = risk free rate.

The optimal active rate is equal to the sum of the:

• Target rate: i(tr) = ROI – costs incurred by the financial institution

• Risk free rate: i(rf) = interest rate of a risk-free financial transaction

• Risk spread = structure of the amortization plan + corporate risk.

The NPV, IRR and Duration metrics of the target amortization plan delivered by the financial institution are calculated based on the target rate defined by the bank. The interest rate thus obtained incorporates investor’s needs and requirements in terms of ROI, but it doesn’t include the risk. Should the client need it, modefinance is capable of calculating the above metrics that take risk into consideration (so-called risk-free metrics), even if the target rate doesn’t.

This is where modefinance introduces the notion of Active Rate Pricing, an interest rate based on a fair-value approach that accounts the risk of a financial operation in its calculation, the latter based on the probability of default of a given enterprise.

Once the active rate pricing is obtained, it can be inserted in the automatically recalculated amortization plan, the APOU model being thus able to provide metrics that take risk into consideration in a completely digitized way: risk-based NPV, risk-based IRR, risk-based Duration and RAROC. Eventually, the rate i(ar) thereby obtained can be used to benchmark the operation against the pricing defined by the user.

A tangible example: case study with and without the adoption of the Pricing model

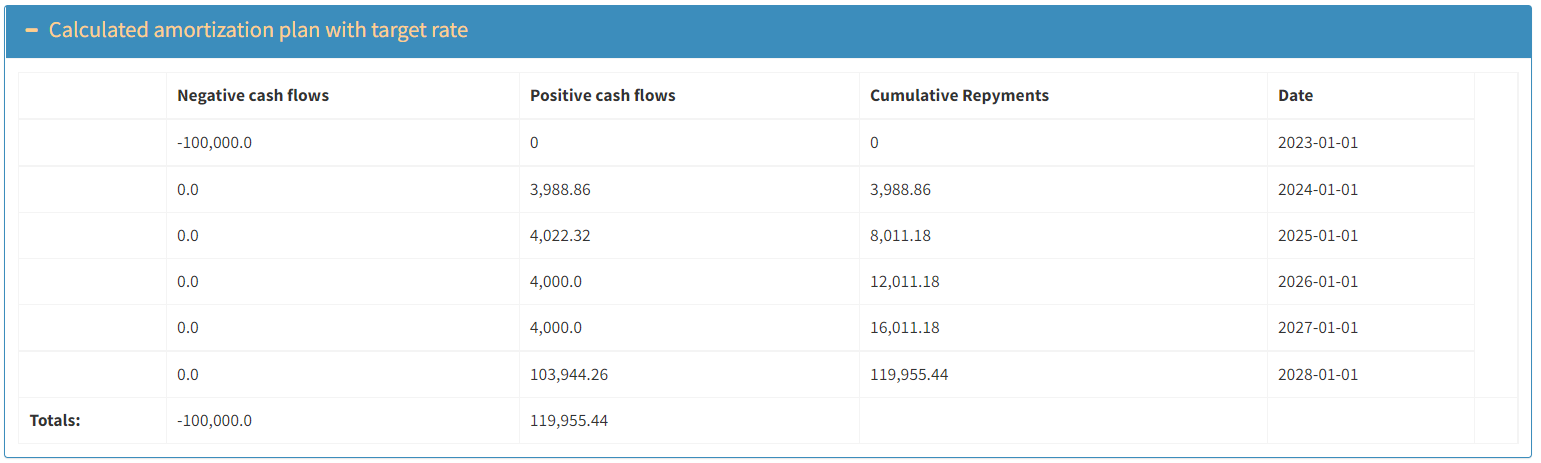

In order to fully understand the level of the Pricing model’s added value, we report below a case study in which a financial institution granted two loans having the same features to corporates that respectively have an AA and a BB rating, thus presenting different risk levels. The target amortization plan (that hence includes a target interest rate) built and delivered by the bank follows a bullet amortization method with the maturity corresponding to five years, as it can be observed in the table below:

