Our ForST model was born in 2019. Short for Forecasting & Stress Test, ForST is a simulation tool based on statistical principles designed to generate budget projections for three different scenarios and estimate the creditworthiness evolution of the analyzed subject. Moreover, the model allows performing stress tests by modifying some of the input variables of the simulation, making it one of our most sought-after models.

In the current ever-changing financial landscape, however, banks require innovative and customizable tools that can provide increasingly accurate financial forecasts and enable strategic decision-making.

ForST evolves – the launch of ForST Contabile

In this context, we have launched ForST Contabile this year, an advanced simulation model that provides even more accurate forecasting of companies' future financial statements. By using specific inputs, the model calculates different accounting items, heavily relying on an accounting approach, to offer a detailed view of the financial situation of a particular company.

There are two key inputs to the model that enable the simulation of all items within the financial statements:

- the estimated future revenue of the company, calculated using the modefinance Company Nowcasting model. This model evaluates the economic and financial risk of Italian companies in real-time by comparing their performance with their respective micro-sector

- the amount of financial debts obtained from the Central Credit Register to assess the impact of debts on the financial statements.

Father and son, ForST and ForST Contabile, are complementary and now available to users of our patented platform, Tigran, to better meet the needs of financial institutions and support them in credit risk management.

So what makes our new forecasting model stand out from others available on the market?

“ForST Contabile provides significant added value compared to its predecessor, ForST, as well as other available forecasting models, thanks to its exceptional flexibility," says Giacomo Pazzini, Quantitative Analyst in our Fintech team. "Banks can request model customization according to their specific needs, integrating all the strategic elements they require. This adaptability allows financial institutions to personalize the model based on the peculiarities of their portfolio, obtaining solid, reliable, and highly customized financial analysis. With ForST Contabile, banks can face financial challenges with greater confidence and security, gaining a competitive advantage in a rapidly evolving industry.”

Furthermore, “another unique aspect of ForST Contabile is its seamless integration with other modefinance models available on the Tigran platform. For example, the Company Nowcasting model simulates the future revenue of the company, which is then inputted into ForST Contabile for projecting various items in the financial statements. Another example is the APOU model, which enables the creation of a customized amortization plan, and its values can be subsequently entered into ForST Contabile to simulate the impact on the financial statements of a debt repayment plan. This synergy among models allows banks to perform holistic simulations of the financial health of the analyzed companies.”

How does the model work?

To clarify the operating principle of ForST Contabile, let’s provide practical examples of how the model is applied:

SIMULATION OF BALANCE SHEET AND CASH FLOW

Various balance sheet items that influence the company’s financial position and income statement are simulated. Changes in fixed assets, receivables vs. clients, liquidity, and VAT receivable, for example, affect the values in the balance sheet. In the income statement, simulating revenue, EBITDA, total costs, and depreciation impacts the value of EBIT. Additionally, adjusting interest rates influences financial management and profit or loss before taxes, thus affecting the net profit or loss for the period.

SIMULATION OF DEBT WRITE-OFF

Through ForST Contabile, it is possible to simulate the effect of a debt write-off on the company's financial health. Simulating this operation involves a reduction in unpaid financial debts, leading to variations in related balance sheet items. The decrease in financial debts results in increased financial revenues and reduced interest expenses, thereby improving the company's financial management.

SIMULATION OF FULL OR PARTIAL DEBT REPAYMENT

This simulation affects the items of financial debts, interest expenses, and modifies the originally constructed amortization plan. The ability to test different debt repayment scenarios allows banks to assess the impact on the balance sheet and financial management of the company.

Simulation of the balance sheet with ForST Contabile

Let's go through the approach that the ForST Contabile model adopts in analyzing and simulating balance sheet items:

1. SIMULATION OF RECEIVABLES VS. CUSTOMERS

The foundation for all simulations in ForST Contabile is the future revenue of the company, calculated based on the Company Nowcasting model. By combining this element with the historical revenue value (taken from the latest financial statement), it is possible to simulate the future revenue and, consequently, the Δ Revenue. It's important to note that a company's revenue is directly proportional to Δ Revenue, VAT payable, and Receivables vs. Customers – as sales increase, the company's revenue increases. Based on the projected future revenue, the value of Receivables vs. Customers is simulated, representing registered sales to third parties and providing an accurate estimation of the company’s credit.

2. SIMULATION OF LIQUIDITY

After simulating the value of Receivables vs. Customers in the previous step, the model calculates the target Receivables vs. Customers based on historical average collection days (DSO). By comparing the simulated Receivables vs. Customers with the target value, the model determines the potential increase in the company's liquidity, providing a forecast of its cash flow.

3. SIMULATION OF EBITDA

EBITDA represents the company’s operating income (excluding interest, taxes, depreciation, and amortization). Using historical EBITDA and the percentage changes in historical and simulated revenue, the model calculates the simulated EBITDA.

