Solicited Corporate Credit Rating for OENERGY S.P.A.: B1 (Upgrade)

modefinance published the Solicited Corporate Credit Rating of OENERGY S.P.A. on the CRA website and the rating assigned to the entity is B1 (upgrade). The analysis revealed that the company has an adequate economic-financial situation with average capability of repaying financial obligations and it is little affected by adverse economic scenarios.

OENERGY S.P.A. is a company operating since 2010 in the energy sector and is licensed for retail and wholesale of natural gas and electricity for any typology of customers, from households to large companies. In 2022, the Company managed the difficulties that emerged in the energy sector by repositioning itself on the market, strengthening its sales network and directly contracting institutional operators, making it possible to obtain very positive economic results, outperforming the management forecasts.

Key Rating Assumptions

The Company’s financial and economic situation shows a strong improvement compared to 2021. In particular, in 2022, the Company experienced a significant increase in sales revenue, which amounted to over EUR 40 million (+109% YoY). This result can be attributed to the general increase in gas and energy prices, as well as to the Company's strategies regarding procurement, sales network enlargement and customer portfolio management. The ratios of the profitability area confirm fully sufficient values, thanks to the growing operating margins and net income (€282,000). On the liquidity front, the Company shows a balanced management both in static terms and in the cash flow dynamics. Lastly, on the solvency front, the Company shows a sufficient level of capitalization and a sustainable financial debt in relation to EBITDA and total shareholders’ funds.

The Bank of Italy's Central Risks Report shows a correct management of credit lines.

The Company has an administrative body and a supervisory body, both in a collegial form, and adopts the organizational model ex-231/2001. The Company shows a straightforward corporate structure with a single shareholder represented by 'M2R HOLDING S.R.L.', fully controlled by the entrepreneur Mr. Mattia Pagani. In 2022 OENERGY S.P.A. acquired 30% of OEgreen S.p.A., which produces electricity from renewable sources. In terms of fixed investments, it is also worth highlighting that in 2022 OENERGY continued the implementation of the development plan aimed at building photovoltaic plants: in the next five years, the Company plans to install a fleet of ten plants in Italy, which will further boost the Company’s business. The investments were, moreover, entirely financed with the resources generated by core operations.

Compared to the reference peer group, the Company's positioning is above the 50th percentile in terms of size and solvency, while the performance in terms of profitability is poor, although it should be noted that the latter does not reward the appreciable growth in profitability ratios and economic margins, confirmed also in 2022. The sector peer group expresses sufficient solvency levels, while the financial balance appears adequate and profitability is good.

The energy sector in Italy has a considerable strategic importance and has gone through a period of strong and important changes due to recent geopolitical tensions. In recent weeks, however, the difficult situation seems to have normalized, with a partial reduction in commodity prices. The medium/long-term scenario still appears uncertain, but recovery.

Italian macroeconomic forecasts data shows a modest growth in 2023, characterized by rising rates and inflation. However, it is expected that this situation will be followed by a period of growth trending above pre-pandemic levels. For this reason, macroeconomic forecast data could be revised upwards.

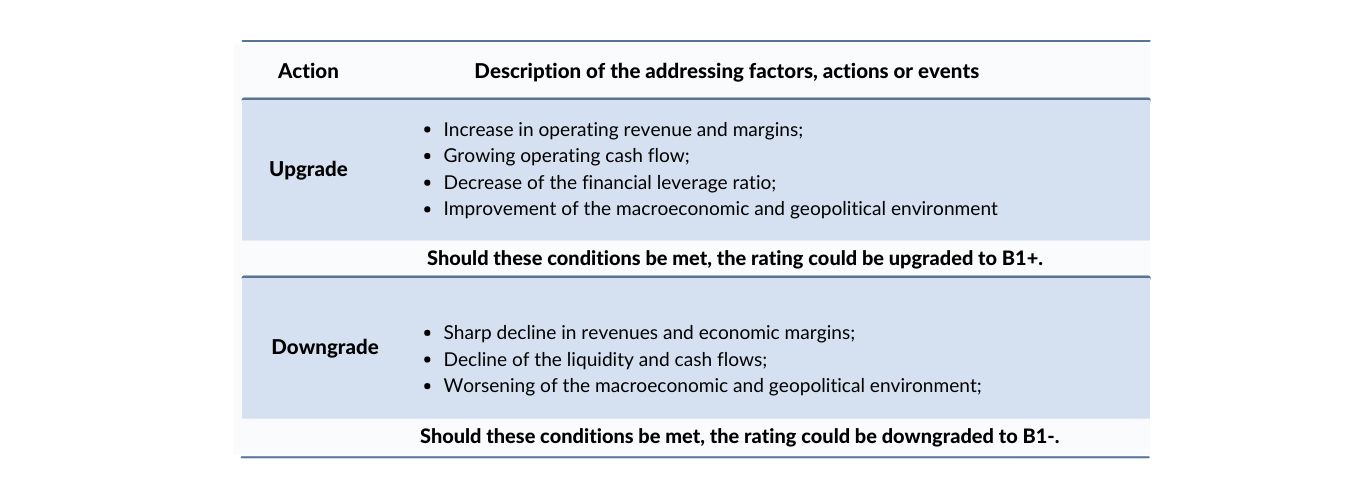

Sensitivity Analysis

In the following table, the addressing factors, actions or events that could lead to a rating upgrade or a downgrade are summarized:

{kind=link}

Important

The present Corporate Credit rating is issued by modefinance under EU Regulation N. 1060/2009 and following amendments.

The present rating is solicited, and based on both private and public information. The rated entity and/or related third parties have provided all private information used. modefinance had access to some accounts and other relevant internal documents of the rated entity and/or related third parties. Solicited and unsolicited ratings issued by modefinance are of comparable quality, as the solicitation status has no effect on methodologies used. More comprehensive information on modefinance Corporate Credit Ratings are available here.

The present Corporate Credit Rating is issued on MORE Methodology 2.0 and Rating Methodology 1.0. A comprehensive description of both methodologies, as well as information on modefinance Rating Scale and Mappings, is available here. For information on historical default rates of modefinance Corporate Credit Ratings please refer to ESMA Central Repository and ESMA European Rating Platform.

modefinance refers to default as a company under bankruptcy, or under liquidation status, or under administration or for which missed payments on a financial obligation are officially recorded.

The quality of the information available on the rated entity and used to determine the present rating was judged by modefinance as satisfactory. Please note that modefinance does not perform any audit activity and is not in a position to guarantee the accuracy of any information used and/or reported in the present document. As such, modefinance can accept no liability whatsoever for actions taken based on any information that may subsequently prove to be incorrect.

The present credit rating was notified to the rated entity in order to identify potential factual errors, as prescribed by the CRA Regulation. No amendments were applied after the notification process.

Modefinance provided the rated company with ancillary services (ESG Rating). Modefinance ensures that the provision of ancillary services does not present conflicts of interest with its credit rating activities.

The rating action issued by modefinance was performed independently. The analysts, members of the rating team involved in the process, modefinance Srl and its members and shareholders do not have any conflicts of interest in relation to the Rated Entity and/or Related Third Parties. If in the future a potential conflict of interest is identified in relation to the persons reported above, modefinance Ratings will provide the appropriate information and if necessary the rating will be withdrawn.

The present Credit Rating is an opinion of the general creditworthiness that modefinance issues on the rated entity, and should be relied upon to a limited degree. The issued rating is subject to an ongoing monitoring until withdrawal.

Contacts

Head Analyst – Elisa Graffi (Rating Analyst)

Responsible for Rating Approval – Pinar Dilek (Rating Process Manager)