{kind=link}

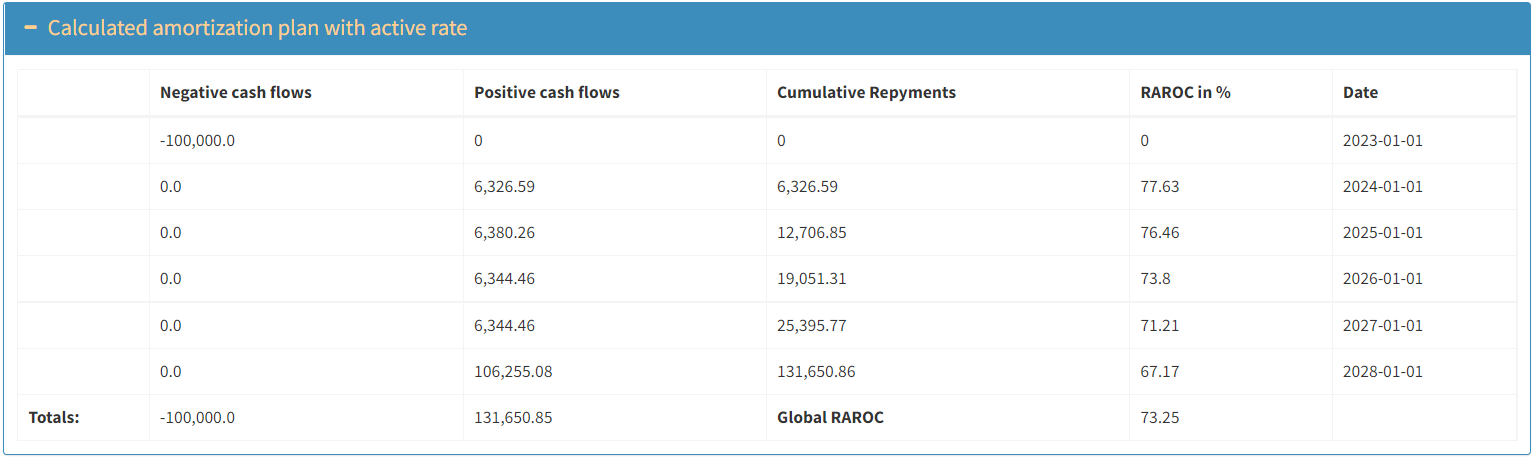

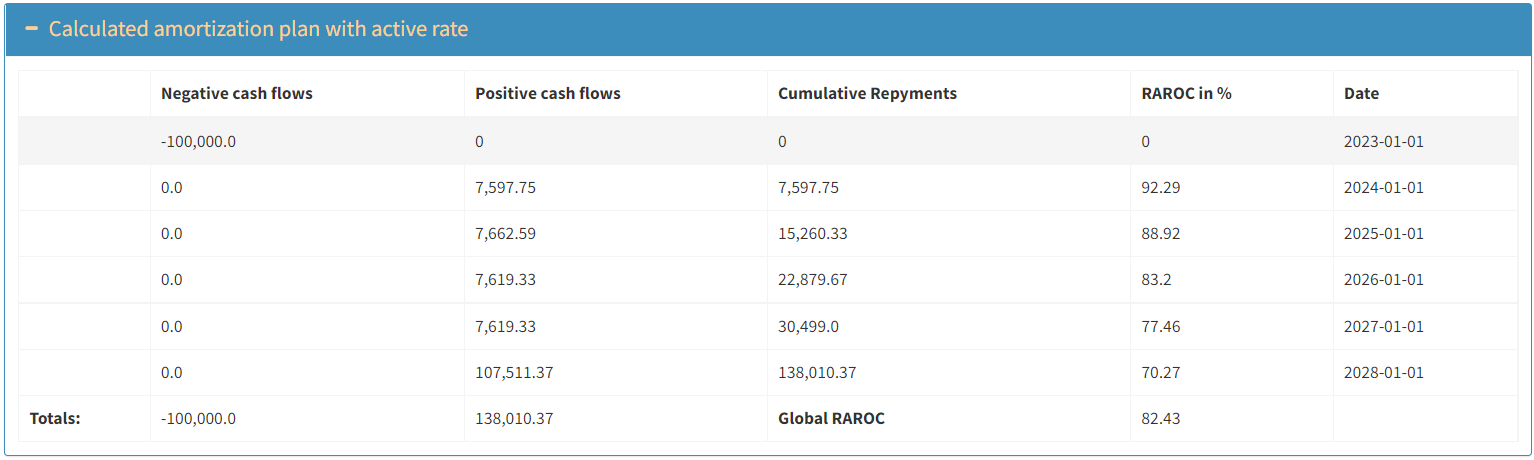

The result of modefinance’s analysis and comparison between the two enterprises is summed up in the two tables below:

{kind=link}

{kind=link}

As it can be noted, the target rate defined by the financial intermediary for both the AA company (table 2) and the BB company (table 3) amounts to 4%, and the Net Present Value is equal for both corporates. Moving on to the next step, at the time when the target rate is applied to the NPV, we obtain the risk-adjusted NPV, which presents a different value in the two cases: in both, the value of future cash flows is low, given that we consider the enterprises’ probability of default. However, the NPV of the AA company turns out to be higher than the same metric of the BB company, as well as the risk-adjusted NPV of both enterprises is lower that the same value that does not include the risk.

The second part of both tables is dedicated to risk-adjusted KPIs calculated on the Active Rate, instead of the target rate delivered by the bank, which brings us to the modefinance Pricing model output. As already mentioned, the active rate equals the sum of the target rate, risk free rate and spread of risk. The first and most important point to be highlighted is that the active rate varies between the two corporates presenting different levels of risk, thus modifying all risk-based KPIs. Namely, the target rate for both enterprises is fixed at 4%, while the active rate amounts to 6,34% and 7,62% for the AA and the BB company, respectively, given the fact that providing liquidity to a lower credit rating enterprise holds a higher risk. The definition of the interest rate to be applied based on the probability of default’s calculations results in the risk-adjusted NPV on active rate output, which brings the financial institution 10 000 euro for the AA company and 17 000 euro for the BB company net value on the loan. This implies that the financial intermediary that applies the interest rate carried out by modefinance’s Pricing model, should be and is compensated for granting a loan to a riskier company.

