Definition of sustainable finance

European Union’s initiatives, Glasgow COP26 and various news given to us daily through media. With all these inputs, it is hard not to have heard about sustainable finance. However, not everyone can define this notion. According to CONSOB (National Commission for Companies and Stock Market), sustainable finance is the application of the concept of sustainable development to financial activity. Therefore, its purpose is the direction of capital towards activities that generate economic value, but also putting environmental, social and governance (ESG) issues in the center of business and investment decisions.

Namely, sustainability is important for environmental protection in itself, but also for investors, since climate change constitutes a considerable risk for “traditional” funds. While the financial world focuses on a low-carbon economy, new climate-oriented business models represent new investment opportunities. Besides, the increasing importance of green finance does not take into account only the protection of the environment, but values such as recognition of a fair remuneration and respect of ethical and social values, as well. This is important news since green finance aims to put the financial system at service of the collective well-being.

{kind=link}

Green Finance Data in the EU

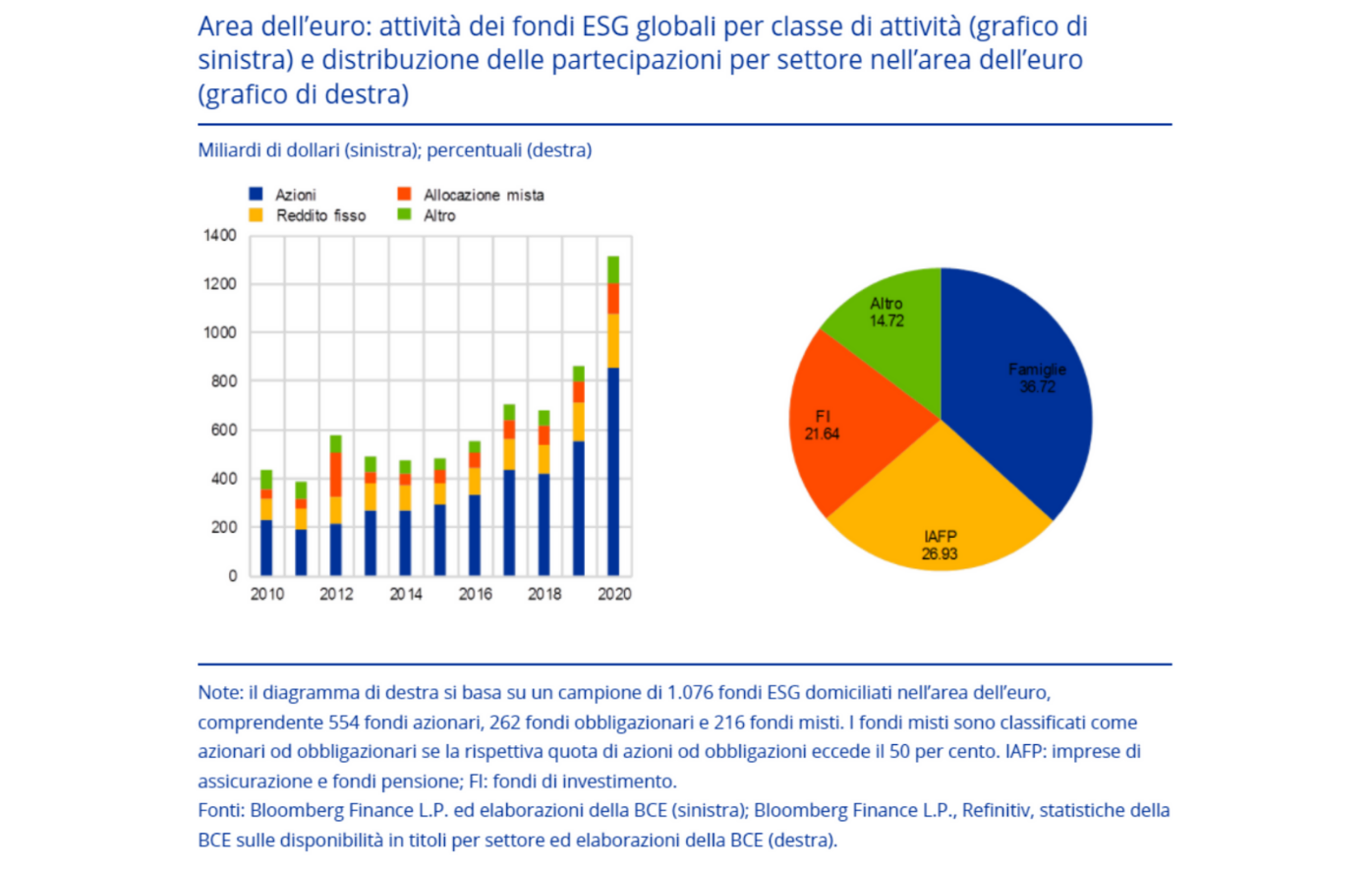

The subject of sustainable growth in the financial world received little interest in the past, but this trend has changed in the last few years. From an ECB study emerges that activities managed by ESG investment funds and Green Bonds have increased by more than 170% from 2015 to the present day. From January to October 2020, these investments registered a saving of more that €150 million, 80% more compared to the same period in 2019. Furthermore, in November 2021, Europe counted 2196 ESG funds, that is 77% of the total of these investments registered. In the opinion of analysts from the Italian Association for Financial Analysis, this trend is set to continue in years to come.

