Corporate Credit Rating (Solicited) for I.M.I. S.P.A.: A3- (First Issuance)

modefinance published the Solicited Corporate Credit Rating of I.M.I. S.P.A. on its CRA website, and the rating assigned to the entity is A3- (First Issuance). The analysis revealed it is a good company with good capability of repaying financial obligations and little affected by adverse economic scenarios.

I.M.I. S.P.A. is a company based in Naples. It was founded in late 2012 as a Limited Liability Company from the business initiative of two professionals in the electrical and mechanical sector. The newly established company dealt with the construction of both industrial electrical systems and of industrial electrical panels and their components.

Over time, although the company structure has changed, it has maintained the founding principles of craftsmanship, professionalism, and expertise of its of human resources. In a short period of time, the company's growth has allowed it to sub-contract and collaborate with companies with international orders.

Key Rating Assumption

I.M.I. S.P.A. shows a balanced economic-financial situation with very solid solvency and profitability conditions. The growth in turnover and total assets is balanced. Liquidity management appears consistent with corporate growth and highlights the important contribution of self-financed liquidity, the company’s driving force. The analysis of the Central Credit Register reveals a consistent and flawless situation.

With regard to governance, the Company has changed its legal form from a Limited Liability Company (S.r.l.) to a Joint-Stock Company (S.p.A.) improving corporate information as well as the structure by expanding governance and organization. Although it is a young company, it can already be considered among the market leaders. The management reacted quickly to the limitations of the pandemic and managed to increase turnover in 2020.

The comparison with the reference peer group revealed that the Company is growing significantly, having already reached an important position among those of the analysis sample. The capital structure and the profitability achieved make it very competitive.

At the sectoral level, the peer group shows an overall sufficient state of health with an improvement in solvency over time. The profitability does not show peaks, but is sufficiently profitable.

From a macroeconomic point of view, current and short-term future conditions appear critical and, in any case, a growth without lasting government stability does not appear predictable. The ongoing health crisis will inevitably impact the European economy throughout 2021.

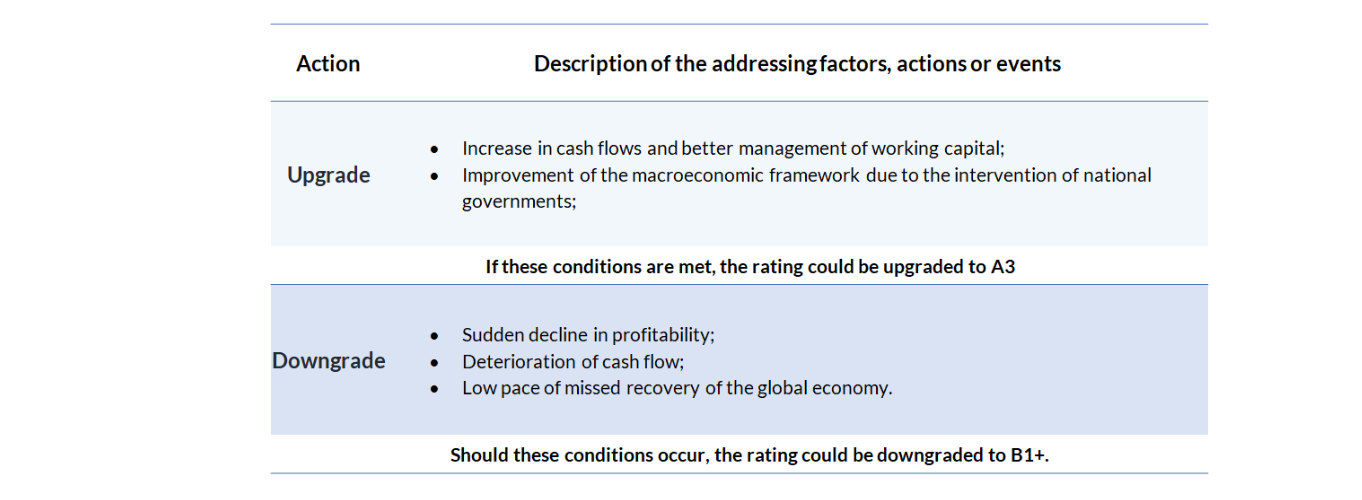

Sensitivity Analysis

In the following table, the addressing factors, actions or events that could lead to an upgrade or a downgrade are summarized:

{kind=link}

Important

The present Corporate Credit rating is issued by modefinance under EU Regulation N. 1060/2009 and following amendments.

The present rating is solicited, and based on both private and public information. The rated entity and/or related third parties have provided all private information used. modefinance had access to some accounts and other relevant internal documents of the rated entity and/or related third parties. Solicited and unsolicited ratings issued by modefinance are of comparable quality, as the solicitation status has no effect on methodologies used. More comprehensive information on modefinance Corporate Credit Ratings are available here.

The present Corporate Credit Rating is issued on MORE Methodology 2.0 and Rating Methodology 1.0. A comprehensive description of both methodologies, as well as information on modefinance Rating Scale and Mappings, is available here. For information on historical default rates of modefinance Corporate Credit Ratings please refer to ESMA Central Repository and ESMA European Rating Platform.

modefinance refers to default as a company under bankruptcy, or under liquidation status, or under administration or for which missed payments on a financial obligation are officially recorded.

The quality of the information available on the rated entity and used to determine the present rating was judged by modefinance as satisfactory. Please note that modefinance does not perform any audit activity and is not in a position to guarantee the accuracy of any information used and/or reported in the present document. As such, modefinance can accept no liability whatsoever for actions taken based on any information that may subsequently prove to be incorrect.

The present credit rating was notified to the rated entity in order to identify potential factual errors, as prescribed by the CRA Regulation.

No amendments were applied after the notification process.

The rated entity is not a buyer of ancillary services provided by modefinance.

The rating action issued by modefinance was performed independently. The analysts, members of the rating team involved in the process, modefinance Srl and its members and shareholders do not have any conflicts of interest in relation to the Rated Entity and/or Related Third Parties. If in the future a potential conflict of interest is identified in relation to the persons reported above, modefinance Ratings will provide the appropriate information and if necessary the rating will be withdrawn.

The present Credit Rating is an opinion of the general creditworthiness that modefinance issues on the rated entity, and should be relied upon to a limited degree. The issued rating is subject to an ongoing monitoring until withdrawal.

Contacts

Head Analyst – Fabio Politelli (Rating Analyst)

fabio.politelli@modefinance.com

+39 040 3756740

Assistant Analyst – Chiara Di Piazza (Rating Analyst)

chiara.dipiazza@modefinance.com

+39 040 3756740

Responsible for Rating Approval – Pinar Dilek

pinar.dilek@modefinance.com

+39 040 3756740