4. SIMULATION OF TOTAL COSTS INCURRED BY THE COMPANY

Total costs incurred by the company include both variable and fixed costs such as services, raw materials, and personnel. The simulation of total costs is based on the difference between the simulated revenue and simulated EBITDA.

The ForST Contabile model also separately simulates the future variation of personnel costs and operational costs. For personnel cost calculation, the model multiplies the historical percentage variation in personnel costs by the variation in simulated total costs, providing an estimate of how personnel costs will evolve based on changes in total costs.

Operational costs, including costs of raw materials and services, are simulated by considering the historical percentage variations in operational costs and the variations in simulated total costs. This allows for an evaluation of how operational costs will change based on changes in total costs.

5. SIMULATION OF FIXED ASSETS VALUE

The simulation of fixed assets value is conducted in two phases:

- Fixed assets are recalculated net of depreciation, distributing the multi-year cost of the asset over its useful life

- The possibility of the company acquiring new fixed assets is calculated based on the previous year’s profit.

6. SIMULATION OF SHORT-TERM AND LONG-TERM FINANCIAL DEBTS

This projection utilizes data derived from the Central Credit Register. It allows for evaluating the impact of debts on the balance sheet and liquidity. The simulation involves two possible scenarios:

- Increase in debts resulting in increased liquidity and interest

- Reduction in debts resulting in decreased liquidity and interest.

Validation of ForST Contabile: accurate analysis for reliable assessment of corporate credit risk

The validation of the ForST Contabile model, essential to verify the effectiveness and reliability of company balance sheet simulations, was conducted using two approaches:

Comparison between the actual and the simulated creditworthiness score (MORE Score)

- Analysis of error distribution.

