Solicited Corporate Credit Rating for ECOSERVIM SRL: B1+ (Upgrade)

modefinance published the Solicited Corporate Credit Rating of ECOSERVIM SRL on the website and the rating assigned to the entity is B1+ (Upgrade). The analysis revealed how the company has adequate capabilities to honor obligations and can face adverse and changing economic conditions in the medium and long term.

ECOSERVIM S.R.L. was founded in 1996, although the company's roots go back to the 1970s thanks to the entrepreneurial initiative of Matteo Bonini, who set up a small thermo-hydraulic services company. Today, the company is led by his son Gianluca, who over the years has expanded the range of services offered to companies and individuals throughout the region, giving rise to the group of the same name active in the energy and facility management sectors, with a particular focus on plumbing, energy saving, construction and heating/cooling. The company's operations from the financial years 2020 and 2021 experienced a strong development linked to the Superbonus and Ecobonus tax bonuses.

Key Rating Assumptions

The Company's economic and financial situation is adequate, characterized by a strong growth in turnover, which led to an increase in operating margins and net profit. The profitability of equity and shareholders' equity remained solid. However, the increase in operations led to an increase in the incidence of production costs, resulting in a decrease in the operating margin. Capitalization is consistent with the sources of financing used. Solvency appears adequate: liabilities are mainly commercial and with a short-term due.

The net financial position shows a positive balance, largely supported by the gross operating margin. Total assets consist mainly of current assets, in particularly trade receivables, cash and cash equivalents. The short-term sources/utilization- ratio confirms adequate current ratio and quick ratio indicators.

The cash flow analysis confirms the company’s ability to generate resources through income flows and adequate management of working capital dynamics. During the financial period, the company has reduced its reliance on financial debt, which shows no critical issues, as highlighted by the analysis of the Italian Central Credit Register.

The ownership of the group can be traced back to the director Mr. Gianluca Bonini, together with Next Holding S.p.A., which holds 10% of the shares as financial investor. The governance structure is adequate for the size of the company: the administrative body as well as the control body are collective. Furthermore, the Company has appointed AURE S.R.L. as auditing company.

Compared to the peer group, The Company ranks just below the 100th percentile in terms of turnover. The positioning concerning profitability is also robust, just below the 90th percentile. More contained, but still adequate, is the positioning of solvency, aligned with the 60th percentile. The peer group shows overall adequate levels of solvency, liquidity and profitability. Furthermore, the distribution of companies in the sector shows a concentration of companies above the sufficiency threshold, underlining the health of the peer group.

The ISTAT index shows the first sign of a slowdown in construction (including ordinary maintenance) compared to the first 5 months of 2022. confirmed by the decrease in the number of hours worked (January-April 2023 over 2022). The decline recorded in the residential sector is largely offset by the growth in public works, boosted by the realization of works related to the NRP. The “Super bonus” decree, together with the other tax incentives inherent to the construction and energy efficiency sector, plays a major role in the growth of the sector and of the national economy. However, the limitations related to the purchase of credits by public entities and the abolition of credit assignment or invoice discount for future interventions have led to a significant depowering of the maneuver.

The macroeconomic framework for Italy suggests modest growth in 2023, due to the impact of the rise in interest rates, inflation and unfavorable economic conditions. This would be followed by a period of higher than pre-pandemic growth. The anticipated general election delivered a solid majority, resulting in less governmental instability. However, the new cabinet will have to follow the agenda of the previous government in order to complete the post-pandemic recovery plan. Macroeconomic forecast data could be revised upward.