{kind=link}

{kind=link}

Once that we have considered the performance of the risk-adjusted NPV with the application of a different active rate for the two companies taken under analysis, it is time to compare the two amortization plans that implement the active rate with the target amortization plan (described in the two tables above). To begin with, the target amortization plan is the same for the two companies presenting different levels of creditworthiness, whereas the application of the Pricing model and its active rate that takes risk into account, carries out two different amortization schedules, due to the fact that two different interest rates have been given to the two enterprises.

Eventually, what is essential to highlight once again is the fair-value principle upon which modefinance’s Pricing model is based. As it appears to be clear from the analysis above, the risk-adjusted NPV defined with the active rate is higher than the one calculated with the target rate, but the difference does not appear to be excessive since it includes the risk, which makes possible for the financial institution to gain as much as possible from a loan it granted, denying the enterprise’s likelihood of not being able to repay their debts.

Today, the loan granting process management that takes risk into account can be considered at the forefront for any financial intermediary, from traditional banks to any other kind of financial institution. In such a time of great uncertainty, when global corporates are facing difficulties and liquidity problems related to the economic and social crisis, it is crucial to anticipate it with appropriate cutting-edge tech tools and with an increased awareness in facing risk situations, meeting the borrower’s needs of accessing non-excessive rates at the same time. It means being able to grow, bringing value to your clients and to the entire financial ecosystem.