According to the definition, an amortization schedule is a table that provides details on payments for an amortizing loan, each of the installments consisting of a portion going towards a capital share and another consisting of interests. Namely, an amortization plan is the detailed repayment schedule between a financial institution and its customers. That is why it is crucial for a bank or another financial institution to be able to trust its clients on their creditworthiness when defining the plan, which makes having a quality and dynamic amortization plan highly necessary. Moreover, it is important to highlight that the world we are living in is strongly hit by an economic, environmental, and social crisis, the impact of which is huge nowadays. With this in mind, being able to observe the reliability of an enterprise to repay its debts and consider the risk faced while granting a loan, can be fundamental for a financial intermediary.

In this context, modefinance took a further step in the evolution of its technological offer to financial institutions: launching of the Amortization Plan Over Uncertainty (APOU) model and the Pricing model that is derived from it, based on the principle of fair value, in order to include the risk in the process of building and evaluating an amortization schedule for a specific loan, providing the entire lending process with greater added value.

modefinance’s Amortization Plan Over Uncertainty (APOU) is developed on the bases of five types of amortization schedules:

• French amortization method – fixed installment amounts where the payment of overdue interest and capital share vary

• Italian amortization method – varying installment amounts where the payment of overdue interest share varies, while the capital share remains fixed

• Bullet amortization method – installments composed only of interest shares, while the final installment is equal to the initial capital amount plus the final interest share

• Balloon amortization method – only part of the capital amount is paid in installments until maturity and the rest in one final macro installment

• The model is dynamic to an extent that it gives the possibility to the user of flexibly inserting the number of installments, repayment deadlines, capital shares and interest rates.

modefinance’s APOU solution carries out fully automated standardized amortization plan metrics, namely indicators that help evaluate the quality of an amortization schedule, all while taking into consideration the obligor risk and thus allowing the creditworthiness output of the latter:

• Canonical and Risk-Based Net Present Value (NPV)

• Canonical and Risk-Based Internal Rate of Return (IRR)

• Average Time to Maturity and Duration

• Risk-Adjusted Return on Capital (RAROC).

modefinance amortization metrics: risk included in all parameters

Traditionally, amortization schedules are based on the above-mentioned metrics, however without integrating the risk parameter in their calculation, thus lacking of a dynamic and advantageous creditworthiness tool. Meanwhile, the main feature of the Amortization Plan Over Uncertainty model is the ability to consider payoffs of the amortization plan adjusted with the probability of default, namely the payoffs follow a binomial distribution (entity’s default or non-default).

{kind=link}

At time 𝑡₀ (begin of period), the financial intermediary lends to a company a 𝑐𝑓₀ amount of money. The company returns the loan to the bank over the next three years by making a Payment (R). The Payment (R) is composed of the capital (C) and the interest (I):

• Time 𝑡₀ – the financial intermediary lends a 𝑐𝑓₀ amount of money to the company.

• Time 𝑡₁ – two scenarios are possible:

- The company doesn’t repay the payment (R) and the financial intermediary loses all the capital (Payoff 1).

- The company repays the payment (R),

and so forth following the same logic.

