Introduction

Invoice financing is a thriving market in Europe.

Due to the credit crunch of the banking system and the late payment of the Public Administration, an increasing number of companies resort to this funding instrument to obtain liquidity and improve the NFP.

But as demand increases, so does the need for fast and accurate risk assessment tools. In this article, we'll see how to use oplon Risk Platform to evaluate the clients' creditworthiness and thus reduce the times of due diligence processes from weeks to a few minutes.

The challenge

In order to reduce the risk to incur non-performing receivables, invoice financing transactions require a careful analysis of the creditworthiness of the assignor and its debtors.

Making such a process as quick as possible is the main challenge today. The digital revolution made paper-based procedures outdated, pushing customers towards online services able to provide credit promptly.

However, while much has been done for the digitalization of the user journey, back-end due diligence and evaluation activities suffer too often from time-consuming procedures.

To compete on the market today, the whole invoice financing process, from the quote request to the eligibility decision, should take just 3 days.

oplon Risk Platform

Of course, the promptness of the result can not undermine the analysis’ accuracy.

oplon Risk Platform provides AI-based analysis models for credit risk evaluation that allows to automate the whole due diligence process.

As Fintech Rating Agency, we embedded our in-house AI-based tools in a Fintech solution for risk assessment, automating each step of the decision-making process; from data acquisition to the final approval.

In oplon Risk Platform, factors and digital lenders can find all the analysis models they need to perform a credit risk analysis in a few minutes, such as:

- MORE Score: it automatically calculates the company's credit score from the balance sheet data;

- the debt-capacity model: it automates the budgeting forecast (up to 5 years) and allows to perform stress-test on key variables;

- qualitative questionnaires: they improve the analysis through specific multiple-choice questions;

- the evaluation model of the Central Credit Register: it automatically read the Central Credit Register's file and provides an evaluation of the data in it;

- the massive analysis model: allows to calculate, from the indication of the VAT number only, the credit score and the probability of default of each debtor. The results of the massive analysis influence the assessment of the assignor.

The analysis models to be included in the process are defined when setting up the platform. New models can also be developed or customized upon request. Factors can for example request invoice pricing models developed ad-hoc on internal policies.

