Unsolicited Corporate Credit Rating for FINECOBANK BANCA FINECO S.P.A.: A2- (Affirm)

modefinance published on its CRA website the Solicited Corporate Credit Rating of FINECOBANK BANCA FINECO S.P.A., reviewed after the publication of the half-year accounts 2020. modefinance confirms the rating previously assigned to the entity, equals to A2- (affirm). The company has confirmed its high capability to meet its financial obligations, proving to be a very good bank with very good capability of repaying financial obligations.

FinecoBank Banca Fineco Spa was established in the late Seventies as a company specialized in factoring and leasing operations. In1999, after several years of M&A, FinecoBank started looking at online services related to corporate finance, providing highly customized solutions in order to set the standard in a highly competitive environment.

Key Rating Assumptions

FinecoBank was established in 1999, so it’s a very young institution but with an innovative business model compared to the reference market, being Fineco a pioneer in the online banking market. FinecoBank S.p.A. was among the first in Italy to digitalize the banking industry through a service mainly available online, actually a virtual banking service; this factor favored bank’s activities during the Covid-19 crisis.

The key figure in FinecoBank is the Chief Executive Officer Alessandro Foti. He joined Fineco Holding S.p.A. in 1989 as a manager with responsibility for capital markets. In December 2000, he was appointed Chief Executive Officer of the new banking company FinecoBank S.p.A. Despite the difficult and challenging period related to the Coronavirus outbreak, Fineco registered very good and encouraging values in all considered areas, increasing the overall amounts of loans to customers, keeping unchanged the level of non-performing loans and growing in the profitability area with a good level in net interest income and operating revenues. The capitalization of the company is still strengthening with extremely good values in the regulatory capital ratios.

Compared to its pertaining sector, FinecoBank overperformed the peer group in all the considered areas: the rated entity recorded very good values in terms of size, profitability and asset quality. The peer group has improved in the last three years in asset quality, while still remains stable in the other considered area.

Regarding the relevant news of the industry, the measures put in place by the Italian government are under development. The first results show a slow granting process, also due to the problematic communication between companies, banks and guarantors. At the same time, this measure can help the banking system to improve its granting process in terms of allocative efficiency. The situation is uncertain more than ever and it will be necessary to wait until the publication of the first 2021 annual reports of the banks to be published, because the half-year reports demonstrated a deterioration in the creditworthiness, but bearable by the bank and by the system, but all the elements have been reported will have a negative impact on the banking system, not only on Italian banks. Maybe the idea of a European bad bank (for non-performing loans) could help the European banking system and it is a good sign the opening from the European Institutions.

Furthermore, the last release of the IFM shows a GDP growth rate (estimated) for the euro area in 2020 of -7.1%. The economic, financial and social crisis originated by the Covid-19 lockdown is unprecedented and it will increase unemployment rate, decrease GDP growth rate and the consumption will be difficult to recover in all European countries. The intervention of European government and the European Commission will affect positively the economy.