The EU can be considered an innovator in the legislation of sustainable finance field, a fact that can be deducted from a number of initiatives, such as the European Green Deal, the New Strategy for Green Finance published in July 2021 and the issuance of Green Bonds. However, despite this, the final implementation of the taxonomy of sustainable financial activities is scheduled for the current year, which will find the adoption of additional delegated acts and the definition of guidelines for analysts, banks and enterprises.

An important example is given by the Corporate Sustainability Reporting Directive (CSRD) that will have to be implemented by all EU members by 1st December 2022. This directive incorporates all those environmental and social factors that fall within of the ESG characteristics definition. Those include mitigation of and adaptation to climate change, working conditions improvement, including secure employment, salaries, social dialogue, work-life balance and a healthy and safe working environment.

Before continuing with the analysis, it has to be highlighted that the Regulation of the European Parliament and Counsel relating to the establishment of a Framework that favors sustainable investments (briefly: taxonomy Regulation) was issued in June 2020.

As far as the latest decisions of the European Commission when it comes to green finance are concerned, the New Strategy for Sustainable Finance has to be mentioned. This regulation indicates some initiatives for tackling climate change, mainly by increasing the investments and by including European SMEs in the transition towards a sustainable economy at the same time.

These and various other initiatives show how the EU has become a global leader in the establishment of international rules for green finance, with the aim of safeguarding the planet, valuing human capital, increasing investments, and avoiding the emergence of shell environmentalism.

Green Finance in Italian SMEs

On the initiative of the European Union, green finance is ever more established in Italy, as well. According to a survey conducted by the Sustainable Finance Forum, COVID-19 pandemic has had a strong impact on the SRI market (Sustainable and Responsible Investments) in Italy because it changed the financial habits of investors. Moreover, it has been highlighted that 35% of entrepreneurs in charge of ESG firms increased the share of sustainable investments and 57% plans to do so in the near future.

In addition, attention toward the economic situation in general has increased, with a strong focus on the risk profile of investments. As a result, given that a preference for low-risk investments has grown by 23%, ESG investments have increased, as well. This also due to the fact that 64% of dark green funds (those that promote most sustainability) have a corporate rating ranging from AAA to AA.

Despite the fact that Italy made great strides in the green finance domain, especially because of EU initiatives, Italian SMEs are still lagging behind with the spread of investments towards companies that meet the ESG parameters. This is given especially by the modest financial education of the investors.

Supporting Italian SMEs in their sustainable conversion does not bring only a reputational advantage, but also the implementation of a higher purpose, namely a contribution for the creation of a greener and a more inclusive economy, but not only. From the study conducted by the Sustainable Finance Forum emerges that SMEs involved in processes of sustainability reporting (55% of the total) have experienced positive effects due to this choice, also in terms of enticing new clients and accessing new credit facilities.

ESG Ratings

The last aspect that has to be taken under consideration when talking about green finance in Italian SMEs is the ESG rating. Unfortunately, the present-day evaluation is not enough, since increased availability of information is needed, as well as guidelines and standardization. For example, it frequently happens that ESG ratings relating to individual companies refer to uneven methodologies and they appear to be little correlated. Here too, measures of regulatory character and initiatives both by SMEs and rating agencies would be appropriate.

Given that investors need tools that could help them identify ESG risks within firms of their interest and compare them among the various sectors, from 2022, modefinance clients will have access to cutting-edge tools, ever more focalized on all-around sustainability, as well as ESG Rating evaluations capable of providing a complete enterprises’ landscape with regard to governance, social responsibility and environmental impact. These risk assessments, combined with the “traditional” credit risk evaluation, provide the client with a wider vision of the risk they will be facing, should they decide to invest in a given entity.

The data presentation and analysis given by the European Union and the Italian Sustainable Finance Forum have provided several encouraging ideas on the development of green finance in the EU and in Italy. As much as Italian SMEs need to be given more emphasis in the ESG department so that they can reach European standards, it is easy to understand that in the last few years, and particularly during the pandemic, some great strides have been made in the context under analysis.