modefinance UnsolicitedCorporate Credit Rating for FINECOBANK BANCA FINECO S.P.A.: A2- (Affirm)

modefinance published on its CRA website the Unsolicited Corporate Credit Rating (Affirm) of FINECOBANK BANCA FINECO S.P.A., reviewed after the publication of 2019 financial statement. modefinance confirms the rating previously assigned to the entity, equal to A2- (Affirm). The bank has indeed confirmed its very good capability of repaying the financial obligations

Key Rating Assumptions

Reason behind the review: Publication of 2019 consolidated annual financial statement.

The reasons that have driven this decision are:

- The overall financial and economic situation of FinecoBank is good and stable over the period considered. The capital adequacy is higher than the industry’s level and above the minimum requirement of ECB. The profitability is rather high even if the value of the ROE ratio has slightly decreased. The bank’s overall situation is good.

- The bank’s assets portfolio is mainly composed of interest-earning assets, which account for 97.69% of total assets. Most of the earning assets are Hold To Collect instruments (98.71%), reflecting the long-term financial strategy pursued by the bank. The HTC financial assets include debt instruments (13,096 million EUR) and a notable yet marginal credit exposure towards clients (3,676 million EUR), mainly consisting of private and families’ loans. There was a slight decrease in the amount of customer loans and operating revenues compared to the previous year, when both were equal to 90/100. In the meantime, FinecoBank improved its position in terms of capitalization, having set aside a substantial regulatory capital. The value of Total Capital Ratio is higher than in 2018 and it’s equal to 33.67%.

- Founded in 1999, FinecoBank is a quite newly established bank but with an innovative business model, being a pioneer in the online banking market. FinecoBank was a pioneer in Italy in the digitalization of banking activities and mainly provides online services. This peculiarity has positively affected the bank’s activities during the Covid-19 crisis.

- In July 2019, the former main shareholder Unicredit S.p.A. sold its stake in FinecoBank. This event represented an important opportunity for Fineco to confirm its operational and strategic independence from the Italian baking system. The key figure in FinecoBank is the Chief Executive Officer Alessandro Foti. He joined Fineco Holding S.p.A. in 1989 as a manager with responsibility for capital markets. In December 2000, he was appointed CEO of the new banking company FinecoBank S.p.A.

- FinecoBank overperformed the peer group in all the considered areas: the rated entity recorded very good values in terms of size, profitability, and assets quality. Over the last three years, the peer group has improved the asset quality, while remains stable in the other considered area.

- To support the Italian business environment, during COVID-19, the Italian government has launched the Liquidity Decree, where the role of the banking system is essential. At the moment of this analysis, the above-mentioned measure is under development and the first results revealed a time-consuming lending process, also due to the difficult communication between companies, banks, and guarantors. Nonetheless, the Decree could encourage the banking system to improve the credit disbursement process in terms of allocative efficiency.

- The last release of the IMF estimates a -7.1%. GDP growth rate for the eurozone in 2020. Due to the unprecedented economic, financial, and social crisis originated by the COVID-19 lockdown, many European may encounter difficulties in recovery. The intervention of the European government and the European Commission will affect positively the economy.

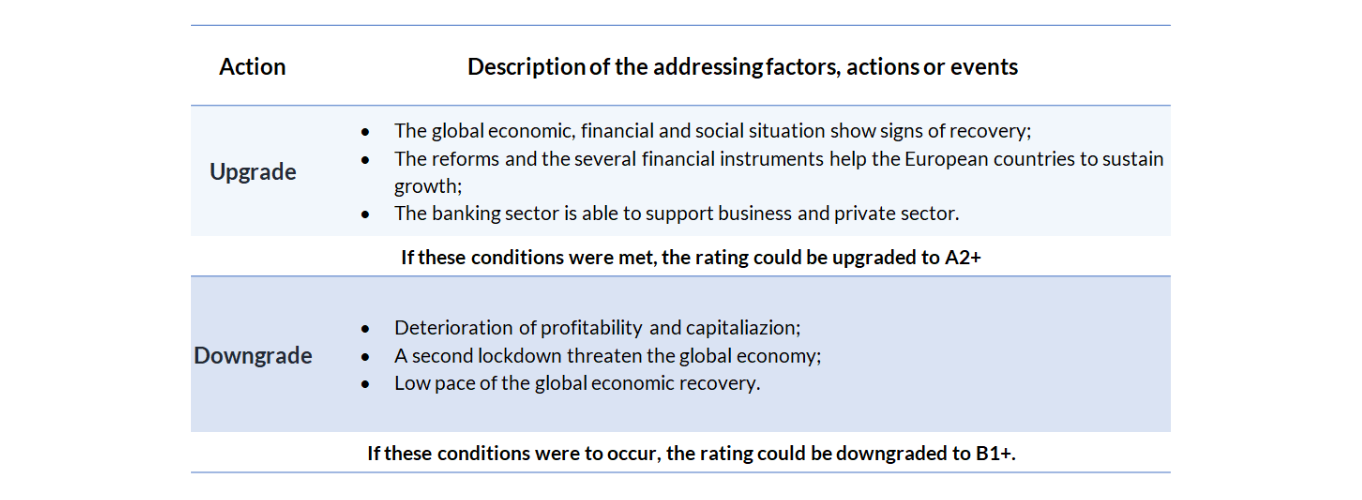

Sensitivity Analysis

The following table summarizes the addressing factors, actions or events that could lead to a rating upgrade or downgrade:

{kind=link}

Important

The present Corporate Credit rating is issued by modefinance under EU Regulation 1060/2009 and following amendments.