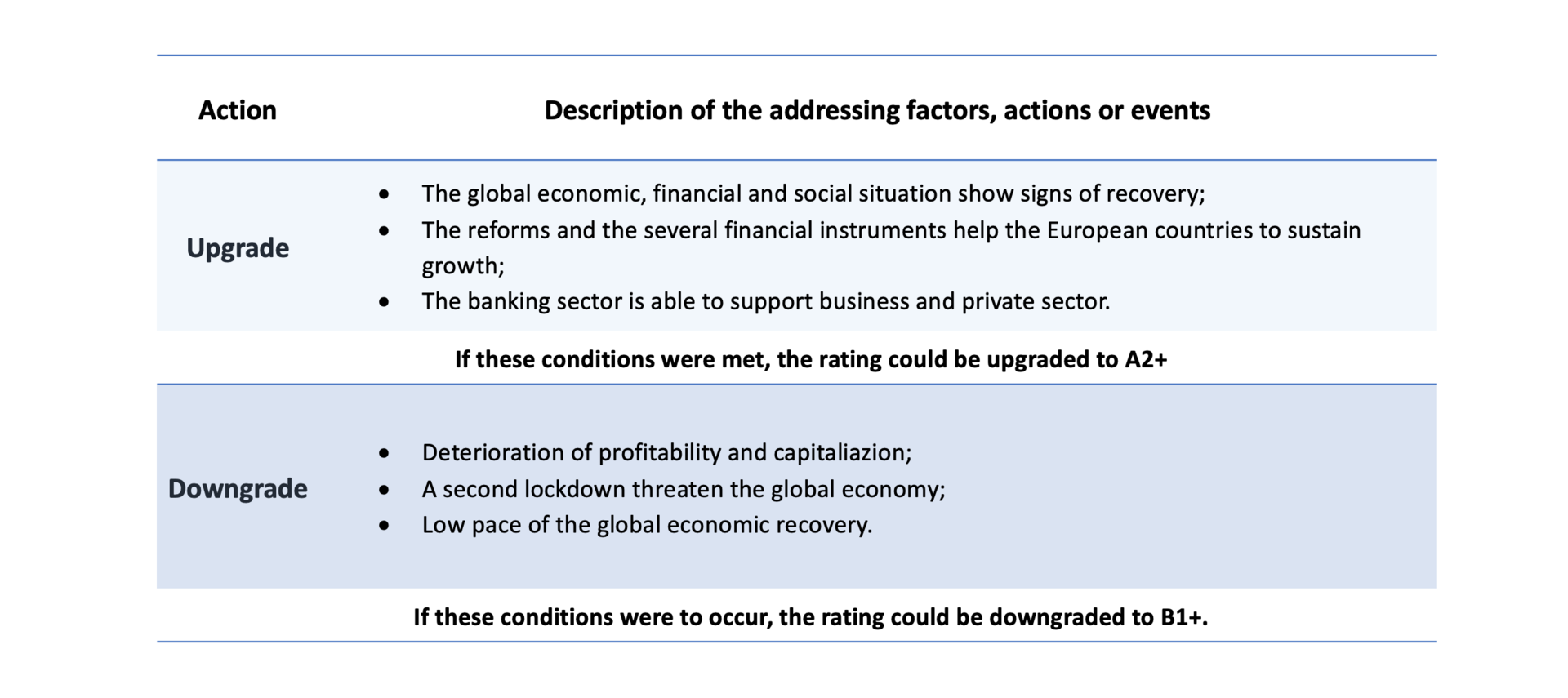

Sensitivity Analysis

In the following table, the addressing factors, actions or events that could lead to an upgrade or a downgrade are summarized:

