The “Osservatori Digital Innovation” of the Politecnico di Milano have presented a study on the impact of the Fintech and Insurtech world in Italy, providing some really interesting insights.

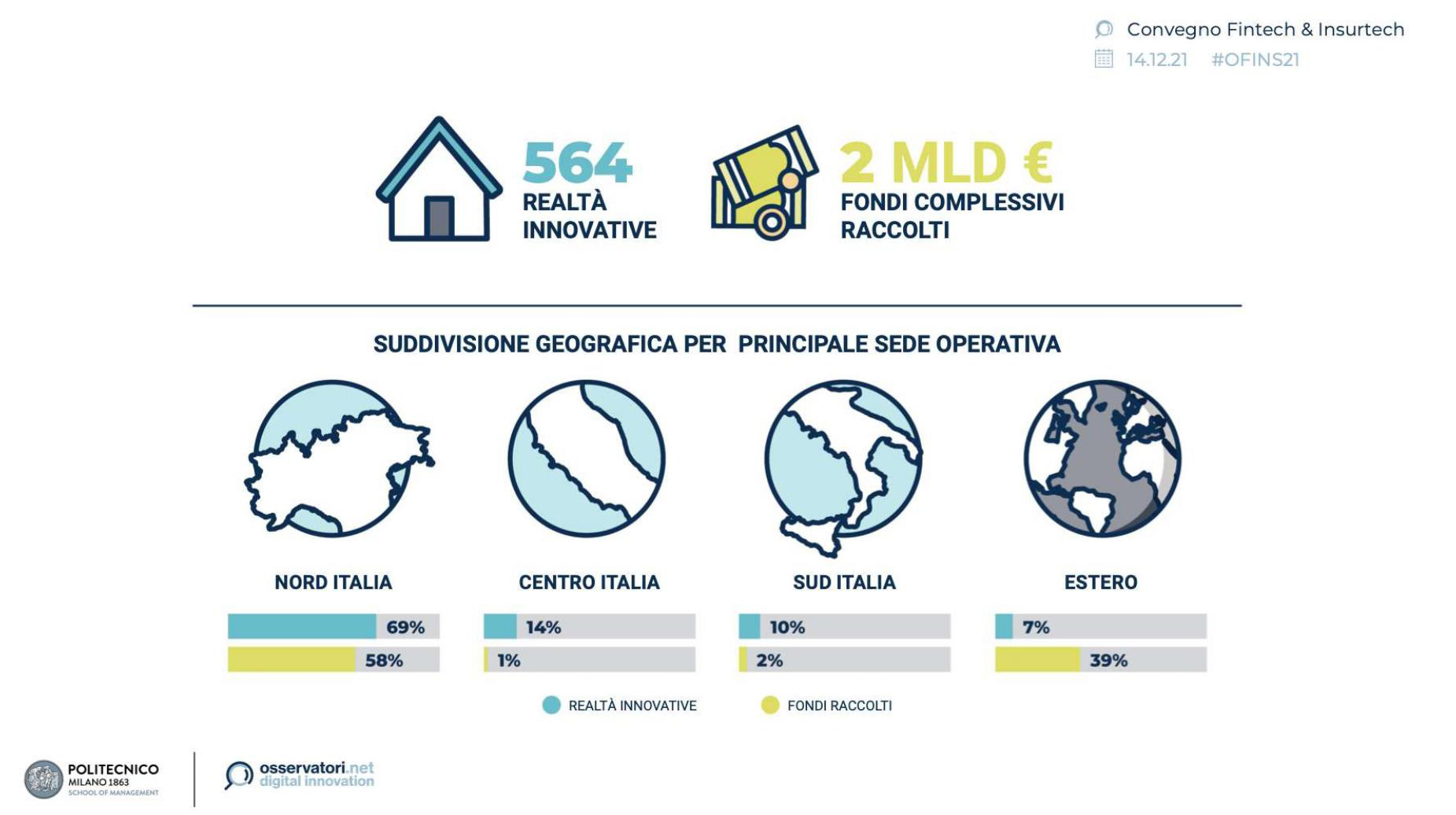

The results are very encouraging, as they show an increase in consumer awareness, that are increasingly choosing to rely on emerging companies in this field. Nowadays, there are 564 innovative realities in Italy, capable of raising a total of EUR 2 billion.

