How to manage exposures in oplon Risk Platform

In August 2018, the European banks witnessed a significant stock fall caused by the plunge of the Turkey’s lira. The consequently fear of a domino effect on the global equity markets has once again raised the issue of the exposure risk and the need for safe and reliable risk management tools.

The issue concerns all the market players, from financial institutions to non-financial corporations. Exposure can be defined as the amount of an investment (or a credit) and since no investment is risk-free, exposure refers to the risk of loss of the money invested. A previous evaluation of the counterparty creditworthiness and of the related risks is therefore required.

{kind=link}

How to assess the exposure risk

According to the European Capital Requirements Regulations (Basel), banks and depositary institutions have to establish an equity reserve to cover expected and unexpected losses.

The so-called regulatory capital (or Capital Requirement) is calculated by applying a set of credit risk measurement techniques (Standard Approach, IRB or Advanced IRB) based on:

- External rating (issued by ECAIs, i.e. institutions, other than banks and insurance companies, authorized to issue credit assessment);

- Probability of Default (PD);

- Loss Given Default (LGD);

- Exposure at Default (EAD);

- Maturity (M).

The European regulatory framework also applies to corporates and non-financial institutions, which have to institute a loss allowances (Economic Capital) according to the expected losses. Moreover, to prevent themselves from the counterparty insolvency risks, companies can also rely on the credit ratings issued by the Rating Agencies or on the available scoring tools.

Are there any protection tools?

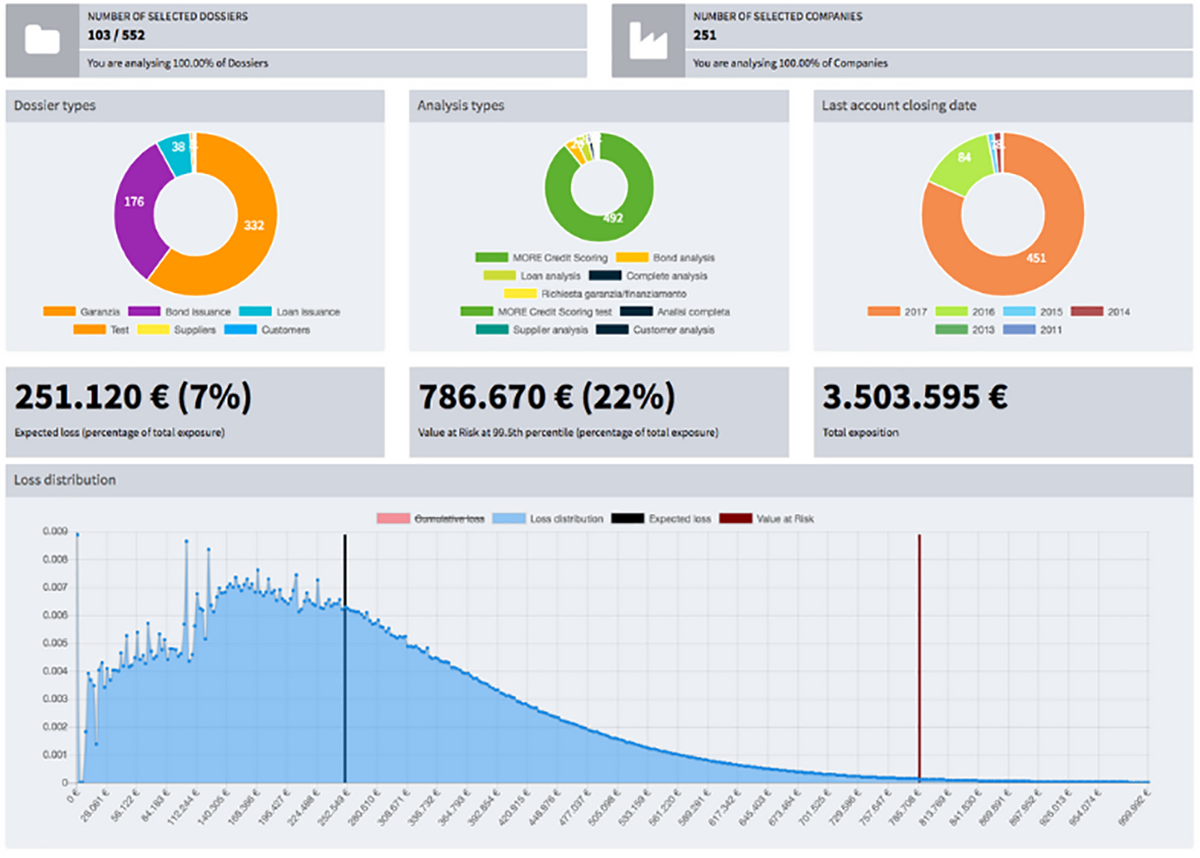

To sum up, in order to reduce the risk of losses, it’s firstly necessary to quantify the exposure risk and extend the analysis to the entire portfolio. oplon Risk Platform includes all the risk management analysis tool needed by companies and financial institutions in a single framework. Exposures can be managed either individually or at a portfolio level and the features included allow capital allocation's evaluations for both prevention and investment purposes.

oplon allows to:

- input the exposure data: exposure data can be entered in the relative form. Amount of the exposure, maturity, recovery rate and collateral are the supported fields. Depending on user needs, additional fields can be added when setting up the platform;

- assess a company or bank creditworthiness: via MORE creditworthiness evaluation tool is it possible to get the credit score and a fundamentals analysis of any company or bank. MORE is modefinance’s methodology for risk assessment. The MORE score can be used by financial institutions as part of the IRB or Advanced IRB approaches (as ECAI, modefinance credit rating are also compliant with the Standard Approach);

- evaluate the Probability of default (PD): MORE also provides the 1-year PD estimation of the analyzed company. Furthermore, according to the customer needs, it is also possible to re-compute the metric, for example extending the timeframe or setting a different definition of default;

- calculate the expected and unexpected losses (VaR) and their distribution: the portfolio risk analysis tools allows to estimate the amount and distribution of the expected losses and the Value at Risk. The latter is calculated over a 1-year timeframe and on the loss percentile defined by the user. The portfolio risk analysis tool allows company to define the entity of the loss allowances (according to IFRS9).

{kind=link}

Furthermore, it is also possible to request customized models (like pricing models or Loss Given Default models); the models are developed by modefinance according to the user needs and set up within the platform.

To discover all the features included, you can visit our website or download the brochure.