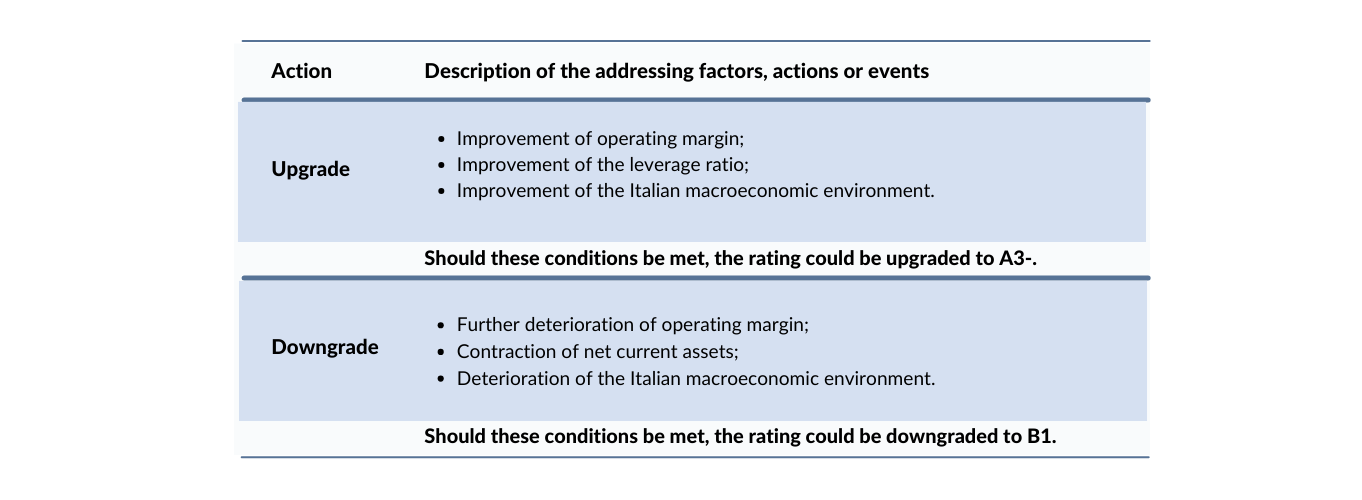

Sensitivity Analysis

In the following table, the addressing factors, actions or events that could lead to an upgrade or a downgrade are summarized:

{kind=link}

Important

The present Corporate Credit rating is issued by modefinance under EU Regulation 1060/2009 and following amendments.

The present rating is solicited and is based on both private and public information. The rated entity and/or related third parties have provided all private information used. modefinance had access to some accounts and other relevant internal documents of the rated entity and/or related third parties. Solicited and unsolicited ratings issued by modefinance are of comparable quality, as the solicitation status has no effect on methodologies used. More comprehensive information on modefinance Corporate Credit Ratings are available at http://cra.modefinance.com/en

The present Corporate Credit Rating is issued on MORE Methodology 2.0 and Rating Methodology 1.0. A comprehensive description of both methodologies, as well as information on modefinance Rating Scale and Mappings, is available at http://cra.modefinance.com/en/methodologies.

For information on historical default rates of modefinance Corporate Credit Ratings please refer to ESMA Central Repository and ESMA European Rating Platform.

modefinance refers to default as a company under bankruptcy, or under liquidation status, or under administration or for which missed payments on a financial obligation are officially recorded.

The quality of the information available on the rated entity and used to determine the present rating was judged by modefinance as satisfactory. Please note that modefinance does not perform any audit activity and is not in a position to guarantee the accuracy of any information used and/or reported in the present document. As such, modefinance can accept no liability whatsoever for actions taken based on any information that may subsequently prove to be incorrect.

The present credit rating was notified to the rated entity in order to identify potential factual errors, as prescribed by the CRA Regulation.

No amendments were applied after the notification process.

The rated entity is a buyer of ancillary services provided by modefinance (private corporate rating). modefinance ensures that such situation does not imply a conflict of interest in the issuance of the present credit rating.

The rating action issued by modefinance was performed independently. The analysts, members of the rating team involved in the process, modefinance Srl and its members and shareholders do not have any conflicts of interest in relation to the Rated Entity and/or Related Third Parties. If in the future a potential conflict of interest is identified in relation to the persons reported above, modefinance Ratings will provide the appropriate information and if necessary the rating will be withdrawn.

The present Credit Rating is an opinion of the general creditworthiness that modefinance issues on the rated entity, and should be relied upon to a limited degree. The issued rating is subject to an ongoing monitoring until withdrawal.

Contacts

Head Analyst - Gabriele Fadon, Rating Analyst

gabriele.fadon@modefinance.com

Responsible for Rating Approval - Pinar Dilek, Rating Process Manager

pinar.dilek@modefinance.com