The Italian Fintech & Insurtech companies, overview

{kind=link}

The numbers of Fintech in Italy

The study shows that Italian consumers have become more digitally literate in the financial world over the past year, and they are increasingly willing to use alternative services instead of relying on traditional players. In fact, it was noticed that 54% of Italians use digital payment services instead of relying on traditional banks, and 44% of consumers use apps to transfer money.

As far as insurance services are concerned, it has been shown that an average of 31% of consumers choose to buy digital insurance policies, which shows that digital services in the insurance sector are still underdeveloped and underused by consumers who continue to trust traditional players.

Banks and insurance companies are therefore being joined by new innovative realities, showing a dynamic collaborative environment between traditional institutions and Fintech firms, to expand new solutions’ adoption and offer more advantageous conditions, tailored to the individual and with a renewed focus on the user.

In the area of small loans, 61% of Italians continue to turn to banks, while 23% are ready to consider new loans linked to car manufacturers, and 32% loans linked to gas and electricity suppliers.

In terms of insurance, on the other hand, 75% of consumers said they are still tied to traditional insurance companies, while 26% rely on policies linked to trade associations and 22% on policies linked to postal services. These data show how, when taking into account the different players within the financial sector, the Italian scenario is expanding: consumers have a wider choice between the various players within the market.

Digital Innovation and Open Finance

The Covid-19 epidemic has certainly given a boost to the digitalization and automation of financial services, which is becoming an ever more present necessity, as demonstrated by the 12% more Italian users taking advantage of Open Banking, given the pandemic situation that made it necessary to use digital banking channels.

It has also been shown how necessary it is for businesses and SMEs to change their habits; they are moving towards the path of Open Finance. This year saw the introduction of new digital channels and services for the financial sector in view of the growing need and capacity for innovation on the part of both consumers and businesses; numerous initiatives for collaboration between the various players in the market were therefore launched. It has been pointed out that access to capital for Fintechs and Insurtechs is still limited, and Venture Capital and foreign funds have not yet recognized the potential of these realities, which are still locally bound.

Coopetition is therefore the key word: new and traditional players join forces, pooling the innovative drive of emerging players with the level networks and capital needed to finance it provided by traditional players.