{kind=link}

Important

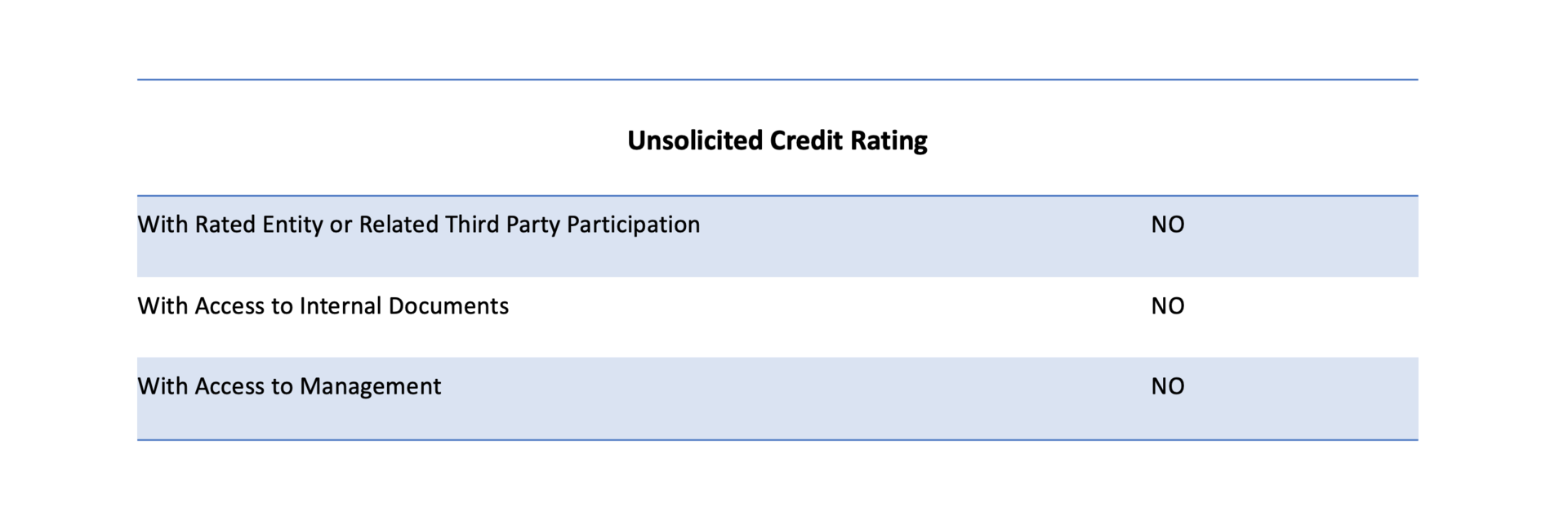

The present Corporate Credit rating is issued by modefinance under EU Regulation 1060/2009 and following amendments.The present rating is unsolicited: the rated entity and/or related third parties have not participated in the rating process and modefinance has no access to accounts or other relevant internal documents of the rated entity and/or related third parties.

{kind=link}

Solicited and unsolicited ratings issued by modefinance are of comparable quality, as the solicitation status has no effect on methodologies used.

More comprehensive information on modefinance Corporate Credit Ratings are available on this link. The present Corporate Credit Rating is issued on MORE for Banks Methodology 2.0 and Rating for Banks Methodology 1.0.

A comprehensive description of both methodologies, as well as information on modefinance Rating Scale and Mappings, is available at https://cra.modefinance.com/en/methodologies/companies.

For information on historical default rates of modefinance Corporate Credit Ratings please refer to ESMA Central Repository and ESMA European Rating Platform.

modefinance refers to default as a company under bankruptcy, or under liquidation status, or under administration or for which missed payments on a financial obligation are officially recorded. The quality of the information available on the rated entity and used to determine the present rating was judged by modefinance as satisfactory. Please note that modefinance however is not in a position to guarantee the accuracy of those information. As such, modefinance can accept no liability whatsoever for actions taken based on any information that may subsequently prove to be incorrect.

The present credit rating was notified to the rated entity in order to identify potential factual errors, as prescribed by the CRA Regulation.No amendments were applied after the notification process.

The Rated Entity or Related Third Party has not purchased ancillary services from modefinance. The rating action issued by modefinance was performed independently. The analysts, members of the rating team involved in the process, modefinance Srl and its members and shareholders do not have any conflicts of interest in relation to the Rated Entity and/or Related Third Parties. If in the future a potential conflict of interest is identified in relation to the persons reported above, modefinance Ratings will provide the appropriate information and if necessary, the rating will be withdrawn.

The present Credit Rating is an opinion of the general creditworthiness that modefinance issues on the rated entity and should be relied upon to a limited degree. The issued rating is subject to an ongoing monitoring until withdrawal.

Contacts

Eva Vocci - Head Analyst

eva.vocci@modefinance.com

+39 040 3756740

Christian Raimondo - Assistant Analyst

christian.raimondo@modefinance.com

+39 040 3756740

Pinar Dilek - Responsible for Rating Approval

pinar.dilek@modefinance.com

+39 040 3756740