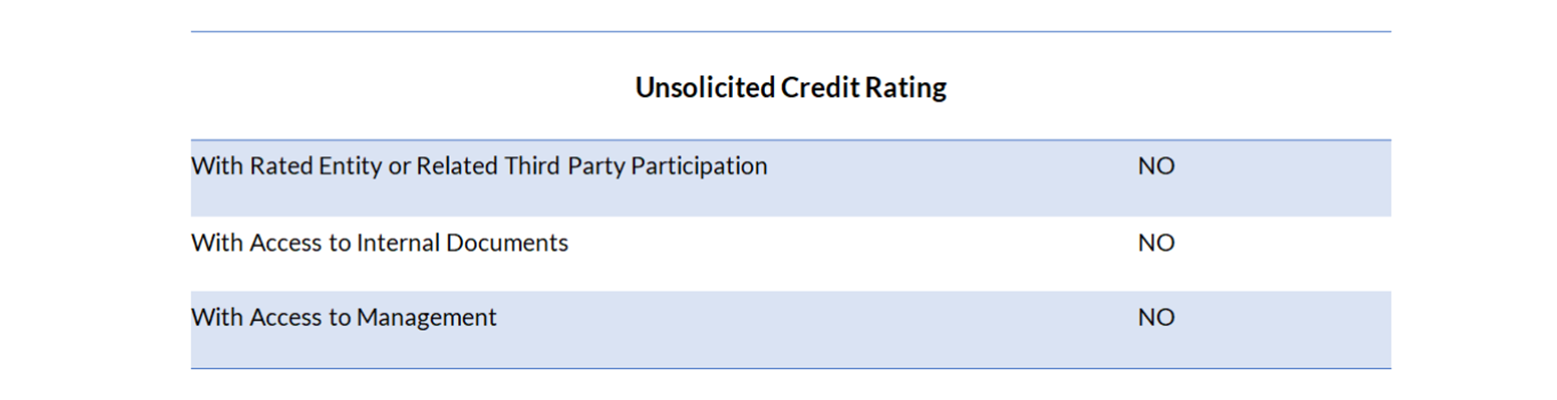

The present rating is unsolicited: the rated entity and/or related third parties have not participated in the rating process and modefinance has no access to accounts or other relevant internal documents of the rated entity and/or related third parties.

{kind=link}

Solicited and unsolicited ratings issued by modefinance are of comparable quality, as the solicitation status does not affect the methodologies used. More comprehensive information on modefinance Corporate Credit Ratings is available here.

The present Corporate Credit Rating is issued on MORE Score Methodology for banks 1.0 and Rating Methodology 1.0. A comprehensive description of both methodologies, as well as information on modefinance's Rating Scale and Mappings, is available here.

For information on historical default rates of modefinance Corporate Credit Ratings please refer to ESMA Central Repository and ESMA European Rating Platform.

modefinance refers to default as a company under bankruptcy, or under liquidation status, or under administration or for which missed payments on a financial obligation are officially recorded.

The quality of the information available on the rated entity and used to determine the present rating was judged by modefinance as satisfactory. Please note that modefinance, however, is not in a position to guarantee the accuracy of that information. As such, modefinance can accept no liability whatsoever for actions taken based on any information that may subsequently prove to be incorrect.

The present credit rating was notified to the rated entity in order to identify potential factual errors, as prescribed by the CRA Regulation.

No amendments were applied after the notification process.

The Rated Entity or Related Third Party has not purchased ancillary services from modefinance. The rating action issued by modefinance was performed independently. The analysts, members of the rating team involved in the process, modefinance Srl and its members and shareholders do not have any conflicts of interest concerning the Rated Entity and/or Related Third Parties. If in the future a potential conflict of interest related to the persons reported above is identified, modefinance Ratings will provide the appropriate information and if necessary the rating will be withdrawn.

The present Credit Rating is an opinion of the general creditworthiness that modefinance issues on the rated entity, and should be relied upon to a limited degree. The issued rating is subject to ongoing monitoring until withdrawal.

Contacts

Christian Raimondo – Head Analyst

christian.raimondo@modefinance.com

+39 040 3756740

Eva Vocci – Assistant Analyst

eva.vocci@modefinance.com

+39 040 3756740

Pinar Dilek – Responsible for Rating Approval

pinar.dilek@modefinance.com

+39 040 3756740