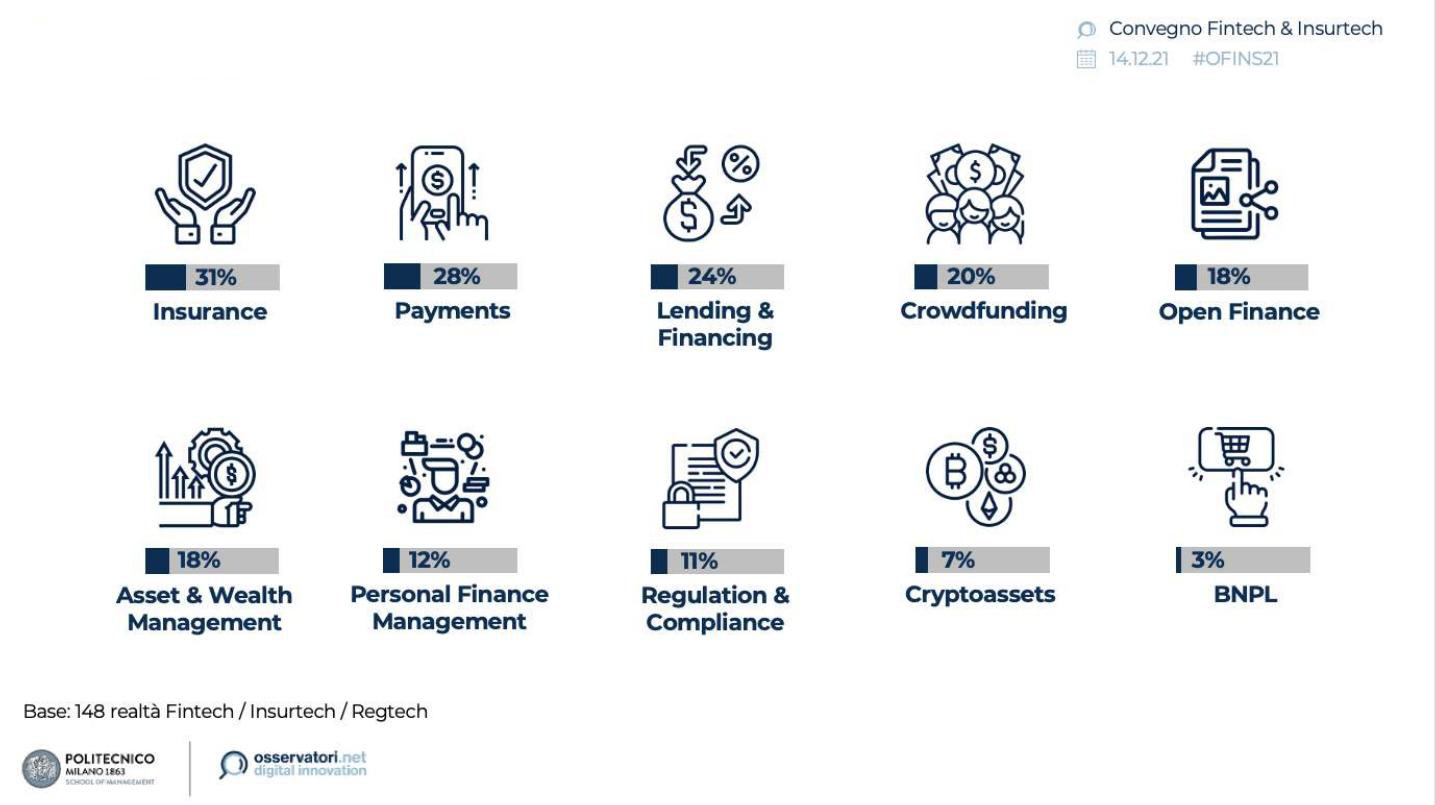

The services offered by the Fintech entities in Italy

{kind=link}

New market players: the drive to Digital Lending

As already mentioned, Mobile Banking is the main driver in the B2C sector of the Fintech and Insurtech universe in Italy, with activities ranging from the provision of instant credit transfers to the development of apps that allow the management of payment accounts held at different banks. But it is not only this area that is growing more and more.

Digital Lending, the digital credit service, is also playing a key role today, with activities that are increasingly emerging at the digital level and that concern us closely, such as credit assessment and credit monitoring, but also activities such as digital onboarding of new customers and Factoring, i.e. the transfer of existing invoices and future receivables to specialized operators before they fall due.

With regard to the latter, we recently announced an agreement with Arcares to bring process automation closer to the real economy and to make it available to the country's leading Factoring platform provider.

Sustainable Finance

Another very interesting point that emerged during the presentation of this study concerns the achievement of social sustainability goals: according to Italian consumers, in fact, the financial sector is among the most important in this sense and ranks third (after the sectors "University and Education" and "Cultivation") out of 11 sectors taken into consideration.

We are starting to talk about Sustainable Fintech, the search for sustainable solutions to be introduced within the Fintech and Insurtech world, such as "micro Fintech" and "micro Insurtech" solutions or apps that allow investing in sustainability, and accompany these with the already existing sustainable alternatives such as ESG investments or Green Bonds.

The study therefore provided a number of interesting insights and data that allow us to gain a greater awareness of the Italian situation in the context analyzed. As a Rating Agency and a TechFin company, modefinance is developing a process of digitalization of financial services, offering solutions tailored to individual needs and responding increasingly to the demands of the financial world, especially data processing and value extraction: a prime example of this is the development of Nowcasting modelling applied within the Tigran platform.

By taking part, as usual, in the studies conducted by the “Osservatori Digital Innovation” of the Politecnico di Milano, we are able to gain an even better understanding of the next steps to be taken, with a view to further improving the experience of our clients and increasing the awareness of consumers, be they individuals or businesses, in the FinTech and TechFin world.