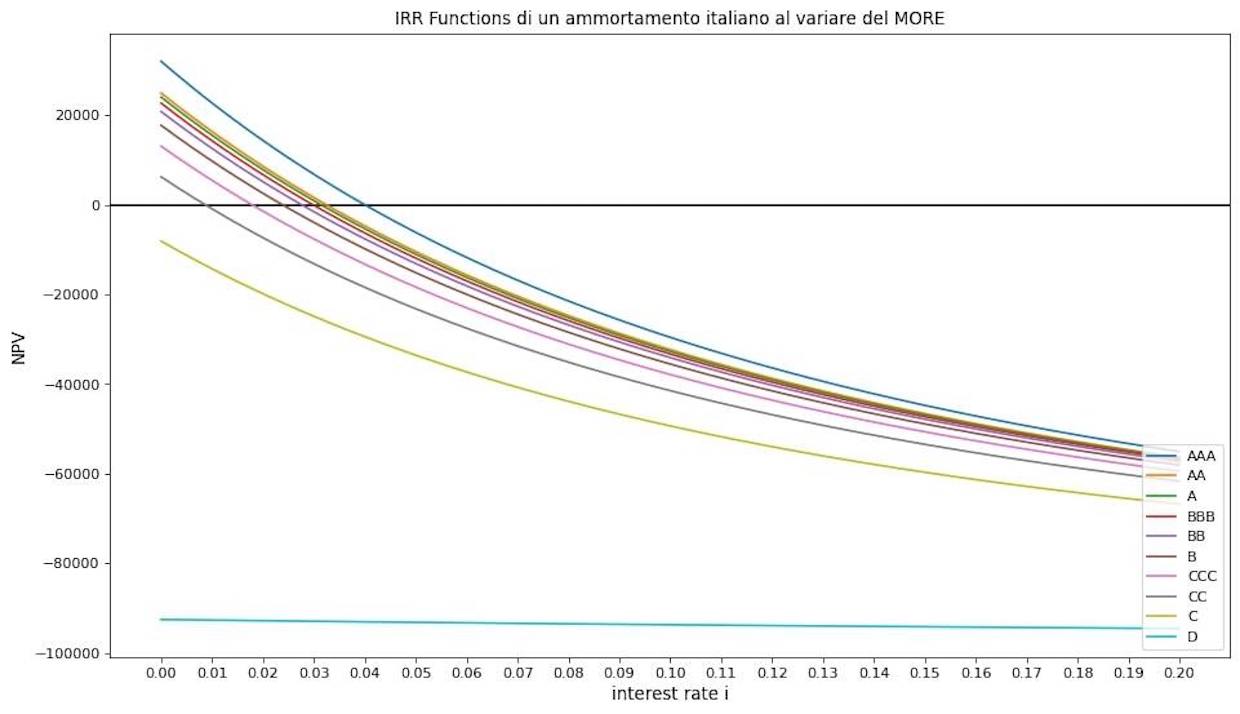

The first metric to be considered is the Net Present Value (NPV), a parameter that indicates the value of all future cash flows (both positive and negative) over the entire life of an investment discounted to the present, used to determine the profitability of a business or investment security. Thus, an operation is profitable when the NPV is greater than 0. This metric, integrated in the Amortization Plan Over Uncertainty – and called risk-based NPV – is directly proportional to marginal survival probabilities and payments, while it is inversely proportional to the interest rate, thus allowing to observe the relation between the company’s rating and the NPV. As it can be noted from the graph below, at the same value of interest rate, the NPV is higher for higher rating value.

{kind=link}

Being based on the customer’s personalized needs, the Probability of Default and thus Survival Probabilities calculations can be customized, allowing the interest rate used to discount the repayment in the calculation to be:

• A fixed value given as an input by the user

• List of interest rates given as an input by the user

• List of interest rates automatically defined by the term structure of interest rates, the latter estimated using the Nelson Siegel Svensson Model.

A metric strictly correlated with the NPV is the Internal Rate of Return (IRR), used to estimate the profitability of potential investments. More specifically, IRR is the discount rate that makes the NPV of all cash flows equal to zero, given that a transaction is profitable for the financial institution only in the case in which the NPV is higher than zero. Thus, APOU’s risk-based IRR is the discount breakeven rate above witch a transaction proves to be profitable, automatically taking into consideration the risk of the financial transaction, making the traditional method and estimates far less accurate.

{kind=link}

Two other important metrics that can be calculated by modefinance’s APOU model are the average time to maturity and the duration. As per definition, the average time to maturity is average remaining time to maturity for each security or contract composing a debt instrument, expressed in years. On the other hand, duration is a measure of the sensitivity of a bond’s price (or of another debt instrument) to a change in interest rates. This means that the duration defines when the financial institution gets back the funded amount without the interests. Whereas maturity is reached when both the funded amount and interests are paid off.

Eventually, a crucial metric for the development or evaluation of an Amortization Plan Over Uncertainty is RAROC, a risk-based performance and profitability measure that reflects the finite interval of interest rates where it is economically sensible for a financial intermediary to originate a loan.

Lastly, the Amortization Plan Over Uncertainty gives also the possibility to include financial guarantees into every type of amortization plan’s construction or evaluation, which ensures that the financial intermediary does not lose the entire capital in case of obligor’s default, but it cashes in a sum that must, however, remain lower than the residual debt.

APOU model, risk evaluations integrated in amortization plans, in a completely automated way

The APOU model, developed entirely on financial institutions’ needs of working with market rate instruments, is customized according to interest rates established by the bank itself and integrated in modefinance’s proprietary patented Tigran Risk Platform, for a fully digitized and automated process of building or evaluating an amortization plan.

Moreover, the digitization of the building and evaluation of amortization plans with risk-based metrics, allowed our analysts to develop our proprietary Pricing model, a tool based on the fair-value principle, capable of calculating the active rate pricing on the target amortization plan. Thus, while the traditional target rate takes into account the investor’s needs expressed in terms of ROI, operational cost and cost for counterparties, the market and recovery rate take into account the risk of the financial operation, following a fair-value pricing approach.

In conclusion, the integration of risk in the building and evaluation of amortization plans impacts not only the bank itself, but helps reducing the number of defaulted companies, a phenomenon that will have a positive effect on the challenging period of crisis we are living in.