{kind=link}

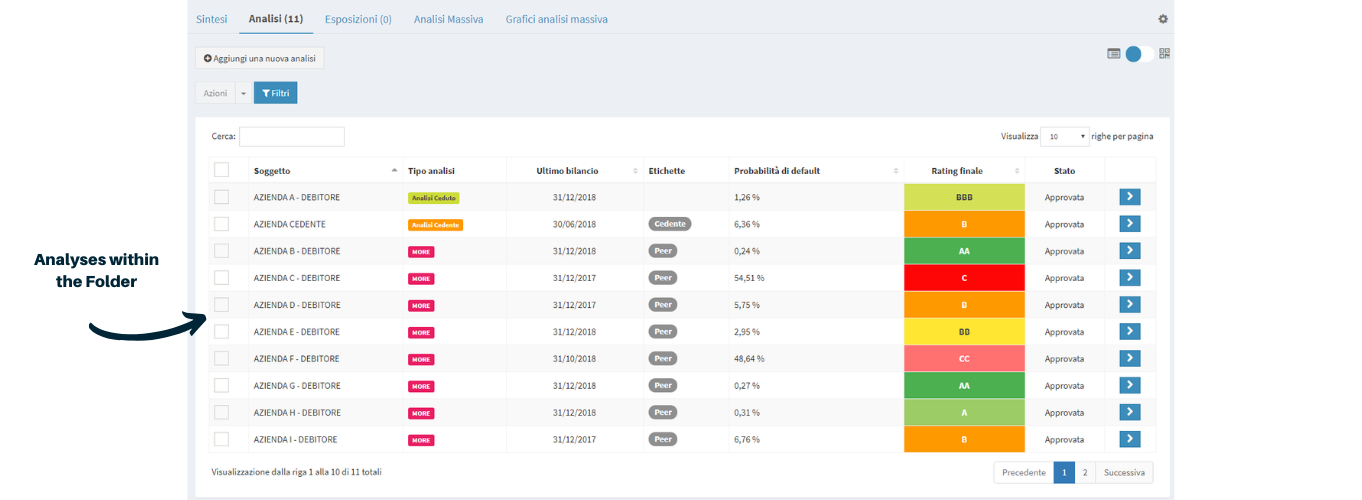

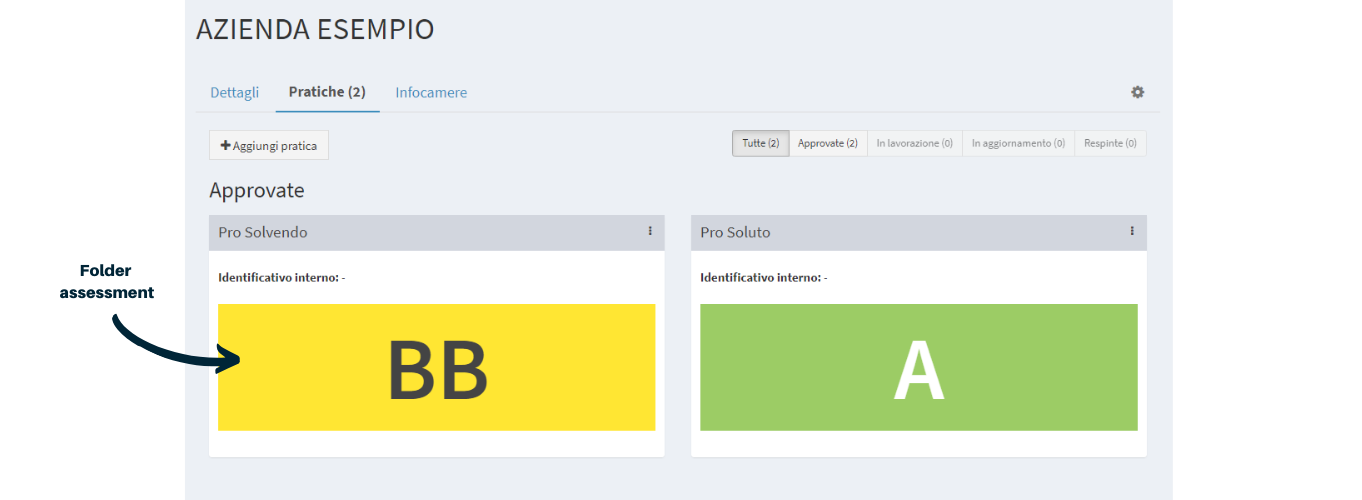

Folder, Analysis and Steps are the platform’s main architecture elements.

Within the same Folder you can perform different analyses on different companies. Once chosen a folder, the factor can perform accurate creditworthiness analyses on the assignor and all the debtors involved in the factoring transaction.

{kind=link}

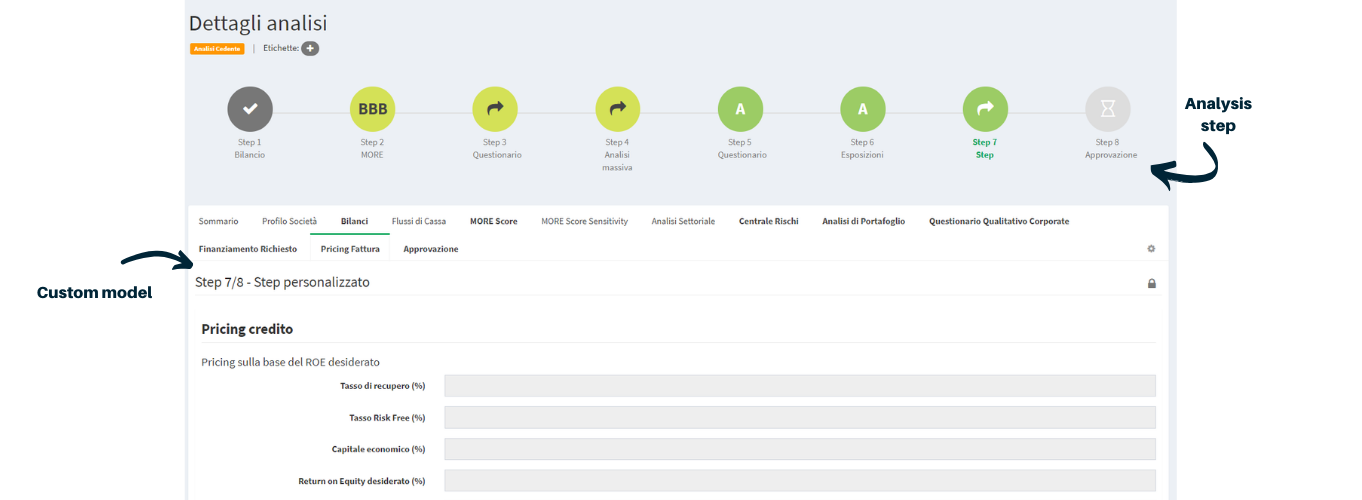

Each Analysis is divided into Steps and results in a credit score.

The number of steps depends on the models that the user has chosen to include in the process. The results of all the Analyses contribute (to the extent established by the client) to the evaluation assigned to the Folder.

{kind=link}

The whole evaluation process takes just a few minutes.

In this article we have provided a generic overview of oplon’s functionalities for factoring. In the following one we will see an example of a factoring analysis within the platform.