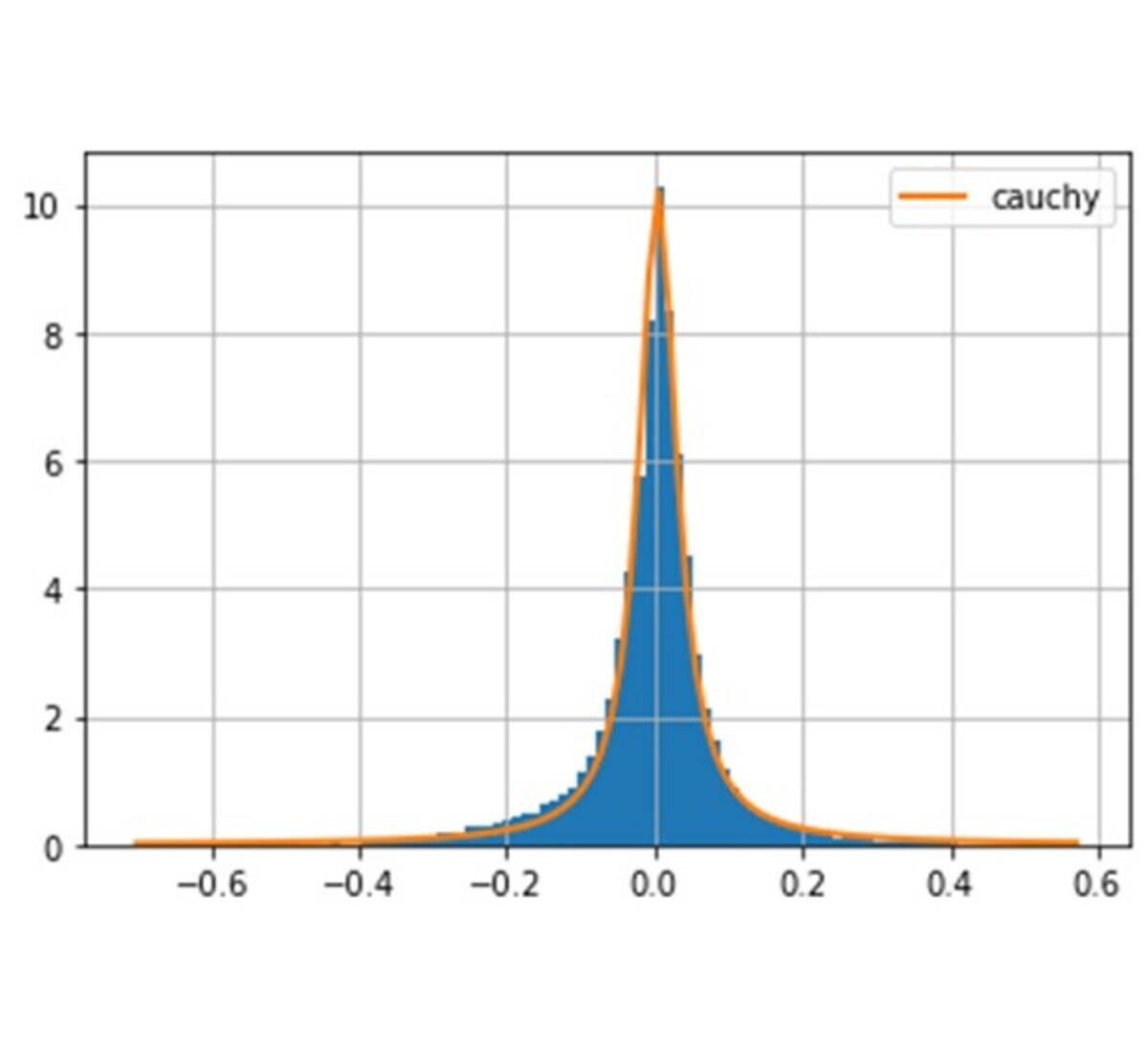

Data from a sample of 54,561 companies with a turnover exceeding one million euros and complete information on financial debts, Payables vs. Suppliers, Receivables vs. Customers, other operating debts and credits, and revenue were selected. The results provided an overall assessment of the model's accuracy, highlighting a low presence of errors between the simulated and actual scores. The Lorentz distribution showed a concentration of errors around the maximum value, with a very low average error and limited dispersion, as can be observed in the graph below.

{kind=link}

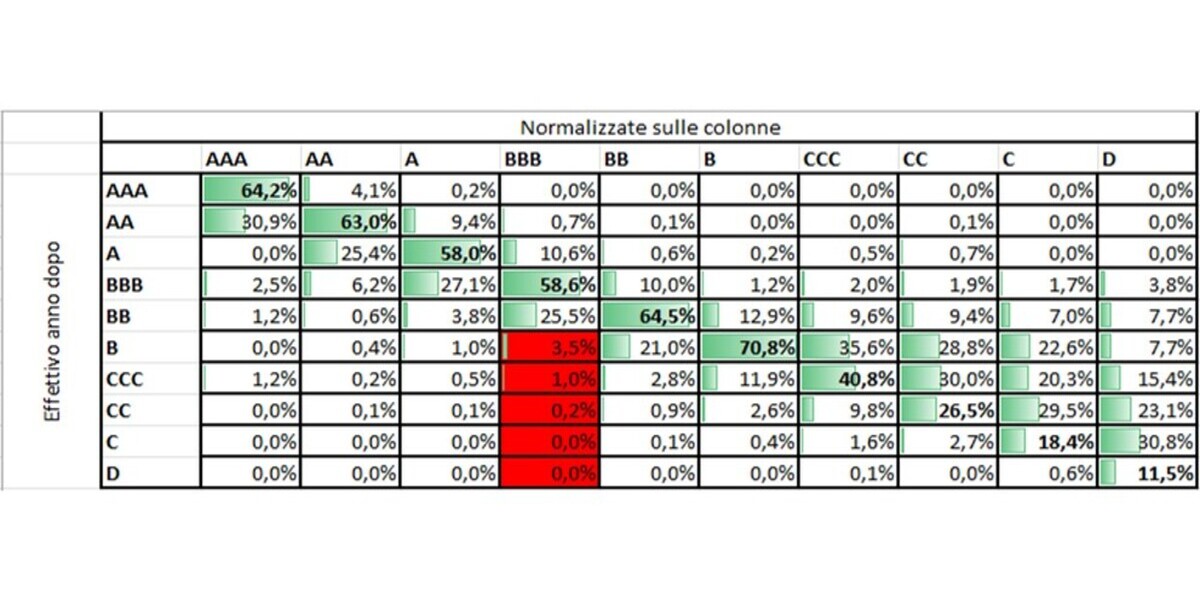

The comparison between the simulated and actual MORE Score through a transition matrix revealed a high correlation, with the majority of companies aligned along the diagonal of the matrix shown below.

{kind=link}

The ForST Contabile model has demonstrated to follow the historical trend of the MORE Score without significant deviations, confirming its reliability in providing an accurate assessment of companies’ credit risk.

Integration of the model within the Tigran platform

The ForST Contabile by modefinance is a valuable tool for banks seeking strategic decision support. Thanks to its integration with various models within the Rating-as-a-Service platform, Tigran (including the Company Nowcasting and APOU models), ForST Contabile stands out from other forecasting models. This means that, unlike other similar models in the market, input data can be estimated through forecasting models available in the platform, and the results, in turn, can be integrated and used as a starting point for further analysis within the platform. The high flexibility of ForST Contabile also allows customization of the model to incorporate desired strategies, whether it is increasing assets, planning debt repayment, or conducting debt write-offs.

Overall, the ForST Contabile model represents an evolving solution that supports companies and financial institutions in a constantly changing financial landscape, enabling them to adapt their strategies based on simulation results and their impact on their exposure portfolio.